Will the Market Force Powell’s Hand on Negative Rates?

One assumption Grizzle has been making of late is that the Federal Reserve will not countenance a formal move into negative rates by cutting the federal funds rate to below the current target range of 0-0.25%.

Remember the ECB’s deposit facility rate is still minus 0.5%.

The above is worth mentioning since the focus has returned of late on a market-driven move into negative rates as US macro data continues to show extreme weakness while there is also the potential for reported inflation to turn negative.

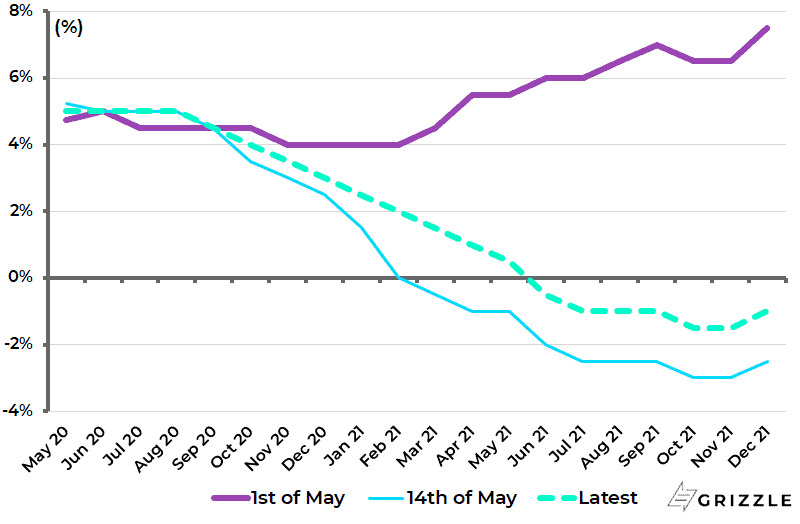

The implied yield of the July 2021 Fed funds futures, for example, declined to a negative 2.5bp on 14 May and is now at negative 1bp.

Fed Funds Futures Implied Yield

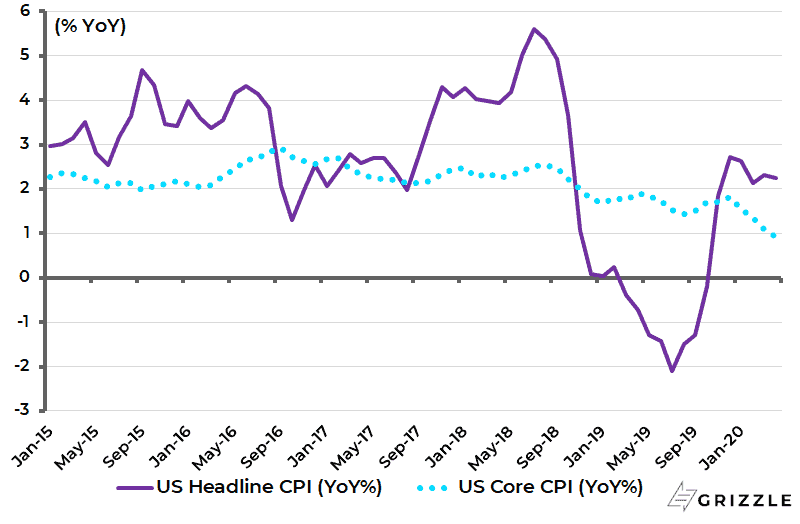

US headline and core CPI declined by 0.8% and 0.4% MoM respectively in April and were up only 0.3% and 1.4% YoY, down from 1.5% and 2.1% YoY in March.

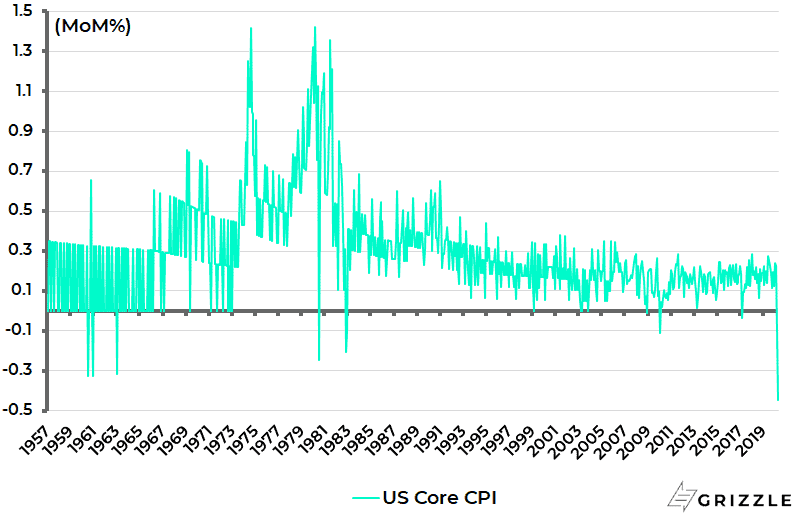

This was the biggest monthly decline in core CPI since the core CPI series began in 1957.

