Private credit is the booming asset class, an asset class which has done a brilliant job taking advantage of the market opportunity provided by the heavy regulation of the US commercial banking sector following the 2008 financial crisis.

Still private credit has yet to be stress tested in a down cycle.

On that point, this writer’s attention was recently drawn to the most comprehensive analysis of the industry seen so far.

That is a chapter titled “The rise and risks of private credit” contained in the IMF’s recently published biannual Global Financial Stability Report (see IMF Global Financial Stability Report: “The Last Mile: Financial Vulnerabilities And Risks”, April 2024).

The IMF report raises a number of interesting issues.

First, that private credit on account of its growth has become of macroeconomic importance and, therefore, has the potential to “amplify negative shocks to the economy”; though this writer would also add that it has the potential to act as a trigger for shocks to the economy.

Second, it notes that the data required fully to analyse the risks of the asset class is unavailable, though, to be fair, the report concedes that these risks “appear contained at present”.

Third, among the various risks the report highlights are “relatively fragile” corporate borrowers, increased exposure of pension funds and insurance companies to the asset class, a rising share of semi-liquid investment vehicles, multiple layers of leverage, “stale” valuations, and what it calls “unclear interconnections” between participants.

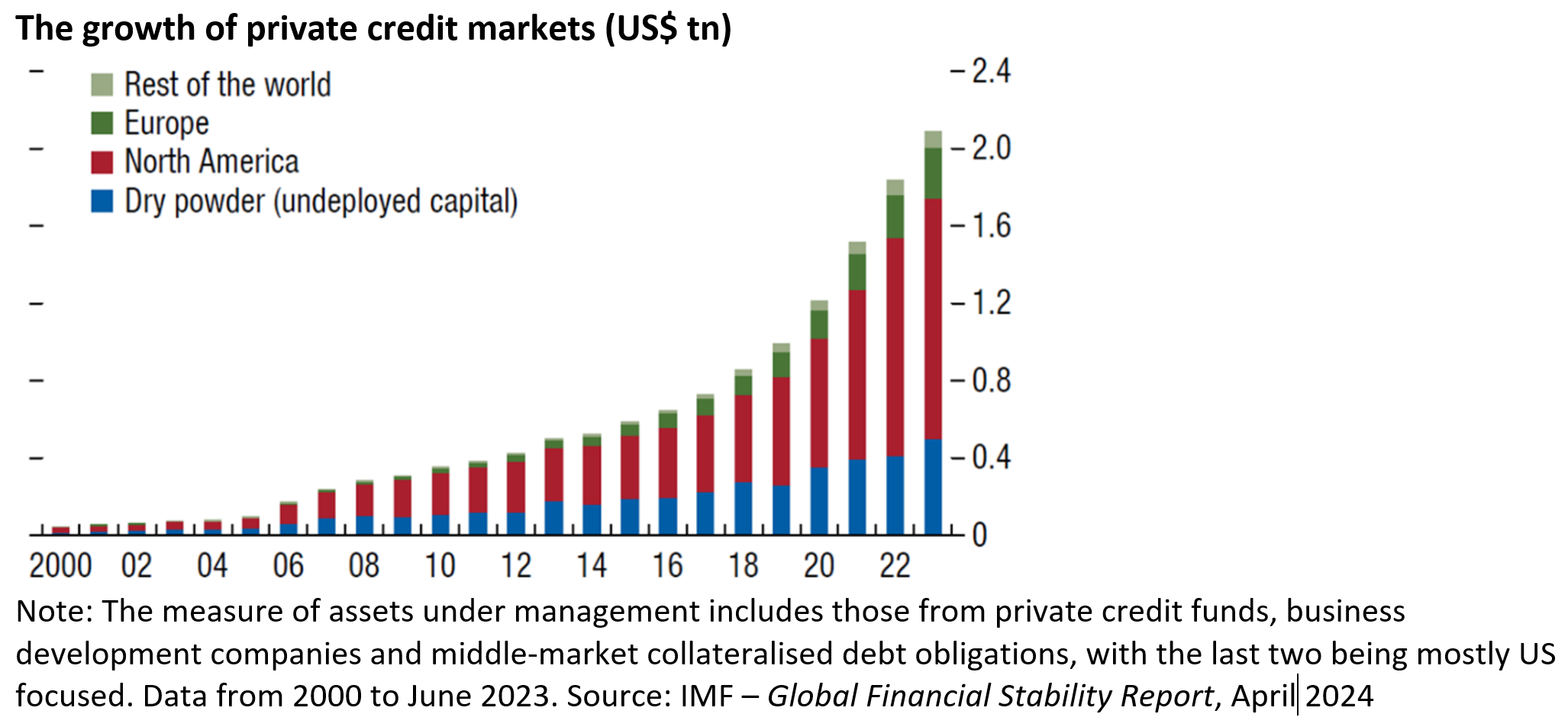

In terms of actual hard data, the IMF estimates that private credit assets totaled US$2.1tn at the end of 2Q23, comprising both combined assets and yet-to-be-deployed capital commitments, a figure which equates to about three-quarters of the global high-yield bond market.

