The Wuhan novel coronavirus has, unsurprisingly, become the main focus of financial markets. With the Shanghai stock market having just reopened this Monday after the Chinese New Year holiday, the base case must be that a panic sell-off lies ahead even if the virus burns itself out on a three-month view when the weather turns warmer, as was the case with SARS in 2003.

Coronavirus Probably Worse than Government Lets on

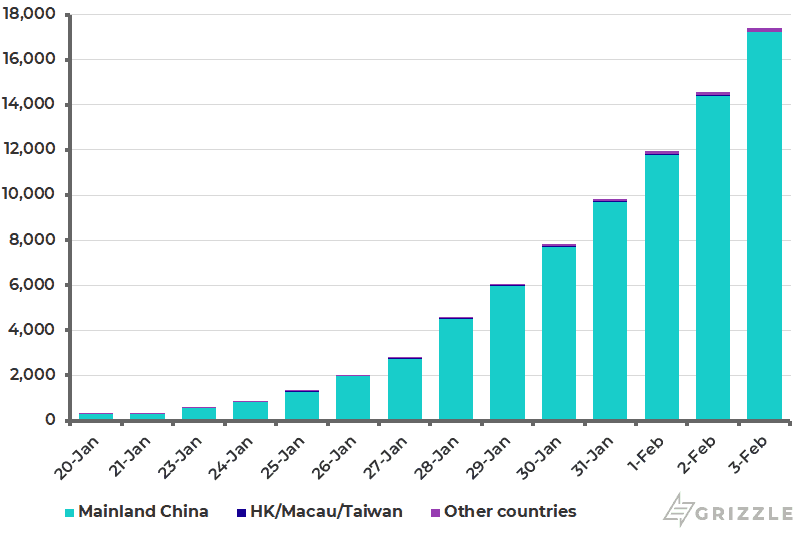

There are two main points of concern. I first heard about reports of the Wuhan-based virus in mid-December from reports on the Chinese internet. This means it probably began in November which raises the risk that the number of cases is significantly higher than the current official tally of 17,205 cases in mainland China and 17,387 cases worldwide (see following chart). The second point of concern is that the number of Chinese travelling abroad is up tenfold in the 17 years since SARS.

Resident departures rose from 16.6 million in 2002 to 162 million in 2018 (see following chart). If these are the negatives, the main positive is that the percentage of cases where the infected person died so far remains relatively low at 2.1%, compared with the mortality rate of 9.6% for SARS. It should also always be remembered that an estimated 290,000-650,000 people die of flu globally each year, according to the World Health Organisation (WHO).

Wuhan Novel Coronavirus Situation (Number of Confirmed Cases)

Good Time to Buy Chinese Stocks

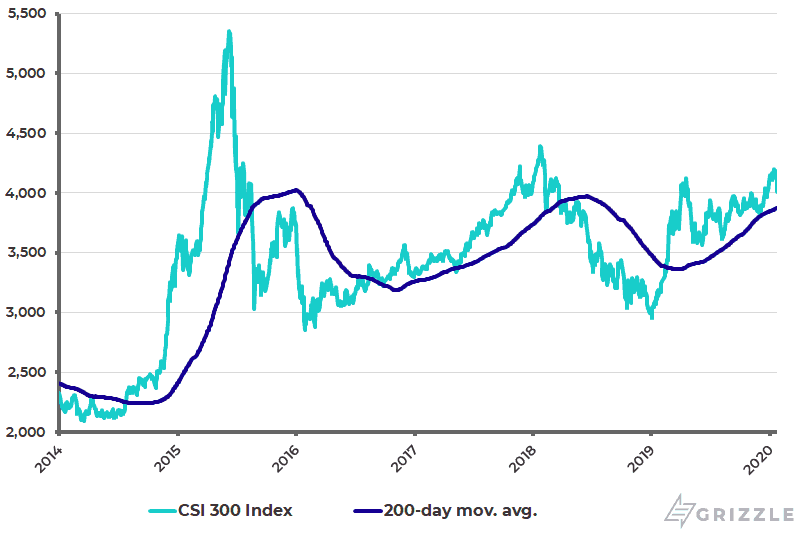

Meanwhile, from an investment standpoint, the virus is viewed as a three-month opportunity to add to exposure in China in terms of a stock market which was breaking out technically after a three-quarter consolidation when the virus newsflow hit. The base case is that the China A share market made a major low at the start of last year when deleveraging peaked in terms of intensity (see following chart).

Meanwhile, for macro investors wishing to trade the virus, or hedge a long equity portfolio, I recommend buying Eurodollar futures. This is because any panic sell-off is likely to lead to a rise in Fed easing expectations. Still if the virus newsflow proves less of a concern, then the current consensus view, namely that the Fed will remain on hold, will prevail. This was also the stance confirmed by the Fed meeting this week.

