Shares of Zoom Video Communications (Nasdaq: ZM) fell as much as 11% in after-hours trade on Thursday, despite the company beating revenue and earnings estimates for the third quarter. The company’s stock price recovered slightly after testing the $62 level it began trading at when its IPO was held in April.

Revenue growth was slower than the market expected, full stop.

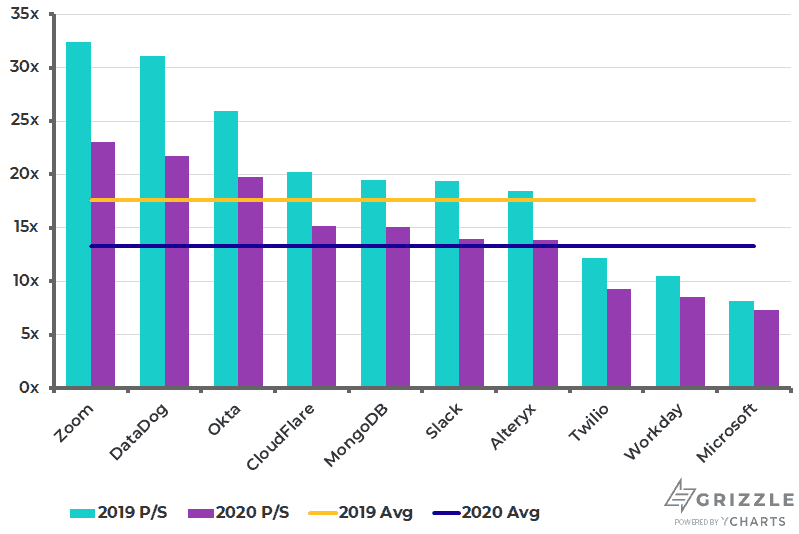

When you are the most expensive stock in the group, it takes nothing less than perfect execution to stay there.

Zoom was priced at a premium because revenue growth was stellar.

If revenue growth is now merely “great” the valuation has to come down.

Price to Sales Multiples (Prior to Earnings)

With the markets now worried about slowing growth, we would sit on the sidelines and wait to see where the multiple bottoms out.

This stock isn’t broken, it just needs to be handled with care.

Revenue Growth is Slowing Rapidly

The market reacted to evidence of a rapid slowdown in sequential revenue growth during this quarter, which looks set to continue during the current quarter.

Zoom’s management expects revenue for the fourth quarter to be between $175 and $176 million which will represent sequential growth of 5.3%. This compares to 14% in the third quarter and 19% in the second quarter.

Net income and earnings per share are expected to fall in the fourth quarter. Non-GAAP EPS of $0.07 are expected, compared to $0.09 in the quarter to September.

Full-year revenue guidance was at the upper end of the $570 to $615 million range analysts expected, but traders were hoping for more.

Margins Remain Steady

The company’s 81% gross margin and negative 1% operating margin remained largely unchanged from a year earlier. Sales and marketing expenses accounted for 57% of revenue, while R&D and general and administrative expenses accounted for 10 and 14% of revenue respectively.

Although Zoom generated an operating loss, interest income of $3.2 million resulted in net income of $2.2 million.

Third-quarter revenue of $166.6 million was up 85% year on year and beat consensus estimates by $10.4 million. Non-GAAP EPS of $0.09 were 6 cents ahead of analyst estimates while GAAP EPS were 4 cents ahead at $0.01.

Expanding Per Customer Revenues

The number of customers with 10 employees or more grew 67% from a year ago to 74,100. The net dollar expansion rate for these customers over the last 12 months was 130%.

546 customers generated $100,000 or more in revenue for Zoom over the last 12 months. While growth in customer numbers lagged revenue growth, the company is earning more from existing customers.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.