SUBSCRIBE TO GRIZZLE and Invest Smarter

Who is Bill.com?

As the name suggests Bill.com was created to simplify the paying and invoicing of bills.

Bill.com is targeted at small businesses that traditionally cut paper checks and had filing cabinets filled with old invoices and receipts.

These one-man operations can now go digital, simplifying and improving their day-to-day transaction processing.

Popularity is Growing but User Experience Could Use Some Work

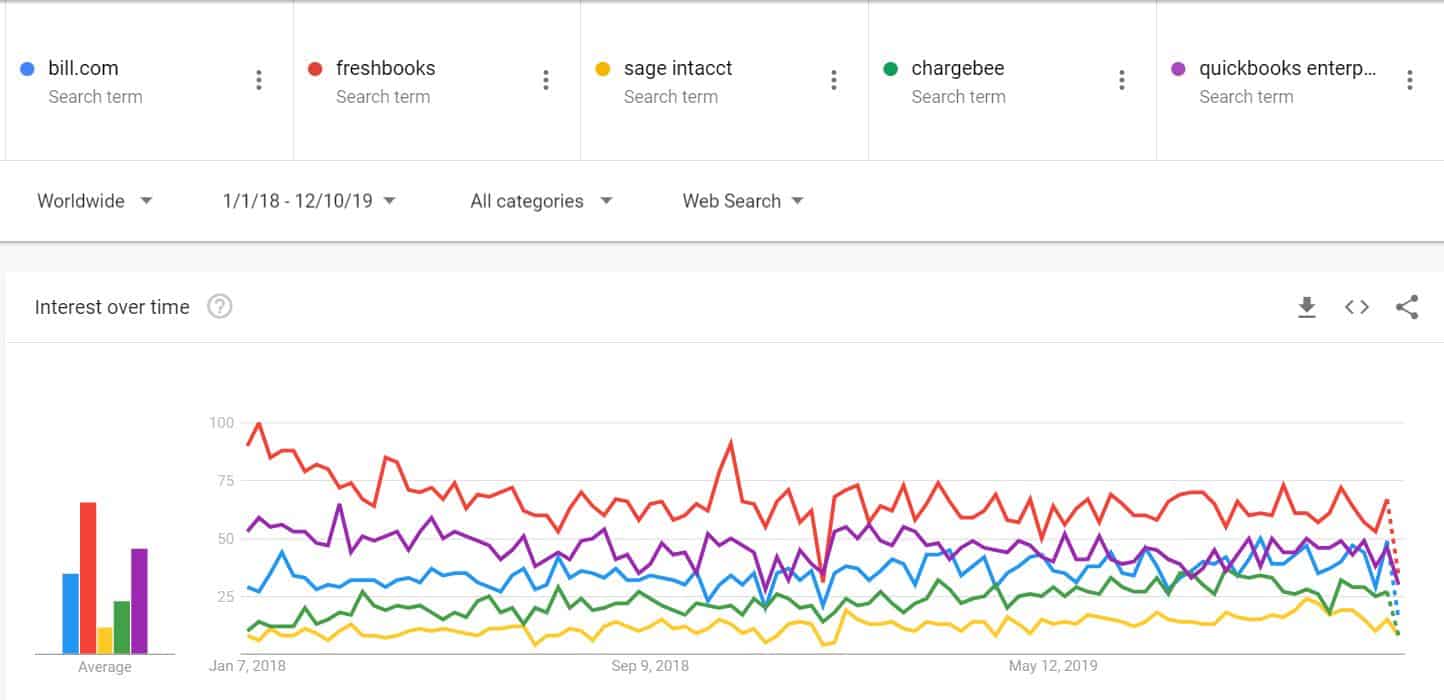

When looking at the popularity of Bill.com based on the number of Google searches, we can see clear market share gains over the last two years.

Bill.com has been gaining in popularity, especially at the expense of competitors Freshbooks and Quickbooks Enterprise.

The industry does appear to be getting more competitive with no one company looking like a clear leader.

Search Interest in Bill.com is increasing

Though Bill.com is obviously growing in popularity, after speaking with a long-time power user we have some concerns the company may be sacrificing customer service for the sake of profit.

