I’m still hopeful, as are financial markets, that some sort of trade deal can be agreed between the U.S. and China in the current quarter. Still there’s a risk that domestic U.S. politics makes this more complicated. One issue of the moment is the current impeachment process and whether the Democrats will be able to get 20 of the 53 Republican Senators to vote against Donald Trump. This would seem a very tall order.

Trump’s Approval Ratings: What the Numbers Say

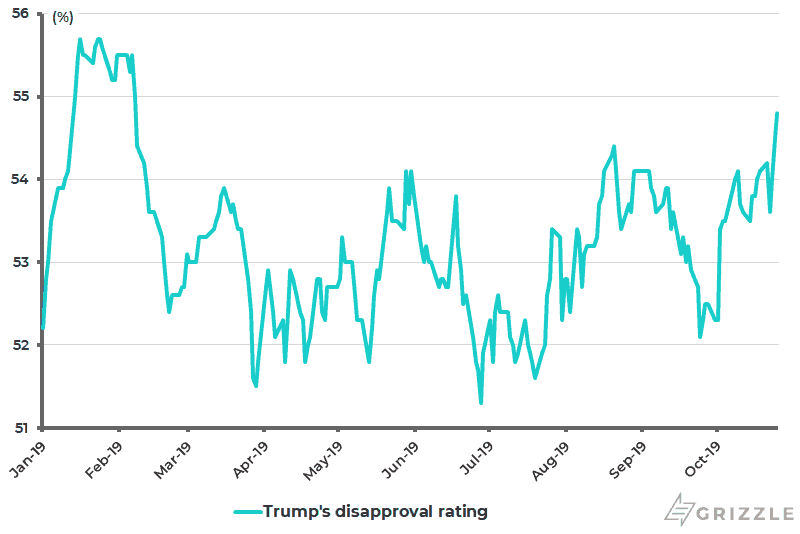

It is now necessary to refocus on Trump’s ratings. The disapproval ratings of the 45th American president are rising, which is a potential cause for concern. Trump’s average disapproval rating has risen from 52.1% in late September to 54.8%, the highest level since February (see following chart).

U.S. President Donald Trump’s Average Disapproval Rating

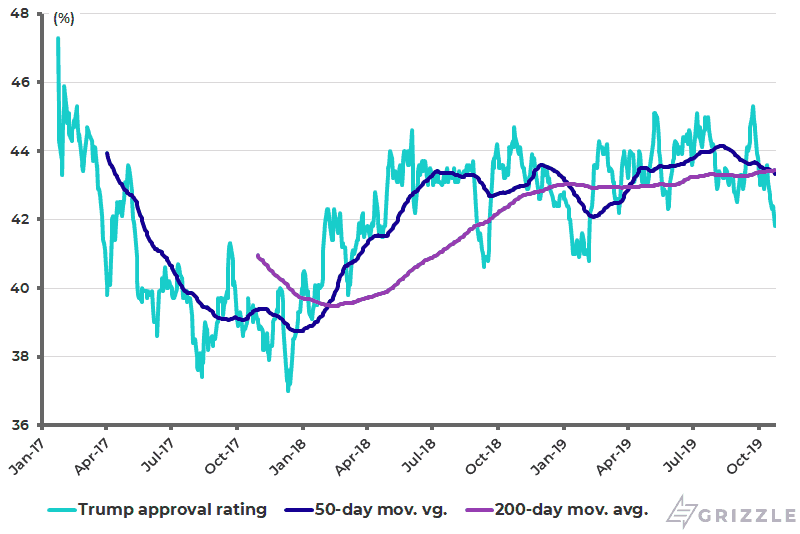

U.S. President Donald Trump’s Average Approval Rating

A positive point is that Trump’s approval rating (41.8%) remains in the same range it has trended since mid-2018 (see chart above), reflecting the solid nature of his core support. Meanwhile, for financial markets the issue is what does all this mean, if anything, for the U.S.-China trade talks where there remain hopes that Trump and Xi Jinping can agree to some form of deal when they’re due to meet at the APEC meeting in Chile scheduled for Nov. 16-17.