Out of this total, America dominates, accounting for about US$1.6tn, where the asset class has been growing at an average 20% annual rate over the past five years.

Private credit now accounts for 7% of the credit extended to nonfinancial corporations in the US, which is comparable with the shares of syndicated loans and high-yield corporate bonds.

By contrast, its share in Europe is only 1.6%, and in Asia a mere 0.2% of credit extended to nonfinancial corporations.

Private Debt is Fully Intertwined with Private Equity

Meanwhile, in terms of who is active in private credit, managers whose umbrella firm is also active in private equity hold more than three-quarters of private credit assets.

While for about 70% of private credit deals, the borrowing company is sponsored by a private equity firm.

In this respect, there is a close if not circular relationship between private credit and private equity. Meanwhile, the IMF report notes that one attraction for borrowers of utilizing private credit is that it “avoids the disclosures and costs associated with public markets”.

This is a reference to the regulatory arbitrage with the commercial banking sector in America since the 2008 financial crisis in terms of the massively increased financial regulation imposed on the commercial banks after that event.

This writer has written here before about how private equity is negatively geared to rising short-term interest rates (see Tracking Three Risks That Could Sink Markets: Oil, Geopolitics and Private Debt, 13 May 2024).

On that point, the IMF report notes that private credit is typically floating rate and caters to “relatively small borrowers with high leverage”.

Such borrowers could perform poorly in a downturn, particularly in a “stagflation scenario”, which is what markets will start to worry about the more the “no landing” outcome for the US economy becomes more consensus.

