Pushing on a string is a term this writer became very familiar with employing when living in Tokyo in the early 1990s and monitoring the slow-motion deflation of the Japanese asset bubble.

The phrase then became much more widely employed in the aftermath of the US housing bust in the late 2000s.

The phrase is normally applied best in asset deflation cycles where an excess of private sector indebtedness reduces the potency of monetary easing.

Still, it also comes to mind monitoring the increasingly frantic efforts of Chinese policymakers to stimulate demand in the context of President Xi Jinping’s continuing pursuit of Covid suppression.

The problem is clearly that Covid suppression is creating fundamental uncertainty for the most important segment of the Chinese economy, namely the middle-class consumer.

China’s technocrats doubtless understand this only too well but they can only work around the edges given the Chinese President’s continuing promotion of Covid suppression.

And it seems unlikely that President Xi has read Irving Fisher and understands the related concept of debt deflation (see Irving Fisher’s article: “The debt-deflation theory of great depressions”, Econometrica, October 1933).

In this respect, the risk is that the Chinese president severely underestimates the adverse economic consequences of liquidity preference, most particularly as applied to China’s most important sector, the residential property market.

Indeed this has often been described in recent years, without undue exaggeration, as the most important sector in the world.

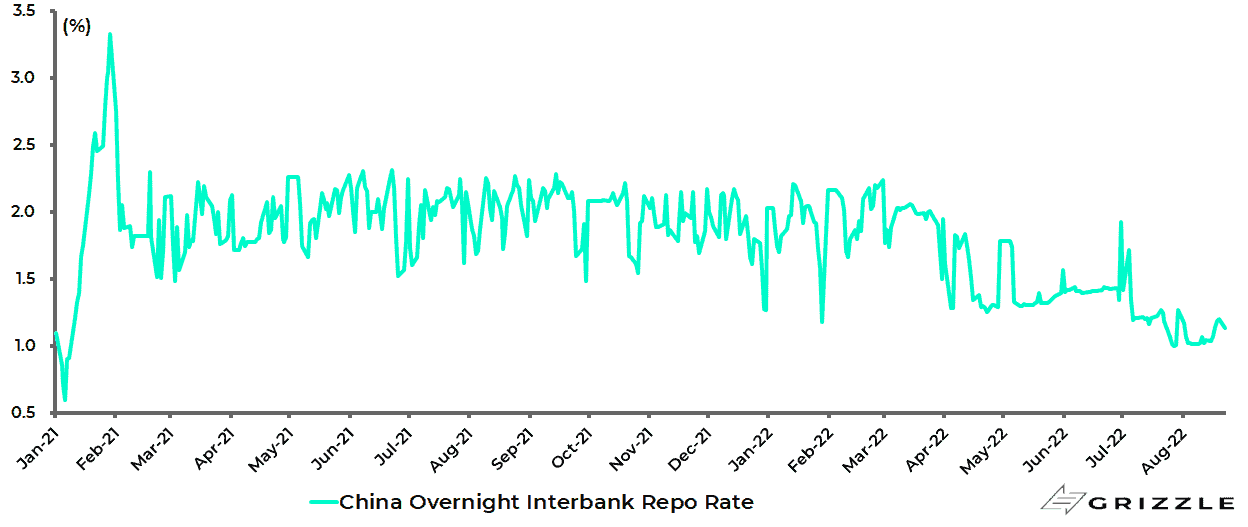

As regards stimulus measures, the recent monetary easing efforts are reflected in a further decline in money market rates over the past two months.

The overnight borrowing rate in the interbank market declined from 1.93% at the end of June to 1.0% on 27 July, the lowest level since January 2021, and is now 1.14%.