With an Election Coming Will a China Deal Be Struck?

If there have been positive developments of late in terms of renewed talks between the two sides this month, there has also been threatening noise from Washington-based China hawks. One example is talk of ordering U.S. government pension funds to stop buying Chinese stocks (see Bloomberg article: “White House Focuses on China Stock Limits in Retirement Fund”, Oct. 8, 2019). Another is a threat to kick China out of benchmark bond and stock indices. This would be highly provocative and would definitely trigger Chinese retaliation.

The base case remains that Trump will want a deal before raising the threatened tariffs in December on US$160 billion of Chinese imports of mostly consumer goods, a move that would seem extremely risky from the standpoint of the American economy. It’s also the case that it makes sense for China to try and secure a deal with Trump now rather than facing a perhaps more anti-Beijing opponent after November 2020. That China has not given up on a deal is clear from the fact that it has still not published its so-called “unreliable list”.

Meanwhile the combination of the spectre of Elizabeth Warren on the horizon, with her detailed policies targeting corporate America, and the unpredictable nature of The Donald re his stance on trade and tariffs, is likely to lead to continuing weakness in U.S. corporate investment. This leaves the U.S. economy running on consumption and government spending, though there has now to be a growing risk that wage growth has peaked.

U.S. Economics and the Impact on Business and Consumer Confidence

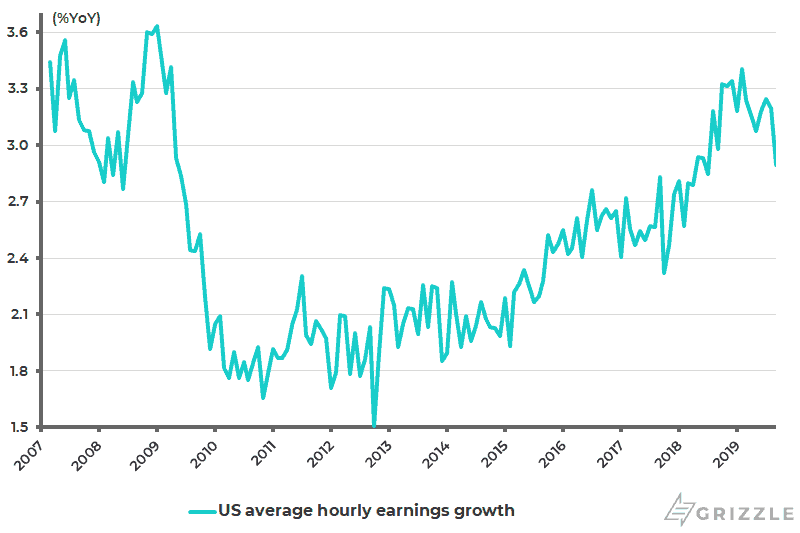

U.S. average hourly earnings growth slowed from 3.2% YoY in August to 2.9% YoY in September, the lowest level since July 2018 (see following chart). It’s also worth noting that the small business confidence index, which reached an all-time high in August 2018, continues to lose momentum.