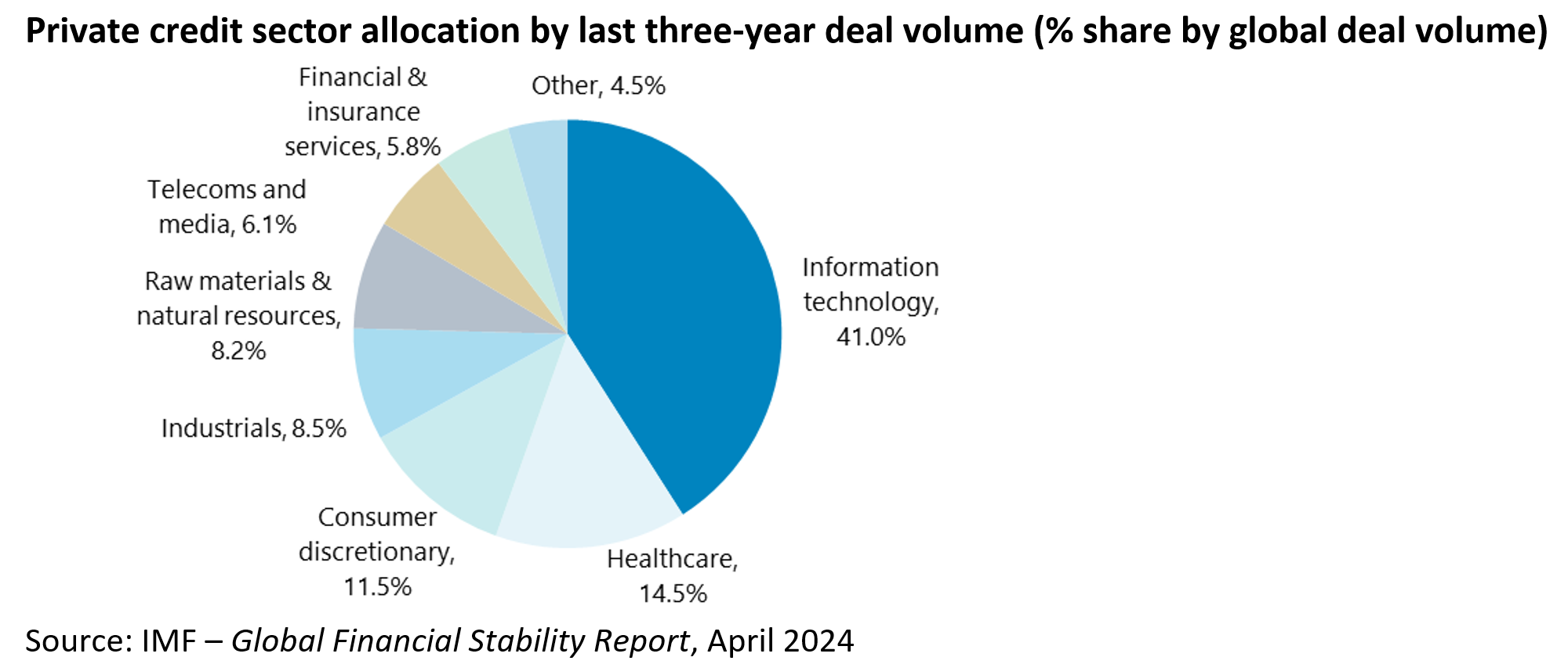

In terms of sectoral exposure, the report notes that the health care and information technology sectors are overrepresented in private credit.

As regards the above-mentioned interconnections, the IMF report details how private credit is a key funding source for firms sponsored by private equity.

On this point, it is standard practice for private equity “sponsors” to seek to enhance returns for their investors by increasing debt on the balance sheets of the firms they acquire.

Another statistic highlighting this interconnectedness is that 81.2% of private credit funds by assets also manage private equity funds, according to the same IMF report.

