The news flow over the past few weeks has not supported hopes that there is a better chance of a trade deal with China than currently envisaged by markets. China, for example, withdrew from scheduled trade talks the day after Washington activated tariffs on US$200 billion of Chinese goods (Sept. 24). Yet all hope should not be abandoned.

North Korea – Donald the Peacemaker or Neocon?

This is because of the personality of the 45th American President. Donald Trump likes to make a deal on a one-to-one bilateral basis and he likes to be the centre of the action. This is what attracts him to the North Korean situation where the South Korean President Moon Jae-in is now doing a good job acting as the chief lobbyist for Kim Jong-un in stark contrast to his less impressive management of the South Korean domestic economy.

It also should be noted that 17 businessmen from leading chaebol groups accompanied Moon on his three-day visit to the North Korean capital Pyongyang three weeks ago. This is supportive for the view that a North Korean investment cycle could be “in play” and it is one which Beijing should approve of since it does not involve Korean unification. Indeed special economic zones in North Korea are a perfect development model for the Korean chaebol, though it should be assumed for now that there would be no German-style wage unification.

At this juncture, the main obstacle to Kim Jong-un‘s undoubted ambitions to modernize the North Korean economy is the Washington national security lobby represented by the likes of National Security Advisor John Bolton. This is why it is very important, in the case of both North Korea and China trade, whether Trump is really another national security hawk or whether he is just using the hardliners’ stance as leverage to “make a better deal”.

There is nothing in the Donald’s history to suggest he shares these “neo-con” obsessions. Indeed he is more of an isolationist. Now it is possible that Trump has been captured by the military-industrial complex in his 21 months spent in Washington. But this seems unlikely. In which case, an undoubtedly street smart Trump must surely understand that the North Korean leader is not going to close down every nuclear facility he has before America has even signed a peace treaty. Indeed North Korea stated on Oct. 2 that an end-of-war declaration “can never be a bargaining chip” to get the country to denuclearize, according to the state media Korean Central News Agency.

Will Trump’s China Trade Bashing Backfire?

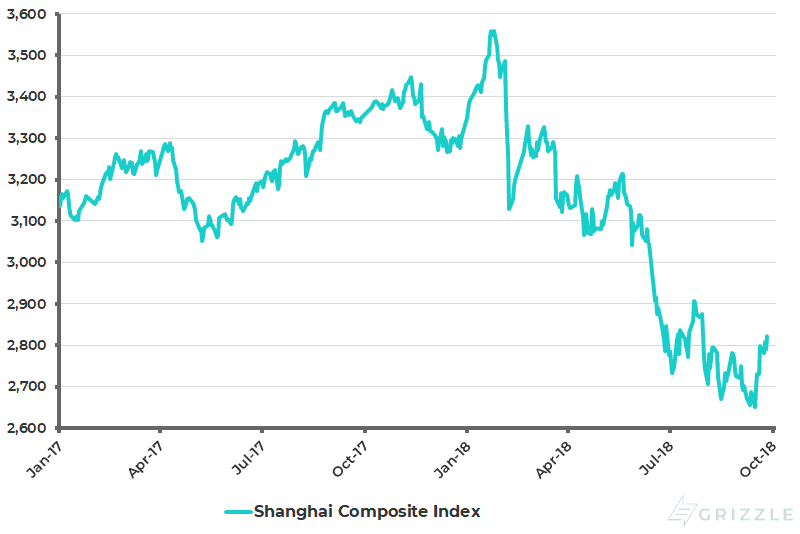

Similarly, on China, at some point Trump needs to close the China bashing trade and take a profit. Otherwise there is a growing risk that it backfires on him. This is because implementation of tariffs is more likely to act as a retail tax on American consumers and as a squeeze on American importers than inflict a major hit to the Chinese economy. There is a risk that Trump believes he has more leverage than he actually does because he has bought into the line that China’s economy is collapsing as reflected in the sell-off in the mainland’s stock market this year (see following chart). That this is a possibility is suggested by Trump’s public references of late to the negative performance of the Chinese stock market.

Shanghai Composite Index

If the above is indeed the case it means Trump is at severe risk of overplaying his hand. It has long been the case from this writer’s personal observation that the biggest bears on China globally reside in New York and Washington and, so far at least, they have always been wrong in their forecasts in a period spanning more than two decades. The reality today is that China, as a domestic demand-driven economy, is now much better positioned to withstand a “trade war” than Trump appears to believe. It is also the case that the A share market has been correcting more on domestic deleveraging issues than “trade war” concerns as discussed here last week.

The other point to make again about Trump and trade is that the track record supports U-turns in the sense that, in the case of Mexico, Europe, and Canada this past week, confrontation turned into seeming “deals”. Yet it is far from clear that these deals met the policy objectives of the protectionist lobby inside the Trump administration. Still, it is quite possible that the trade warriors in Washington are happy to make concessions with everyone apart from China.

Saying ‘No’ to Iranian Oil

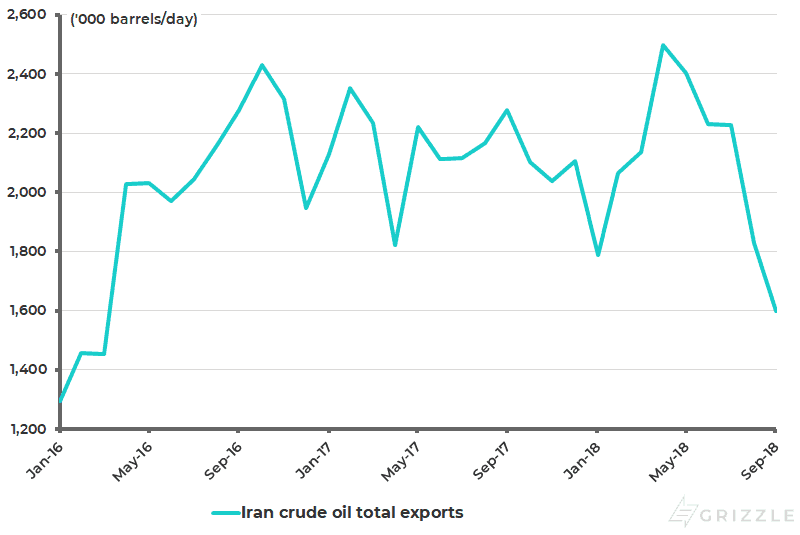

Meanwhile, there is another area where Trump is not backing down as yet and where he is still following the national security hawk agenda. That, of course, is the extraordinary demand that the world should stop buying Iranian oil by Nov. 4. For now it seems that the world is seeking to adhere to this edict. Witness India’s recent announcement that it will stop buying Iranian oil by November and India has been Iran’s second largest customer for oil after China. The same conclusion is also suggested by the sharp decline in Iranian oil exports. Iran’s total crude oil exports declined by 30%YoY to 1.6m barrels/day in September, the lowest level since March 2016 (see following chart), with exports to China, Europe, and Asia down 17%, 44% and 27% YoY respectively in September.

Iran crude oil exports

But this again is another example of where policy can backfire on Donald Trump since the US policy towards Iran is only putting further upward pressure on oil, which is heading much higher for reasons previously discussed here, unless demand suddenly collapses in the emerging world, and so far there is little sign of this. A further surge is the oil price above the current level of US$84 will act as a inflationary tax on American consumers’ discretionary incomes.

Brent crude oil price

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.