Bottom Line

Organigram Holdings (NASDAQ: OGI; TSE: OGI) posted what looked like a strong quarter as the company smashed analyst expectations, but in reality, results were only returning to levels last seen two quarters earlier.

Investors should be very careful buying into the stock’s rally tomorrow as there are some concerning trends going on under the surface.

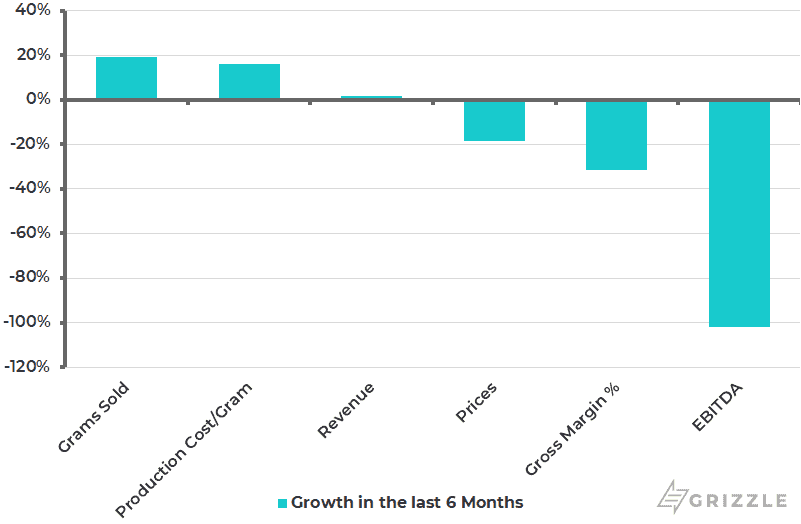

- The company saw pricing fall 20% in only one quarter!

- Revenue caught back up with levels from six months ago but the gross margin and EBITDA margin are both down 30%-100%.

- 6 months of cash left even if they max out the loan facility from BMO. May need to dilute shareholders by another 10% through their share issuance program if more money is needed.

- Sales in the rec market are down 40% from six months ago even as the overall market grew by 70%!

- OGI had to push ~40% of sales into the wholesale market at discounted prices, does this signal consumers have soured on OGI flower?

All of these problems tell us OGI is a broken stock under the cannabis 1.0 regulations.

With cannabis 2.0 products already rolling out to stores OGI needs these products to sell through or else the stock is going lower.

The stock is up big in after-hours trading making these earnings one of the best examples of investors’ inability to see the forest for the trees.

Without a long cash runway, OGI is on the clock to put up big profits in the first six months of cannabis 2.0.