This user reports the company recently got rid of live chat for customer service requiring problems to now be solved through email which takes at least a day compared to an instant resolution with live chat.

They also reported a recent cosmetic and user experience update to the website that made Bill.com harder to navigate.

Some alternative data backs up this user’s claim.

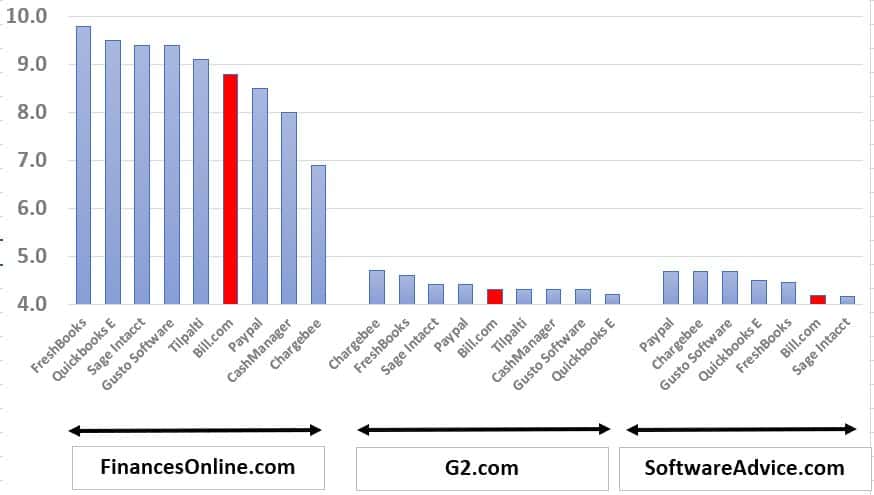

Looking at online user reviews, Bill.Com does not have many evangelists.

Though the service is popular, from the 33,000 reviews we compiled, users are just lukewarm on the user experience.

Compared to peers, Bill.com was rated average or worse than peers. On SoftwareAdvice.com, where most reviews were found, Bill.com ranked 8% below the average and came in second to last.

The user experience is critical to keep newly acquired customers.

Bill.com may be growing quickly today, but if customers don’t stick around, costs to acquire new users are going up and both revenue growth and profit margins are going down.

We would watch customer growth and acquisition costs closely for any signs of customer defections getting worse.

Bill.com User Reviews Only Average

Other Major Risk Factors

One other aspect of the business we think all investors should be aware of is how the company makes money on customer deposits.

When you use Bill.com to pay a bill or request funds from a client those funds are transferred into Bill.com’s bank account ahead of time to make sure the money will be available when it’s needed.

Bill.com takes this cash while it’s sitting around and invests it for their benefit, keeping the interest for themselves.

The interest is substantial, generating 20% of the company’s revenue in the last 12 months and contributing 30% of revenue growth.

This part of the business is susceptible to changing interest rates.

If interest rates go down, the company makes less money on customer cash and revenue growth will slow.

There is also the risk that regulations change or customers start pushing back against how long their funds can be held, in both cases decreasing the interest earned on customer funds.

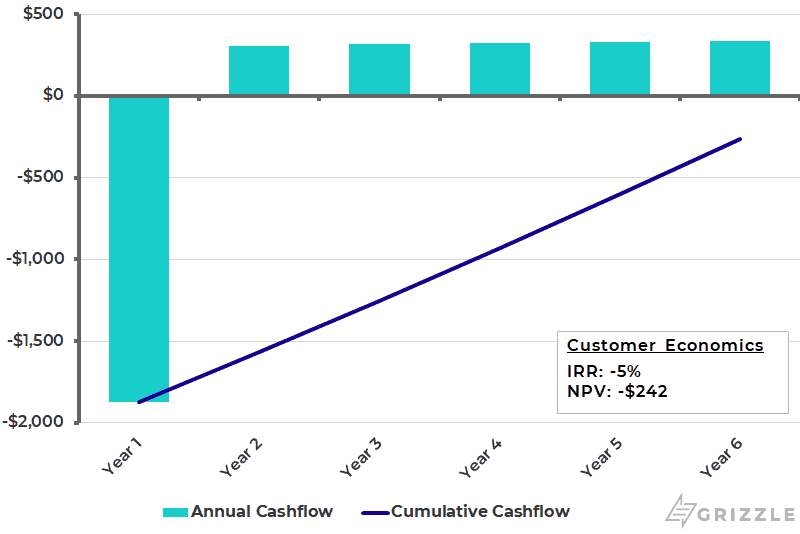

Customer Growth is Great but Customer Economics Aren’t

Bill.com is doing a good job signing up more customers and convincing customers to increase their usage of the platform.

