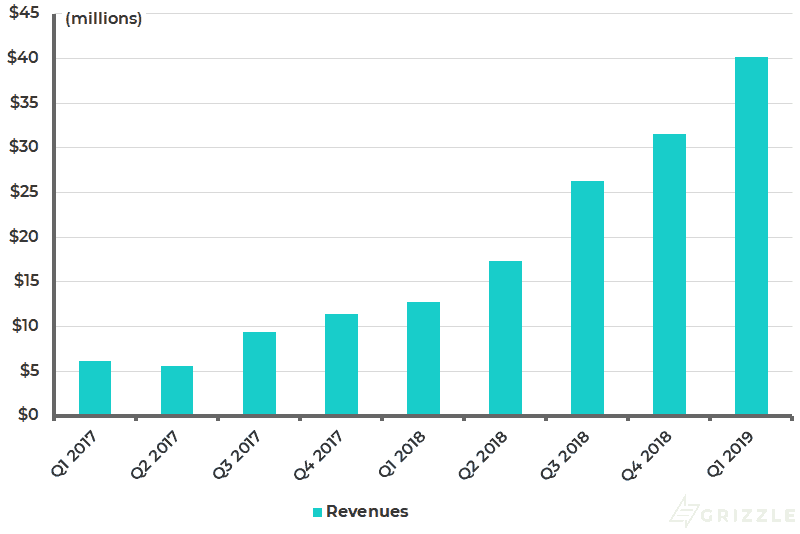

Beyond Meat’s first quarterly earnings as a public company did not disappoint. Results beat sell-side analyst estimates across the board for Q1-2019. Top line revenue came in at $40.2 million vs. consensus of $38.9 million (3% beat), and gross profit came in at $10.8 million (7% beat).

Grizzle has been unequivocal about the significant share price upside in Beyond Meat, before and after the IPO. We are the most vocal bulls on the name by a very wide margin.

While timid sell-side 1-year target prices were getting hit and hedge funds tossed stones we stood by our structural long-term thesis. IPO and non-IPO investors have all been handsomely rewarded, a rarity in the capital markets.

Short Sellers (Jr. Hedge Funds) Continue to Get Lit Up

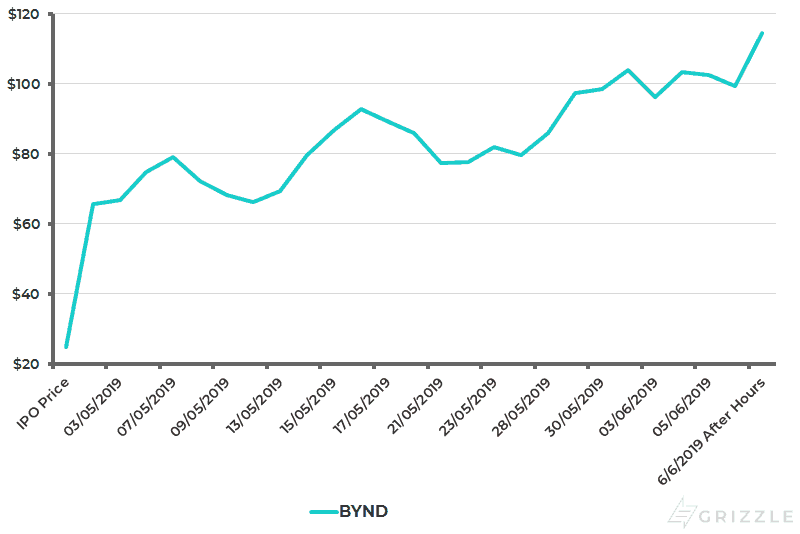

BYND shares rose a whopping +18% in after-hours trading to $117.49/share, short sellers continue to hemorrhage — the stock has been absolutely ruthless against a barrage of heavy short interest (~42% of free float).

With the borrow in excess of 100% there is no margin of safety for these randy ‘red meat’ traders whose short positions are grounded in philosophical beliefs and polo-shirt/khaki naiveté.

Beyond Meat Share Price ($/share)

Sales Juggernaut

There is no question that Beyond Meat is now a consumer cultural phenomenon similar to that of the iPhone. Fans of the Beyond Burger are rabid folks — we would go so far as to call them evangelists. First quarter revenue of $40.2 million represented an increase of +215% from the previous year, the highest quarterly year-over-year growth over the last 2 years.

Beyond Meat Quarterly Revenue

The Beyond Burger has been the key driver of sales growth, driven primarily by food-service points of distribution. These quick service restaurant chains (TGIF, Carls, Del Taco, A&W) also provide vital brand building for Beyond Meat as the menu items include ‘Beyond Meat’ in the name.