China overnight interbank repo rate

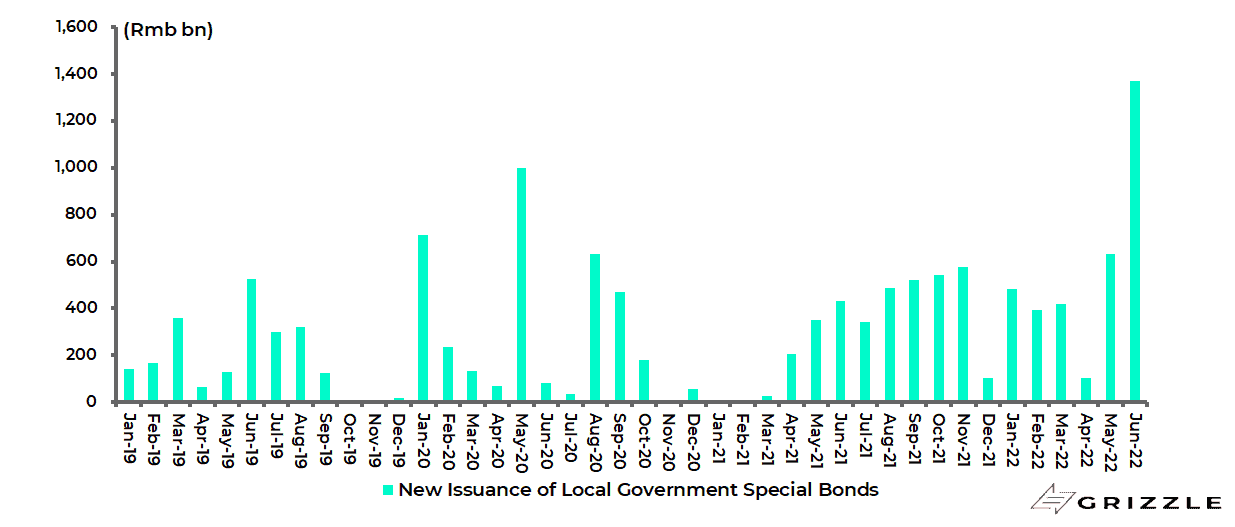

It is also the case that the issuance of infrastructure bonds has increased dramatically in recent months which means infrastructure investment will be stronger this year than originally forecast.

China issued a record Rmb1.4tn of new local government special bonds in June, which are mainly used to fund infrastructure projects, with Rmb3.41tn of the Rmb3.65tn annual quota already issued by the end of 1H22.

The Ministry of Finance is also reportedly considering allowing local governments to issue Rmb1.5tn of special bonds in 2H22.

China net issuance of local government special bonds

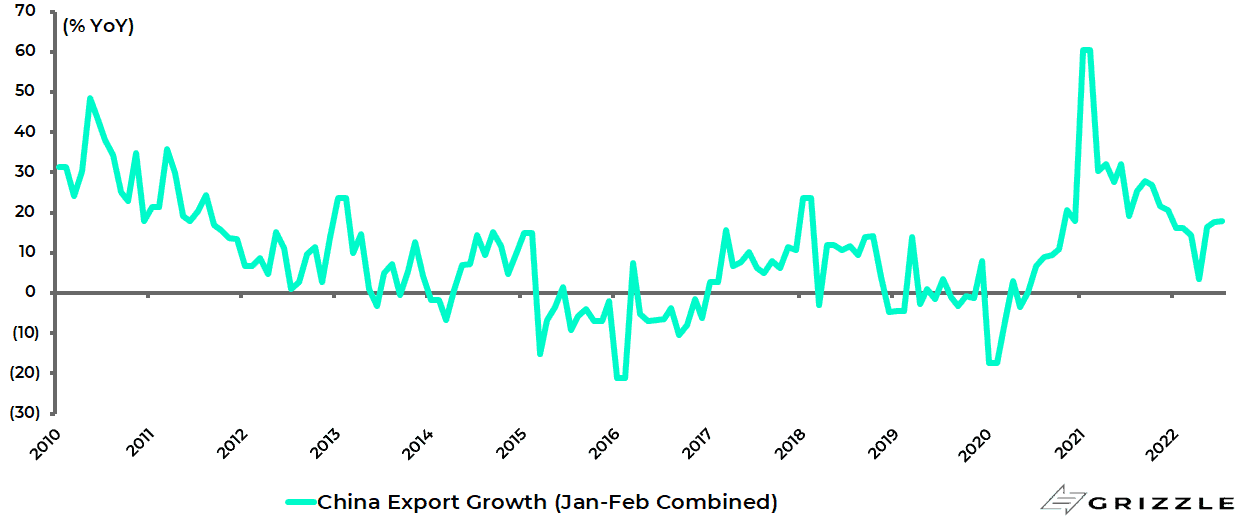

It is further the case that Chinese exports are holding up relatively well.

Exports rose by 18% YoY in July and are now up 14.6% YoY in the first seven months of 2022.

China export growth in US dollar terms

This is probably explained by Chinese factory owners managing to work around Covid restrictions via pragmatic arrangements.

Examples are workers sleeping at the place of work or being told only to come to work if they test negative on a daily basis.