China CSI 300 Index (A shares)

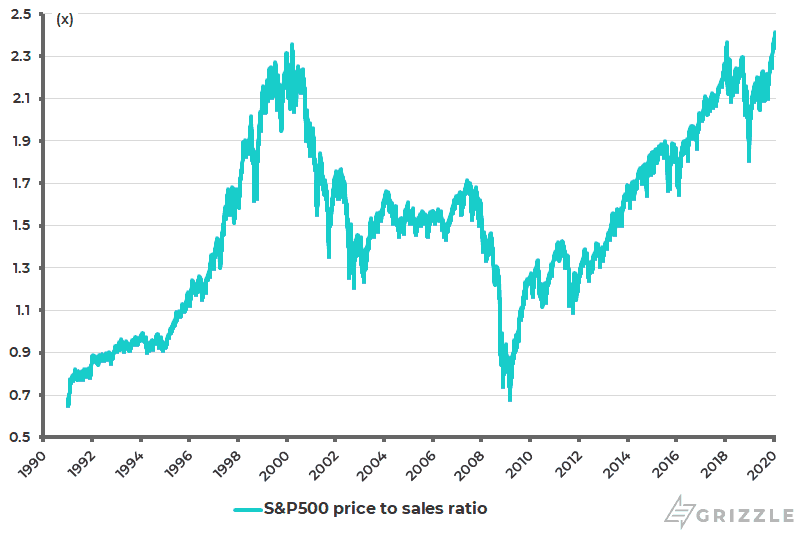

Meanwhile the virus risk aside, the biggest positives for Wall Street-correlated world stock markets in 2020 are continuing Fed balance sheet expansion and hopes of a more doveish interpretation of the inflation target as a result of the Fed’s pending strategic review. The biggest negative is that the S&P500 ended 2019 trading at a record high valuation relative to sales (see following chart).

S&P500 Price to Sales

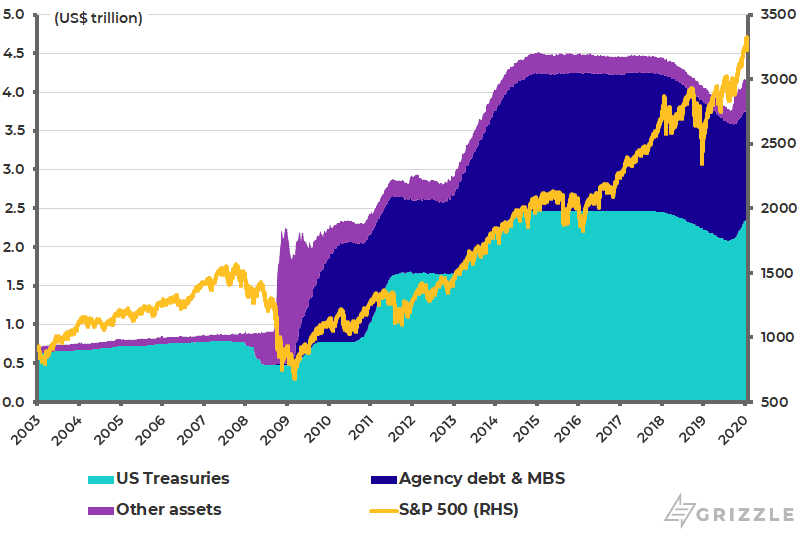

Continued Balance Sheet Expansion

When it comes to monetary policy, it is hard to exaggerate its importance for stock markets, most particularly in the short to medium term. Clearly, the key development last quarter occurred on Oct. 8 when Fed chairman Jerome Powell announced that the Fed would start expanding its balance sheet again soon. It is also the case that the Fed has stated that it may maintain this balance sheet expansion, currently at a pace of US$60 billion a month, until June this year before reviewing the policy. To be precise, the Fed stated on Oct. 11 that it will:

If the buying is maintained at the current pace of US$60 billion per month, that would imply the balance sheet reaching US$4.45 billion by the end of June, the highest level since December 2017, up from US$4.15 billion at the end of January. Still it should be noted that it is not certain if the Fed will maintain this initial pace of US$60 billion until 2Q20.

The above picture of renewed Fed balance sheet expansion is the “risk on” context in which to view the 8.5% rally in the American stock market in the last quarter of 2019 and the 3.1% rally earlier this month before the virus news hit sentiment (see following chart).

Federal Reserve Balance Sheet and S&P500

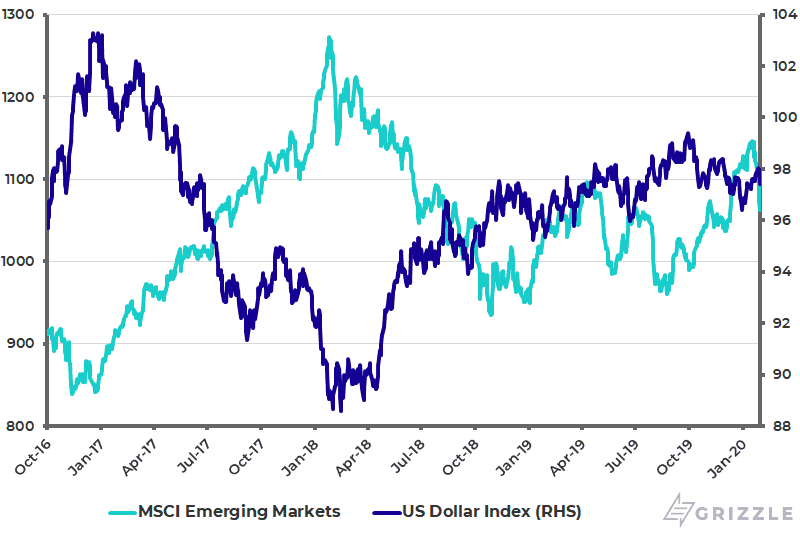

The key question now, especially for Asia and emerging markets, is whether this Fed policy triggers significant U.S. dollar weakness. The dollar had certainly begun to weaken before the coronavirus news created a renewed bid for the American currency.

It should be noted that there is a longstanding negative correlation between the U.S. dollar and emerging market stocks. The correlation between the U.S. Dollar Index and the MSCI Emerging Market Index has been a negative 0.85 since October 2016 (see following chart).

U.S. Dollar Index and MSCI Emerging Markets Index

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.