Customers grew 20% in the last 12 months while revenue per customer grew an impressive 30%.

Offsetting this growth somewhat was customer acquisition costs which grew 44%.

Growth is great, but if you can’t make money on your customers Bill.com will never be able to turn a profit.

Bill.com says in the prospectus that the average customer relationship lasts 3-6 years.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Even if we assume every customer stays the full six years, Bill.com is generating a negative return over the 6 years of an average customer relationship as it stands today. [/su_panel]Current Customer Economics for Bill.com

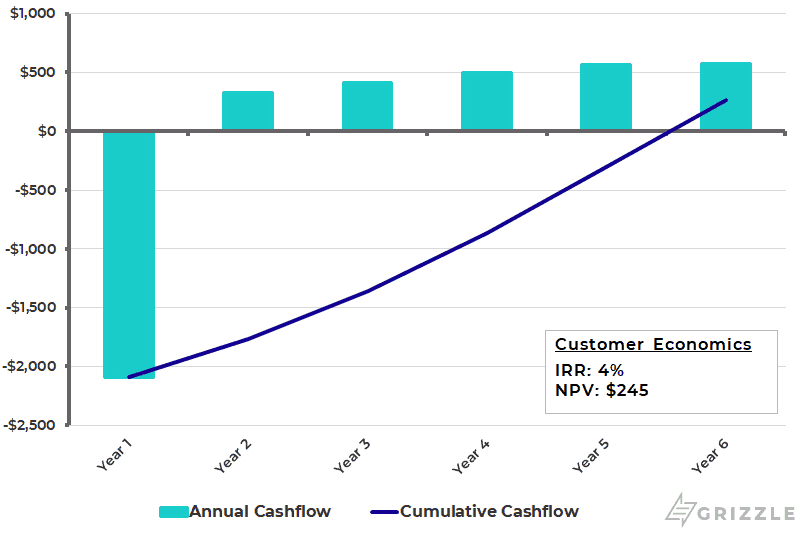

It is reasonable to assume there are economies of scale built into the business model so in the example below we gave the company credit for increasing revenue per customer, and falling per customer costs for payroll, cost of goods sold and research.

Even in this rosy scenario, the return on a customer is only 4%, not very attractive.

Bill.com will have to find a way to lower the advertising costs of bringing in a new customer while decreasing costs significantly across the board to generate a decent return on each customer long-term.

Bill.com’s growth is strong enough today that the stock will go up as the multiple rerates in line with peers, but if they can’t fix the customer economics of the business, investors will eventually realize and start ignoring growth and focusing on profit.

The stock won’t be above $20/sh for long if that happens.

Forecast Future Economics for Bill.com

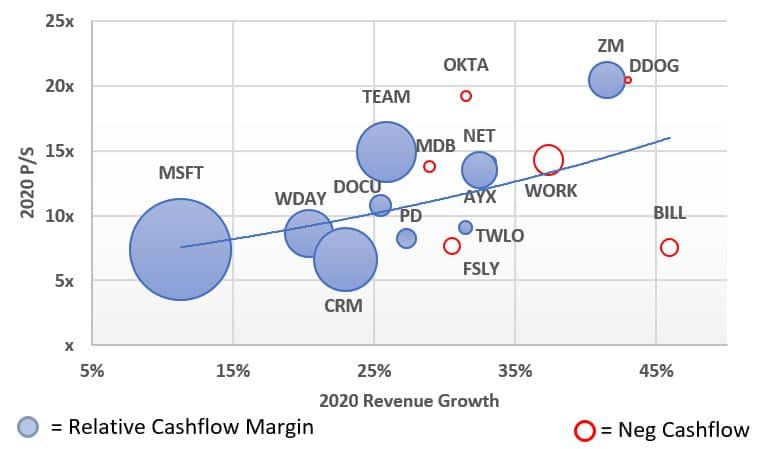

What is Bill.com Worth?