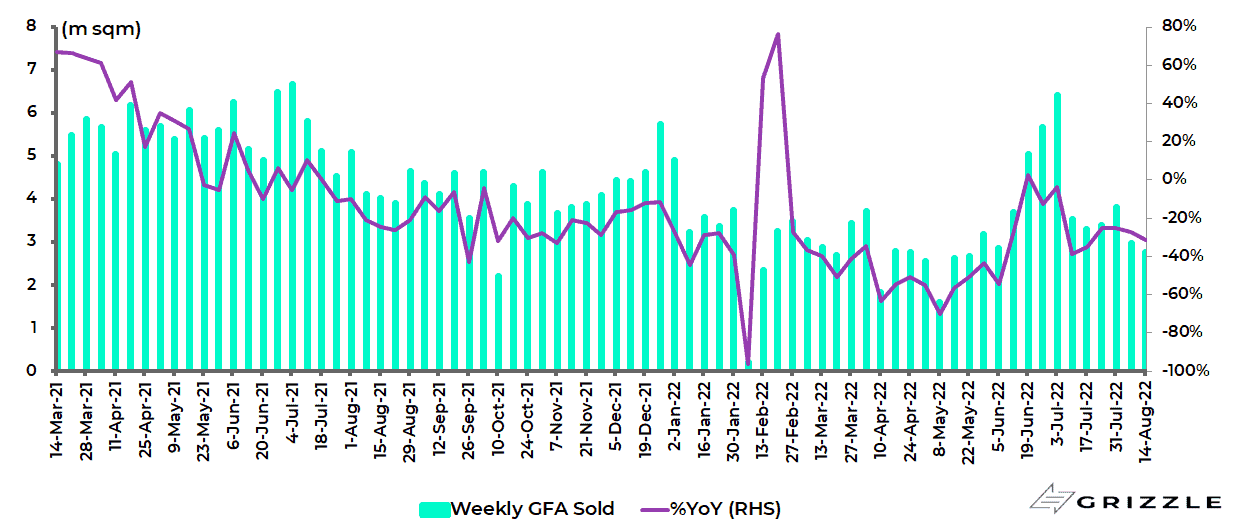

China Property Sector is Flashing Warning Signs

Still by far the most important sector in the Chinese economy is property and there the trend is not encouraging.

In this respect, demand is not responding as usual to the growing number of property easing measures announced in recent months, including cuts in mortgage rates.

Residential floor space sales turned down again in July and August for the 25 major cities, which account for about 15% of total sales, declining by 32% YoY in the four weeks to 31 July and 29% YoY in the first two weeks of August.

China residential floor space sold in 25 key cities

Source: CREIS

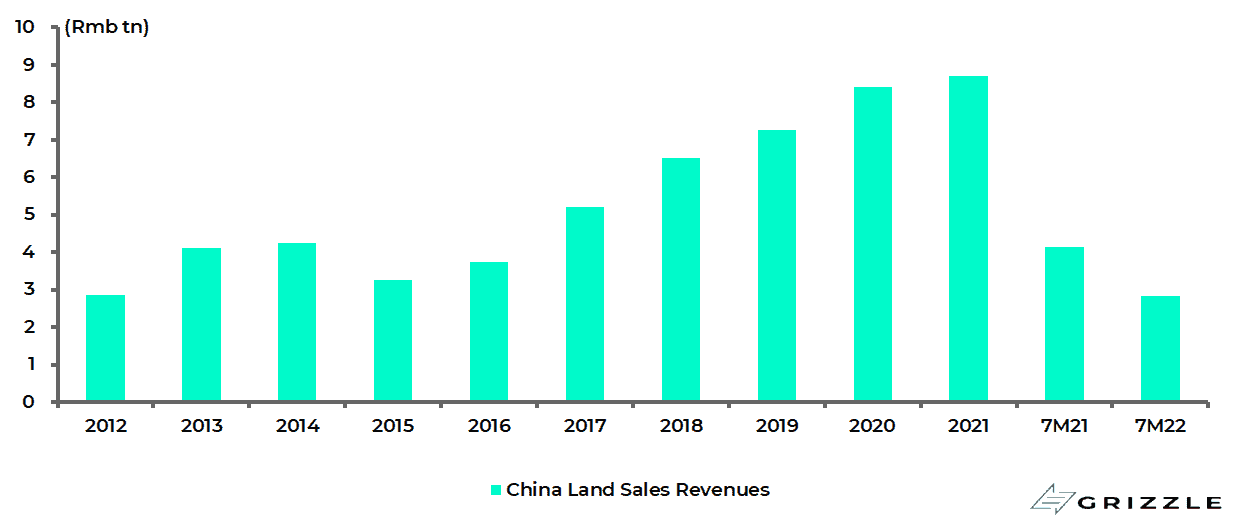

Weak property sales also have negative implications for local governments’ finances given their dependence on property sales.