U.S. Average Hourly Earnings Growth for all Private Employees

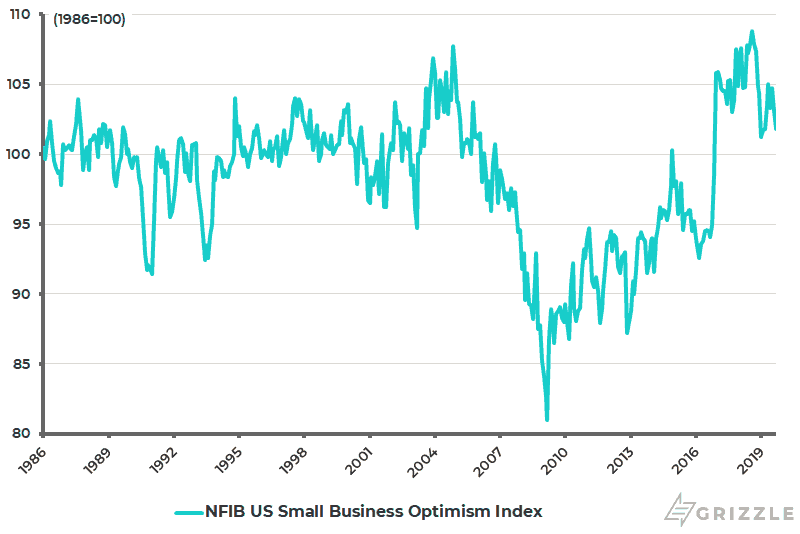

The NFIB Small Business Optimism Index has declined from a recent high of 105 in May to 101.8 in September, the lowest level since March, and is down from the peak of 108.8 in August 2018 (see following chart).

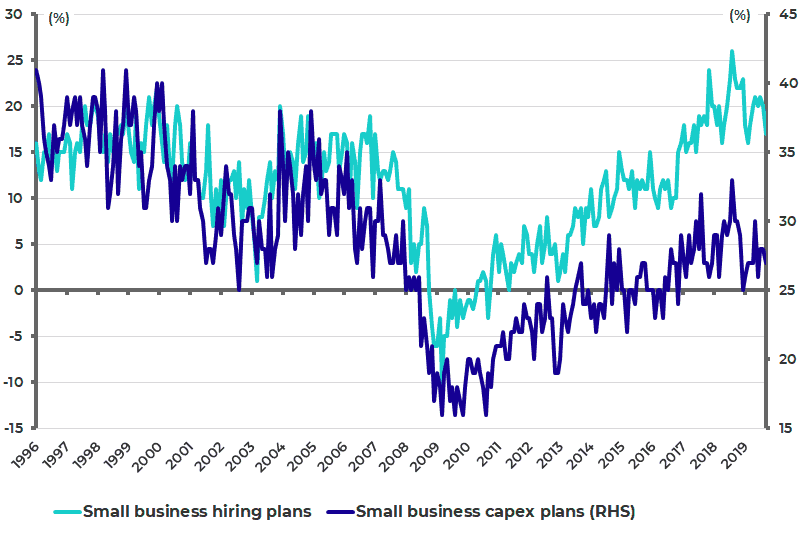

The hiring plans sub-index declined from the peak of 26% in August 2018 to 17% in September, the lowest level since February. The capex plans sub-index also fell from 33% in August 2018 and 28% in August 2019 to 27% in September (see following chart).

NFIB U.S. Small Business Optimism Index

NFIB U.S. Small Business Survey: Hiring Plans and Capex Plans

The key question for the U.S. economy, and indeed for the global economy, is now whether the long-observed weakness in manufacturing related data will start to impact service sectors. Or whether increasing monetary easing globally will revive activity before there is a proper downturn that extends beyond manufacturing. In this respect, there is no doubt that the uncertainty triggered by the trade war and the related reality of increased tariffs has impacted manufacturing sectors.