The expected IPO price of $19-$21 a share would value Bill.com at up to $1.5 billion.

Looking at where tech industry peers are trading today, Bill.com looks downright cheap at only 7.5x next year’s revenue.

Bill.com should grow revenue by 45% in 2020, which implies at least a multiple of 15x, 100% higher than where this stock is planning to go public.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Given the cheap valuation vs peers and industry-leading revenue growth, we expect to see some fireworks on the first day of trading. We would not be surprised to see the stock hit $30/sh or higher on the first day of trading. [/su_panel]Bill.com is Cheap for How Fast Revenue is Growing

Share Unlock, Float and Other Details a Trader Needs to Know

Bill.com is planning to issue 10.15 million shares in the IPO, which would mean 14% of common shares outstanding will be free to trade while the other 86% will be locked up.

This is a similar float to most IPO’s we’ve covered this year.

Mark your calendars, 86% of the shares outstanding will come off lockup on either March 14th or May 14th, 2020 and can be sold into the open market.

Of these shares, 25% can be sold immediately while owners of the remaining 60% can’t sell more than 700,000 shares every 3 months.

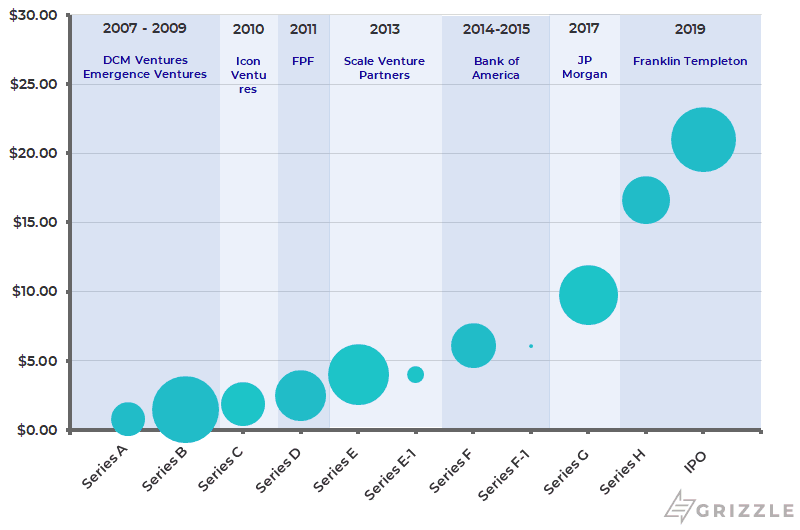

Cost Basis of Funding Rounds (Circle Size = % of Shares)

Insiders Bought Their Shares at $5.35 on Average

The expected IPO price of $21 will make many insiders very rich.

Management, investors and employees acquired their shares for $5.35 on average giving them 300% upside if they were to sell.

61% of shares have a cost basis of $4.00 or less and are looking at gains of 400%+.

What to Do With Bill.com Stock

Bill.com is riding a huge trend in the business world towards digitization.

As the average age of small business owners decreases, their desire for and willingness to embrace digital solutions is only going up.

Bill.com is going public as one of the fastest-growing tech stocks on the market and should command a premium multiple because of it.

We know demand is strong for this offering with the company increasing the IPO range by 18% already.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]This IPO feels very similar to DataDog earlier this year. That stock’s IPO price was raised 23% before it began trading and ended the first day up 40%. [/su_panel]The stock of Bill.com will continue to screen cheap in our view until it hits around $35/sh or above, 66% above the IPO price.

As usual with IPOs, we don’t expect much value to be left for individual investors on day 1, but investors should keep this stock on their radar and look to initiate a position if the share unlock or other catalysts cause the share price to decline back to the low $20s.

Or if you’d like us to track it for you, subscribers to Grizzle will receive free alerts if the stock hits our buy price or runs into a speedbump that makes it no longer investable.

SUBSCRIBE TO GRIZZLE and Invest Smarter

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.