U.S. Headline & Core CPI Inflation %YoY

U.S. Core CPI %MoM

Negative Rates in the Eurozone have Been a Policy Dud

It is, therefore, of note that that Fed governors have been making comments recently implying continuing resistance to negative rates.

Most importantly, Fed chairman Jerome Powell said at the Peterson Institute for International Economics on 13 May, commenting on the subject of negative rates, that “for now it’s not something that we’re considering”.

For the man who bought the world the “Powell pivot” at the start of 2019, it is not insignificant that he used the phrase “for now”.

Still it should be assumed for now that the resistance of the current Fed to negative rates is the result of the negative experience of what negative rates have achieved, or rather not achieved, in the Eurozone.

Or at least that is this writer’s charitable assumption, though it is still possible to find monetary theorists, or cranks, who believe in the theoretical positives of negative rates. See, for example, the IMF working paper published last year (“Enabling Deep Negative Rates to Fight Recessions”, 29 April 2019 by Ruchir Agarwal and Miles Kimball).

Still, it is also the case that the pressure for negative rates will rise if the US starts reporting falling prices because the monetary cranks will focus on rising real rates.

Meanwhile, any formal move by the Fed into negative rates will open up the potential for Treasury bond yields to turn negative.

If negative rates will continue to be resisted in America, for now and hopefully forever, it is another reason why the Fed has been willing to contemplate other unorthodox approaches in terms of the dramatic policy response to the Coronavirus, in terms of both unlimited quanto easing and monetary-financed fiscal facilities.

Remember the Fed is to receive a US$454bn equity injection from the Treasury’s Stabilisation Fund with a plan to leverage that 10:1 implying US$4.5tn of buying power.

This has the potential to cause the Fed balance sheet to grow to US$10tn by the end of this year.

The Next Iteration of Unorthodox Policy: Yield Curve Control

In this respect, in line with the Fed’s willingness to countenance more unorthodox approaches, it also remains quite likely that the Fed will try, sooner or later, to fix long term government bond yields.

This raises the issue of both when such yield curve control will be implemented and how.

In terms of when it could be implemented, the obvious time is when markets begin to focus on the potential for cyclical recovery and the return of pent-up demand.

This would likely lead to selling pressure on the long end of the bond market.

Still, it is also the case that the Fed might choose to be pre-emptive by fixing yields before such pressure came on the long end.

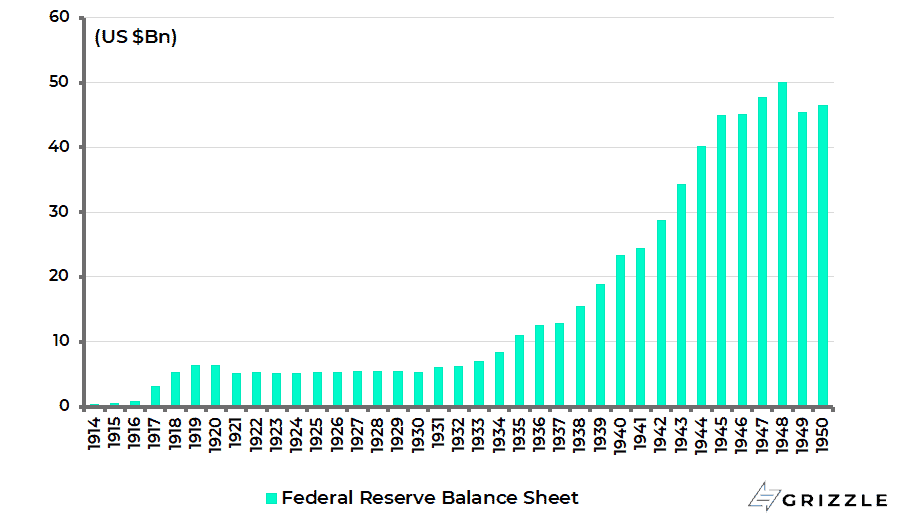

The last time the Fed fixed Treasury bond yields was during the Second World War, resulting in a period of extended monetisation of debt.

The Fed capped the yield on long-term Treasury bonds at 2.5% in 1942 while pegging the short-term Treasury bill yield at 0.375%.

The T-bill yield was raised in 1947 but the cap on the long-term bond yield was kept until 1951. The Fed balance sheet rose from US$15.5bn at the end of 1938 to a then peak of US$50bn at the end of 1948.