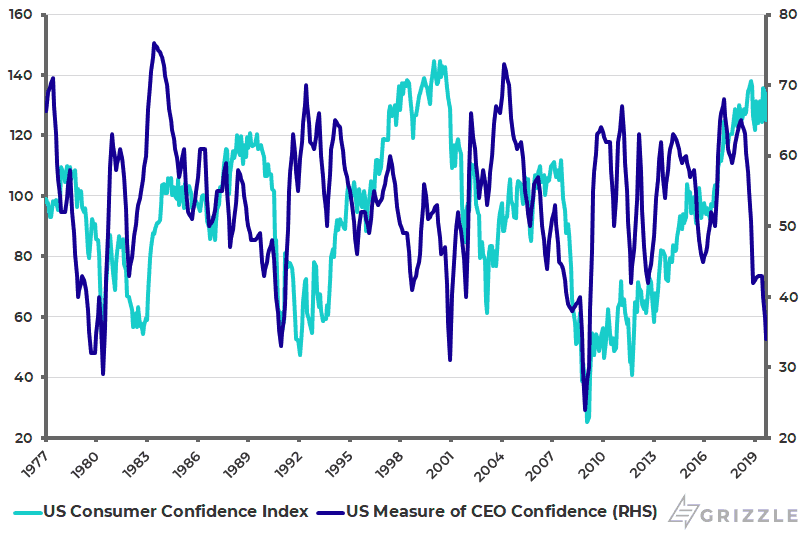

The above question is highlighted by the historically wide divergence between still buoyant U.S. consumer confidence and the marked decline in confidence on the part of major U.S. corporates. True, the Conference Board’s U.S. consumer confidence index declined by 9.1 from 134.2 in August to a three-month low of 125.1 in September. But it remains within the range it has been over the past two years and is significantly above the 2016 low of 92.4. By contrast, the Conference Board’s U.S. CEO confidence index has collapsed from a recent high of 68 in 1Q17 and 43 in 2Q19 to only 34 in 3Q19, the lowest level since 1Q09 (see following chart).

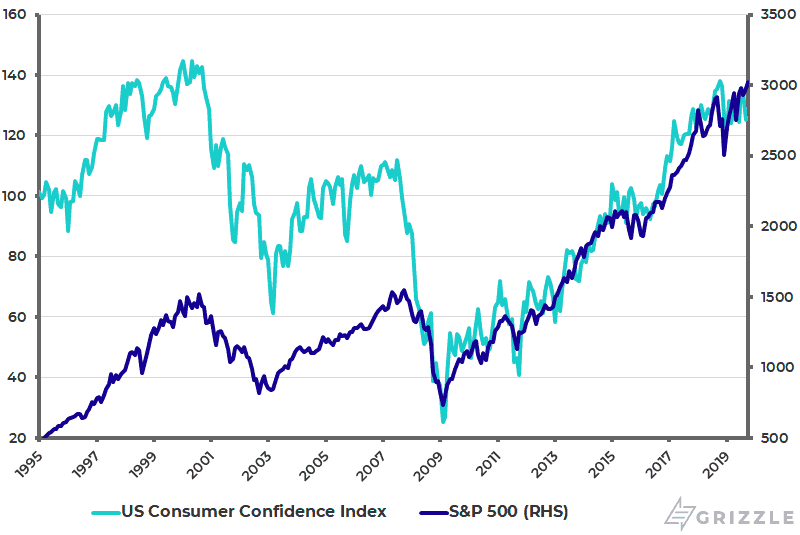

The base case is that the corporate sector is much more likely to prove the lead indicator, most particularly as U.S. consumer confidence historically has tended to go up and down with the U.S. stock market (see following chart).

The Conference Board U.S. Consumer Confidence Index and Measure of CEO Confidence