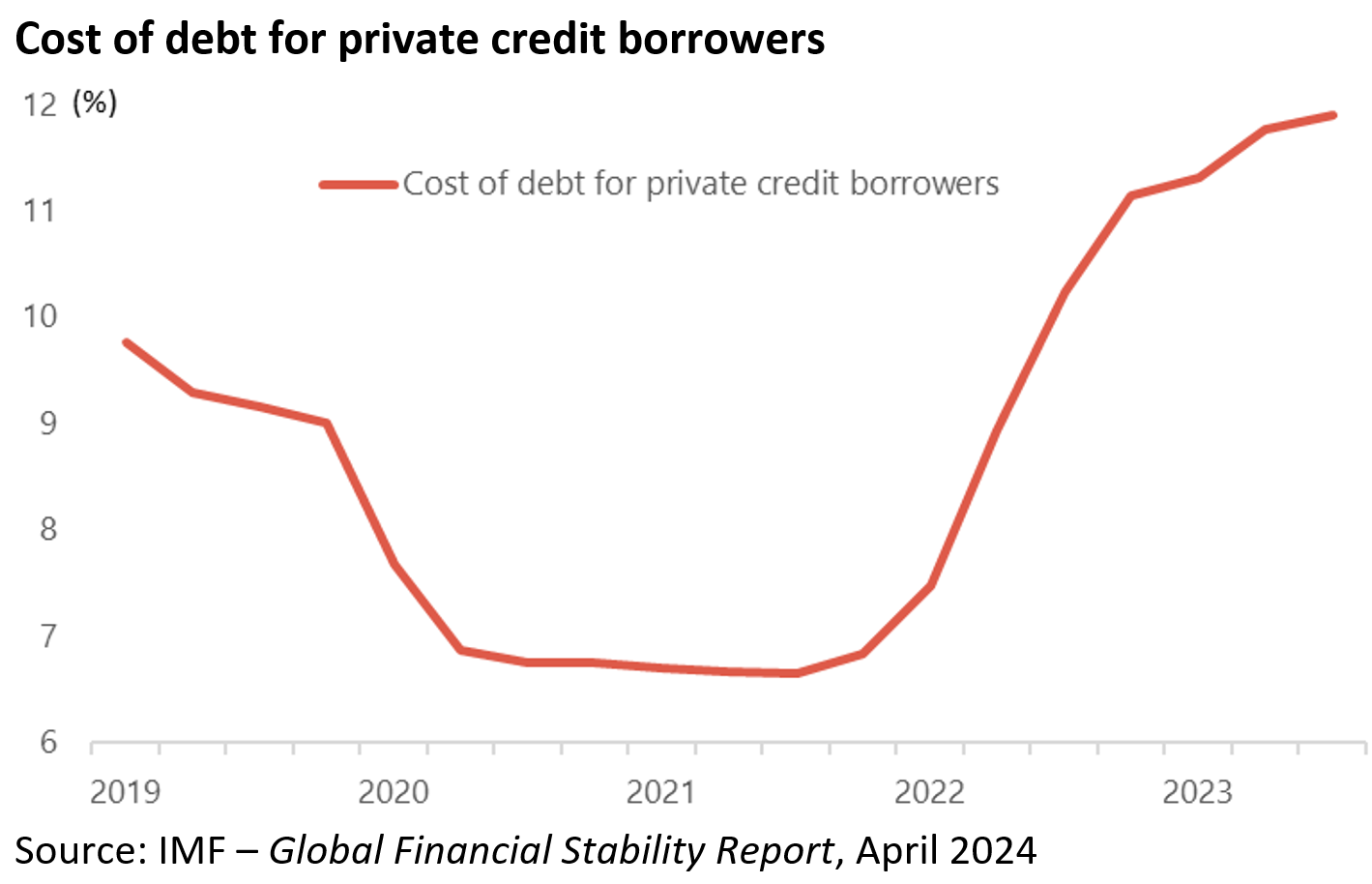

Meanwhile, the report estimates that the average cost of debt for private credit borrowers is 11.9%.

That, as already noted, is well above the prevailing level of nominal GDP growth. US nominal GDP rose by 5.4% YoY in 1Q24.

In terms of policy proposals, the IMF recommends, unsurprisingly, an effort to reduce the regulatory arbitrage between banks and private credit, in terms of a “more intrusive supervisory and regulatory approach to private credit funds, their institutional investors and leverage providers”.

Meanwhile, it remains extraordinary that the likes of pension funds, insurance companies, and family offices have for years been pouring money into locked up investment vehicles, such as private equity and private credit, at the same time as it has become by all accounts extremely hard to raise money for actively managed (as opposed to passive) equity and fixed income bond products, which offer much greater liquidity.

It is probably only a matter of time before this approach to investing will be questioned, if no discredited altogether.

For it depends on an illusion of liquidity which does not really exist, as reflected in the rising number of private equity owned companies that have yet to be sold.

Still, as noted here on several occasions in the past, the financial engineering skills of the private world are never to be underestimated in terms of their ability to keep the game going.

But that is much easier to keep doing in a world where interest rates are declining, not rising.

Meanwhile, the best explanation for the private asset classes’ growing popularity in recent years is probably less the stated returns than that the people employed to allocate the money have not had to worry about a monthly mark-to-market, as would be the case with more conventional funds investing in liquid markets, be it in equities, bonds or commodities or a mixture of all three.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.