OGI Results vs Six Months Ago Don’t Look so Hot

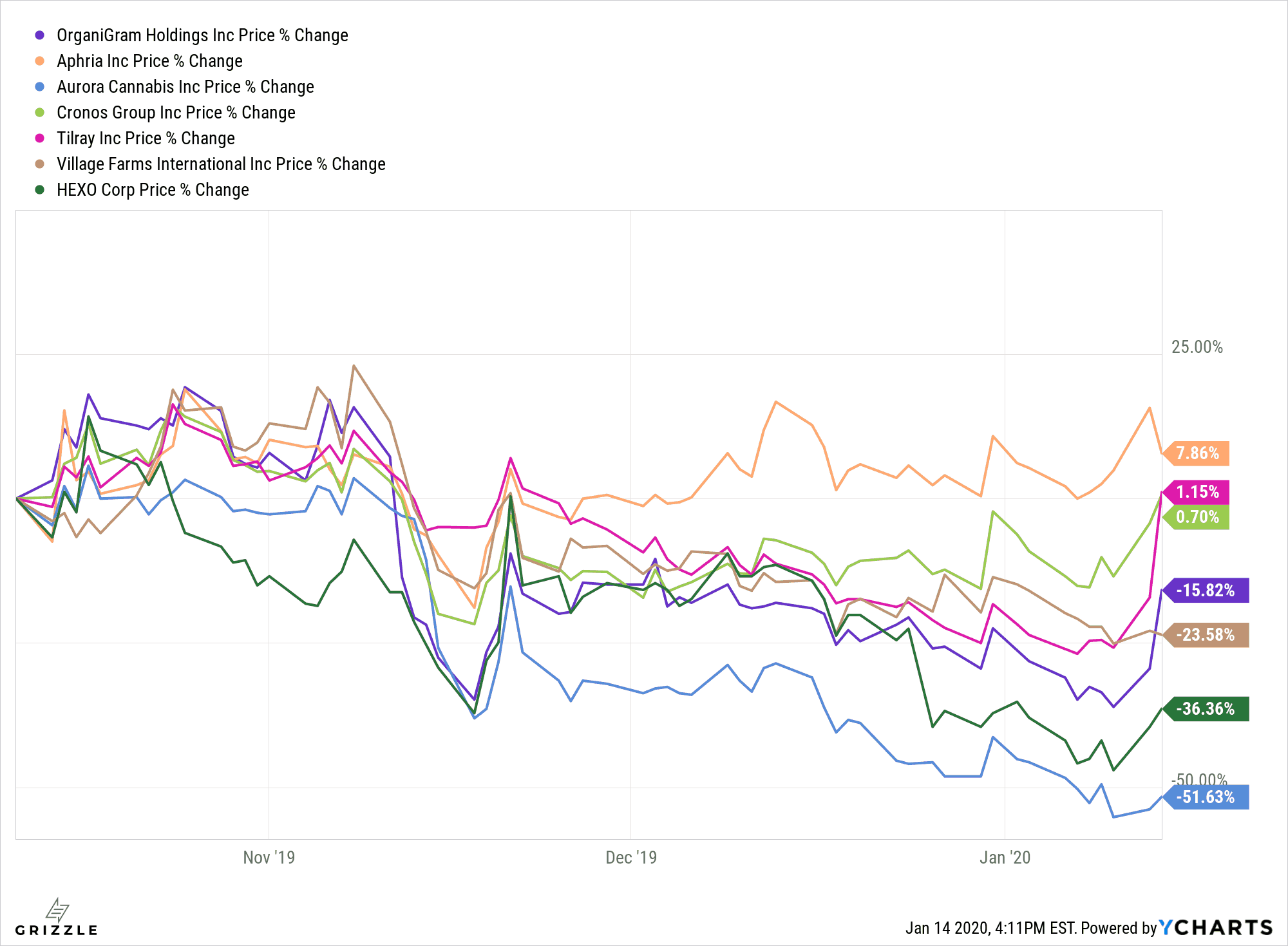

A chart of price changes (%) of OGI before the earnings report today, shows that in the past quarter the stock has been hammered by the market, much like many other players in the industry.

Part of the poor performance was likely due to the company’s share issuance program as 7 million shares were issued in the quarter, likely putting downward pressure on the stock.

Three Month Price Change (%) – OGI Has Been Underperforming

Operational Overview

The company posted a net revenue of $25.2 million, more than double their net revenue in the same quarter last year which came in at $12.4 million. This beats analysts’ estimates which was at $14.9 million.

The company posted a gross margin of $9.3 million (37%) and an adjusted EBITDA of $4.9 million.

EPS came in at $0.00 which beat the analysts’ consensus estimate of -$0.02

Revenue per gram fell sharply this quarter as the company had to resort to selling their dried flower wholesale just to find a buyer for their cannabis.

Continued large sales into the wholesale channel will have us concerned about true demand for the OGI product.

Revenue Per Gram of Cannabis Produced

Production cost per gram fell from $5.4/g last quarter to $2.9/g this quarter. This represents a 46% reduction in per gram production costs, however, costs are still up 16% from six months ago.

Production costs per gram returned to normal levels after an unusually high-cost quarter last quarter due to merchandise returns.

With inventory adjustments and write-offs behind them, investors should be looking for continued downward progress in growing costs as we move into Cannabis 2.0.