U.S. Consumer Confidence Index and S&P500

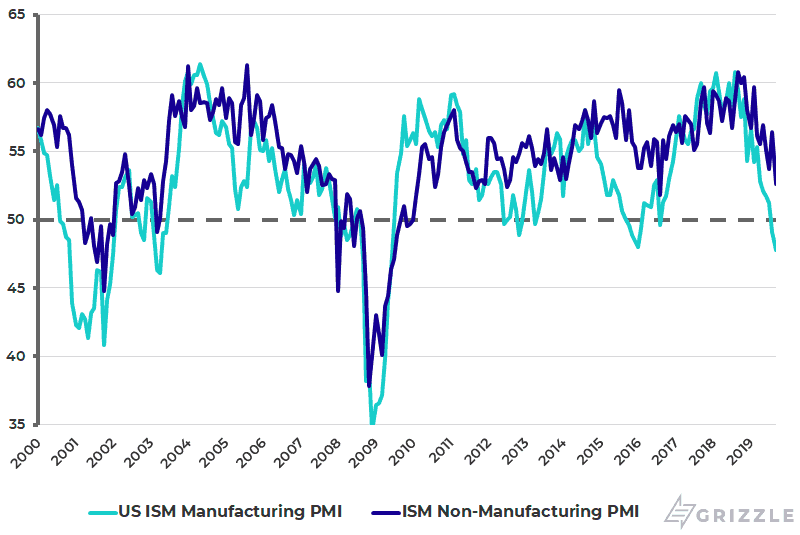

Still the ISM manufacturing PMI gave a false recession signal in 2015/2016. The same could be happening again. That said, it remains the case that the latest downturn in the ISM non-manufacturing PMI has made the chart look more negative from a growth perspective than was the case in 2016, suggesting that the prospects for a more clear-cut U.S. downturn are rising, though far from conclusive. Thus, the ISM non-manufacturing PMI declined from 56.4 in August to 52.6 in September, the lowest level since August 2016 (see following chart). Meanwhile, the manufacturing PMI also declined from 49.1 in August to a 10-year low of 47.8 in September.

U.S. ISM Manufacturing PMI and Non-manufacturing PMI

Meanwhile, it is worth noting that ECB President Mario Draghi presided over the last ECB meeting this week of his eight-year term. He departed amid some controversy with one third of the 25 ECB policy members reportedly criticizing the ECB’s decision in September to renew quantitative easing, the greatest dissent ever in the 21-year old history of the ECB. This criticism was not without reason since Eurozone data is simply not as weak as the narrative being peddled by the consensus, with the major exception of German exports.

Still, despite such legitimate dissent, the media spin has been to hail Draghi’s final actions as impressively aggressive. Almost no one has raised the obvious negative point that Draghi has failed to exit unconventional policy, as was hoped by both him and the consensus at the start of the year in the sense that quantitative easing in the Eurozone was assumed to have ended. In that sense, Draghi has failed as he has never met the official 2% inflation target.

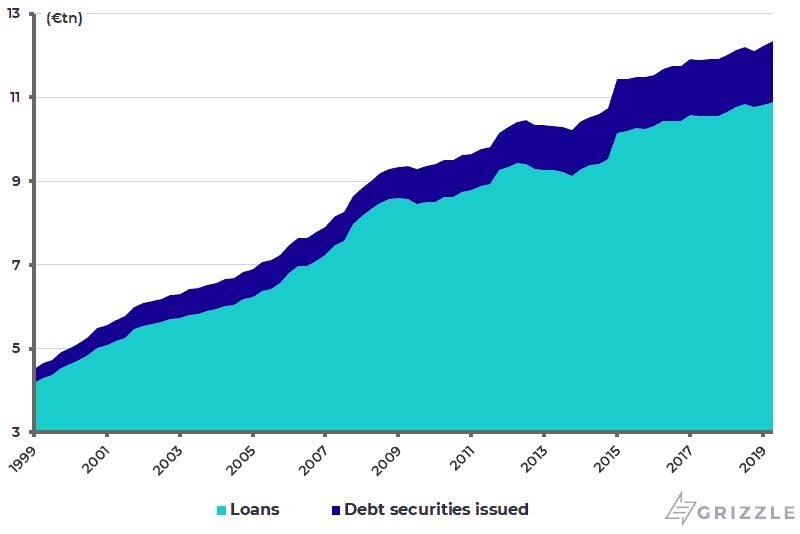

No one has also explained why making interest rates more negative (now minus 0.5%) is positive when it is widely agreed that negative interest rates are negative for banks and the Eurozone remains as primarily dependent as ever on bank credit. Loans to Eurozone non-financial corporations totalled €10.9 trillion at the end of 2Q19, compared with €1.4 trillion in debt securities issued (see following chart).

Eurozone Non-financial Corporations: Loans and Debt Securities Issued

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.