The company is guiding to full-year 2019 revenue of $210 million (consensus at $205 million). On the conference call management spoke to the additional sales opportunities in the new product lines of breakfast sausages, ground meat and Beyond Burger 2.0.

Management also stated that full-year sales will be weighted heavily to Q2 and Q3, representing 55% of overall sales. We could see short sellers abandon their positions over the near-term on the back of this, resulting in more upside pressure for the stock (short covering).

Operational Flex

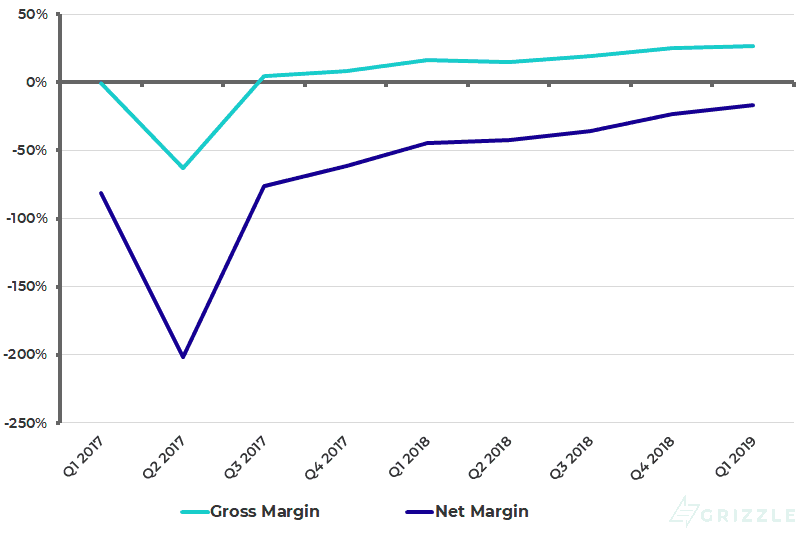

Beyond Meat put up a stellar quarter operationally. We continue to see sequential quarter-over-quarter improvement on both the gross and net margin.

Gross profit increased 421% to $10.8 million, while gross margin stood at 26.8% vs. 16.1% from the previous year (1,000 bps increase). Margin improvement was driven by operational leverage, sweating the assets the old fashioned way — running more burgers through the mill so to speak.

Beyond Meat – Gross Margin and Net Margin (%)

Management believes the company will be full year break-even for 2019 on an adjusted EBITDA basis — an impressive target to say the least. The company has secured the necessary feedstock required for its growth runway and additionally has the flexibility to source varied forms of plant-based proteins (other than peas).

The company is confident that it will be able to adequately ramp up production capacity for any new major fast-food customer — i.e. McDonald’s. Grizzle believes that McDonald’s will launch a veggie/vegan burger in 2019 and that Beyond Meat is the leading contender to supply the chain.

Outlook

Beyond Meat CEO Ethan Brown spoke confidently about the company’s aggressive near-term growth and margin targets and more importantly he outlined his medium-term growth vision.

He’s not afraid of the onslaught of competitors, it’s clear he thrives on the challenge. He echoed Grizzle’s view that 1st mover advantage in this segment cannot be understated. Grizzle believes new entrants will take at least 3-5 years to get remotely close to Beyond Meat or Impossible Burger in terms of taste and texture.

Brown also spoke to the real fundamental understanding that Beyond Meat has of its customer base and their desire for ingredients free of soy, gluten, and GMOs. Grizzle believes that consumers will ultimately prefer pea-based protein over soy-based competitors like Impossible Foods.

With respect to the near-term revenue growth outlook, Brown stated that additional sales from Tim Hortons are not incorporated into their full-year forecasts. Therefore given a reasonable uptake in sales at Tim Hortons (no reason to believe that won’t be the case), Beyond Meat will have to revise up their full-year revenue and profit outlook.

In terms of global growth, the company is focused on Europe and Asia. In Europe there is a well established vegetarian/vegan market, while in Asia there is a ‘desperate need’ for alternatives.