Federal Reserve Balance Sheet (1914-1950)

Does Yield Curve Control Let the Inflation Genie Out of the Bottle?

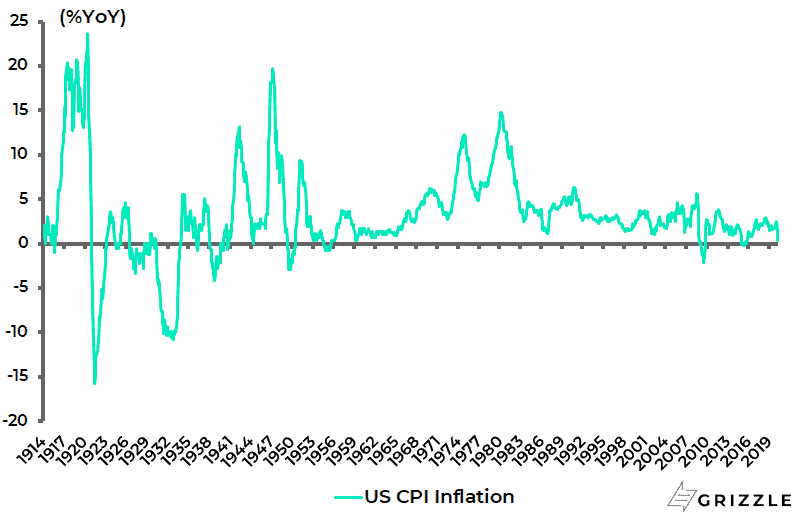

The practical consequence during the 1940s of such monetization was a pickup in inflation.

US CPI inflation rose from 0% in May 1944 to a peak of 19.7% YoY in March 1947 after the Second World War

U.S. CPI Inflation Since 1914

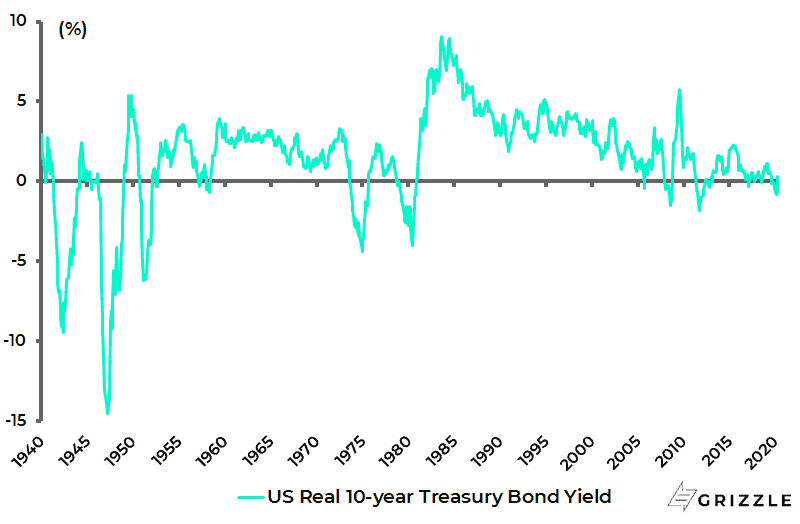

The consequence for investors was therefore a real decline in the value of their government bond holdings, a trend which continued in the post-1945 period.

Real 10-year Treasury bond yields, for example, averaged a negative 3.2% in the period between 1941-1951.

U.S. Real 10-year Treasury Bond Yield (deflated by CPI inflation)

The Death of the Bull Market in Bonds

All of the above is laying the foundations for the beginning of the end of the 39-year bull market in Treasury bonds.

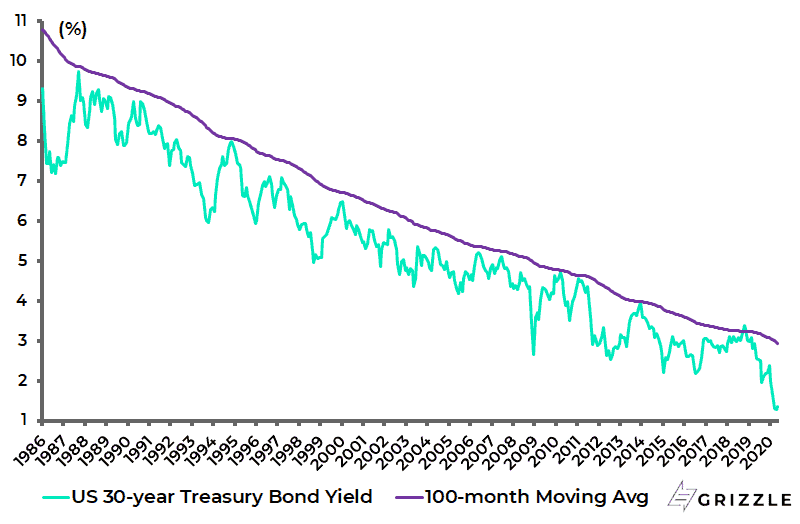

In this respect, an interesting monthly chart of the 30-year Treasury bond yield which shows the relationship between the bond yield and its 100-month exponential moving average (EMA), which gives greater weighting to most recent data.