Production Costs Per Gram of Cannabis Produced

We saw gross margin per gram increase 11% from $1.5/g to $1.7/g quarter over quarter but fall 30% from six months ago.

OGI has work to do as it sits in the bottom half of the pack on gross margins.

Gross Margin Per Gram of Cannabis Produced

The SG&A cost per gram was down 64% compared to last quarter.

This is good news as this may be an indication that OGI has effectively streamlined their business to further reduce cost. The numbers from this quarterly report put OGI’s SG&A cost per gram among some of the lowest in the industry.

SG&A Cost Per Gram of Cannabis Produced

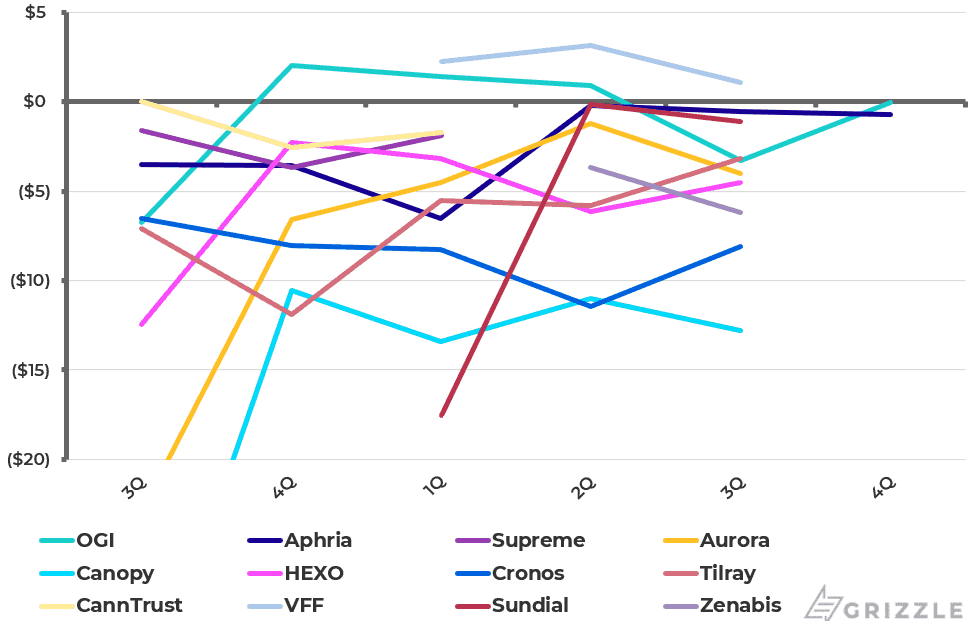

The latest data puts OGI’s EBITDA per gram at -$0.01/g just slightly above Aphria’s -$0.74/g which just released their earnings report as well. It is worth noting though that both companies still generate negative EBITDA per gram. This means that neither company is generating any profits on a per gram basis just yet.

EBITDA Per Gram of Cannabis Produced

Get Ready for Potential Cash Issues

OGI has $57 million of cash right now and would max out at $87 million if they draw down the rest of their secured facility with BMO.

This is good for only 6 months of cash runway at the current burn of $47 million a quarter including debt repayments.

The company estimates there is $36 million left to spend to finish all current construction projects so the $47 million burn rate could decline after next quarter, however they also estimate another $33 million may be needed for other opportunities.

If they end up in a cash crunch a few months from now there is a $25 million revolving credit facility they can draw on, but this facility has limits based on receivables and is only short term.

The company also can raise another $32 million by issuing 15 million shares from their treasury stock program though that would dilute current stockholders by another 10% at the current stock price.

Bottom line, OGI does not have the luxury of time and needs cannabis 2.0 results to be explosive.

In our opinion investors would be better served if they either sat on the sidelines for six months or moved their money to a cashed-up LP like Aphria until there is more clarity on OGI’s cash liquidity situation.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.