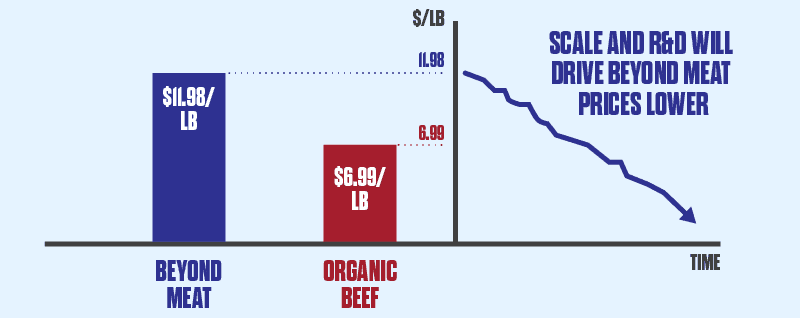

Brown laid out the company’s ambitious “5-year initiative” to undercut the price of one type of animal protein, he believes the company can achieve this in beef. This would be a profound achievement and in our view would unlock far greater share price upside than we had modelled in our base-case target price.

Valuation and Upside

After the massive share price move post earnings Beyond Meat now trades on a 2019 Price/Sales ratio of 33x based on management guidance.

As we stated in our initiation report we believe that investors using near-term valuations metrics as a guide for their BYND investment are deeply misguided. This is a company growing more than 200% y/y.

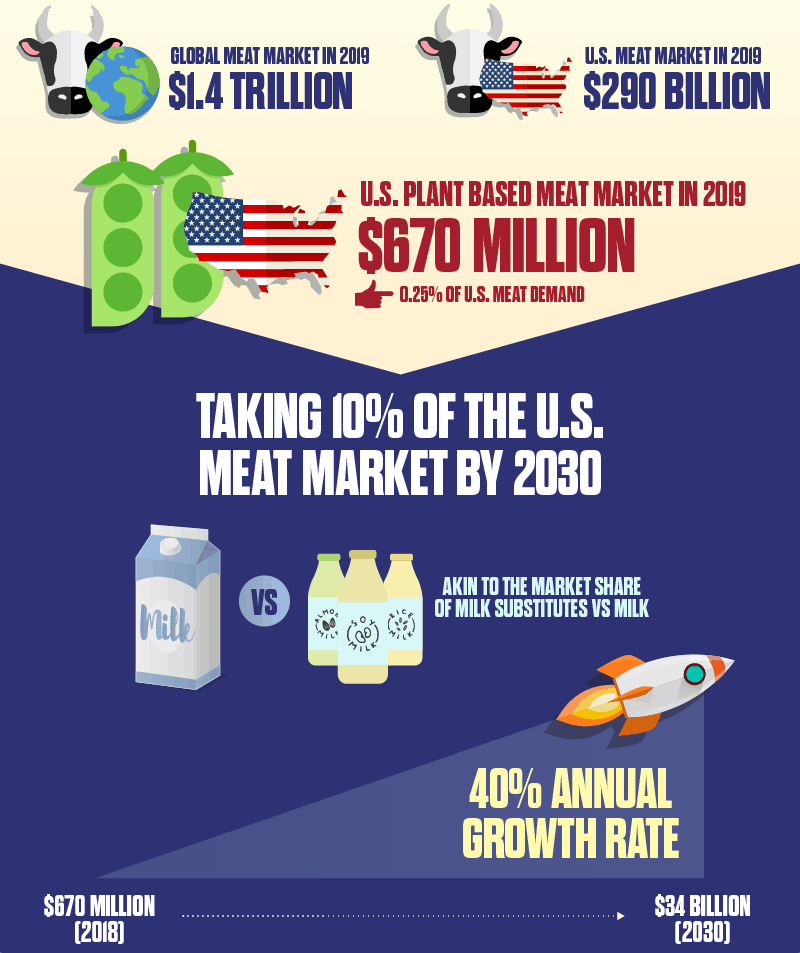

The only way to correctly look at a company this early in its growth stage is to understand the market opportunity in the out years (2030 and beyond). Near-term estimates will always look too high, scaring you away and obscuring reasonable long term valuations.

To put it into perspective Facebook (NASDAQ: FB) at its 2012 IPO traded at a P/S of 20x and had an associated sales growth of 55%.

Beyond Meat’s medium-term outlook gives us confidence that our forecast annualized sales growth CAGR of 40% from 2019 to 2030 is very achievable given that the company is growing 200% over the near term. Our 2030 target price is $1,100/share, from the current share price ($117.5/share) it represents an annual return of 22.5% for investors — a very acceptable risk/reward.

In today’s low-interest rate environment and growth-starved investment landscape, we believe investors can theoretically continue to be buyers of BYND up to $190/share in the near-term, this would result in an annualized return of 18%. Short sellers will continue to get sizzled!

In the interest of full disclosure, employees of Grizzle personally purchased and currently own stock in Beyond Meat. See the Content Disclosure section on our Terms and Conditions page for more details.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.