U.S. 30-year Treasury Bond Yield (Monthly chart w/ 100-month exponential moving avg)

The chart shows the tendency for Treasury bonds in a bull move to peak, or bottom in yield terms, when the yield reaches its 100-month EMA. But, interestingly, in this last move in March when the 30-year Treasury yield reached a low of 69.9bp there was an acceleration beyond the exponential moving average.

It is an axiom of technical analysis that long bull markets normally end in a climactic peak or, in chartist jargon, an “acceleration”.

This writer is no technical analyst but this type of chart pattern is what should be expected if the 39-year bull market in Treasury bonds is really coming to an end.

But if Pivot Powell does another pivot and decides to cut the federal funds rate to minus 3%, for example, it may work out differently by sending Treasury bond yields into negative territory.

Inflation is the End Outcome, With or Without Negative Rates

Anything is possible given the Fed’s monumentally over-the-top response to Covid-19.

Still, even in the event of an outright Fed move into negative rates, this writer still believes the ultimate consequence of such extreme monetary policy, when combined with growing monetisation, will be inflationary.

This is despite the fact that that a long term disinflationary, if not deflationary, view of the world has been maintained here since the mid-1980s.

Anyone who doubts this can look up this writer’s first book published in 1988 (“Boom and Bust: The Rise and Fall of the World’s Financial Markets”, Sidgwick & Jackson, 1988).

Since then the view has been consistently maintained that government bonds have remained in structural bull markets.

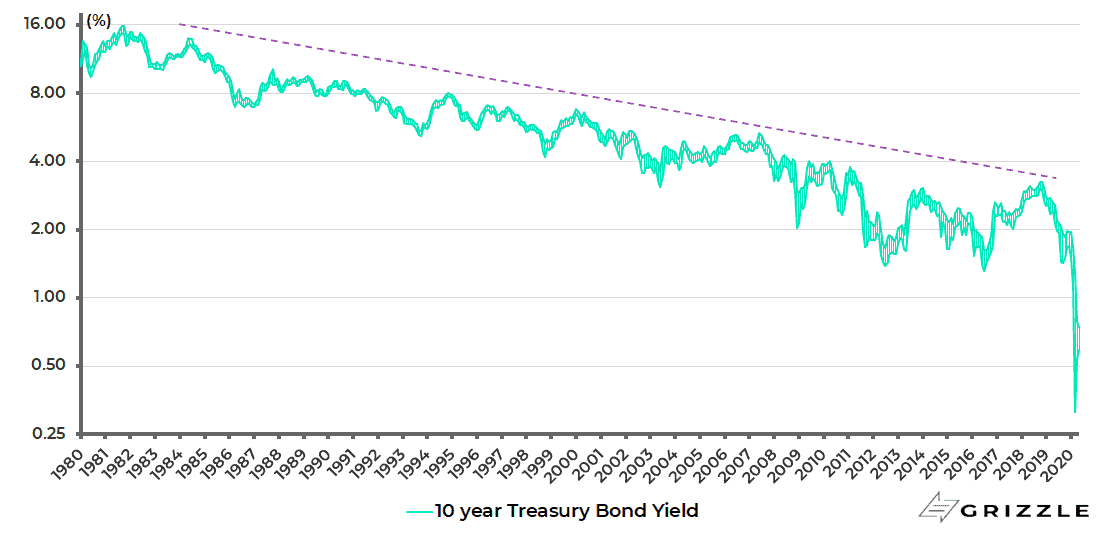

This has also been the message conveyed by the chart all investors should be obsessed with, namely the trend line in place since the start of the bull market in 1981 in the ten-year Treasury bond yield.

Clearly, confirmation of that trend line being broken would require the ten-year yield to break above that trend line which is currently at around 3.0%.

U.S. 10-year Treasury Bond Yield

Still if the Fed, sooner or later, fixes the ten-year at a yield below that trend line, such a formal confirmation may take longer to happen.

Meanwhile, the assumed coming fixing of government bond yields is yet another reason to own gold and, in the case of equity investors, gold mining stocks, on a long-term basis.

That topic will be returned to another week.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.