Land sales revenues, which account for 30-40% of local government revenues, declined by 31.7% YoY to Rmb2.83tn in the first seven months of 2022.

China land sales revenues

Property Buyers are Fighting Back

Meanwhile recent weeks have seen newsflow of a type not really seen since China privatised its residential property sector back in 1994 triggering the mother of all property booms.

That is reports of growing numbers of home buyers, acting in seeming unison via social media, going on mortgage strike because construction work has halted on their unfinished property projects.

Homebuyers say that they will stop mortgage payments until developers and commercial banks take action to resume construction.

More than 300 projects in over 90 cities have now reportedly been affected by such mortgage boycotts.

In this respect private developers, short of cash, have been halting construction of projects even if they have already been sold.

About 90% of property sales in China are of uncompleted units.

Personal mortgage loans totaled Rmb38.9tn at the end of 2Q22, accounting for 19% of total renminbi bank loans outstanding of Rmb206tn.

While these strikes can be dealt with politically by letting the buyers off their mortgage liability, as reported by Bloomberg last month (see Bloomberg article: “China Weighs Mortgage Grace Period to Appease Angry Homebuyers”, 18 July 2022), the core problem is the growing financial difficulties of private sector developers in a property market which is not responding, as it would normally do, to property easing.

For the record, the Bloomberg article reported that China may allow homeowners to temporarily halt mortgage payments on stalled property projects without incurring penalties, based on “people familiar with the matter” citing a yet-to-be-finalised proposal from financial regulators.

Meanwhile, going forward, this is why Chinese property buyers will increasingly only want to buy from SOE developers, whose share prices have significantly outperformed in recent months.

All of the above is the direct consequence, albeit an unintended one, of Covid suppression.

While the three red lines policy introduced by Beijing in August 2020 amounted to a controlled implosion (see China and Hong Kong Real Estate are in Good Shape Despite The Headlines, 2 December 2021), in terms of seeking to bring to heel the most leveraged developers without causing systemic risk, the continuing pursuit of Covid suppression threatens to trigger the property bust China bears have long predicted and, until now, wrongly predicted.

This is why the best easing measure would be an announcement of a meaningful change in Covid suppression.

But that is unlikely in the extreme prior to the 20th Communist Party National Congress which is expected to be held in October or November though there are rumours of the event being moved forward.

The only thing that is certain is that no exact date has yet been announced.

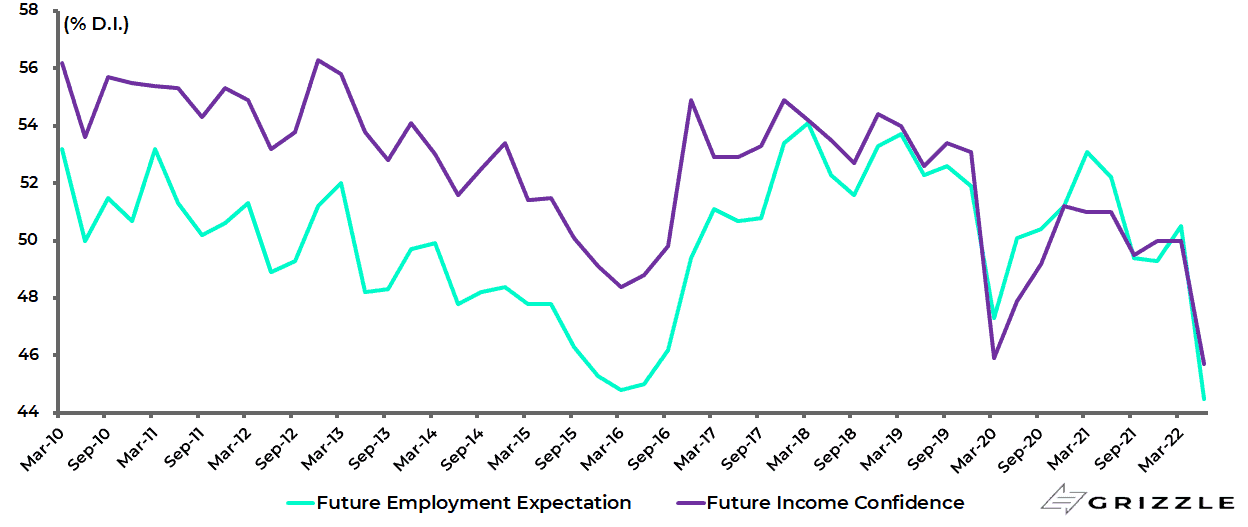

The growing damage done to middle class consumer confidence by Covid suppression, in terms of the lockdowns and the general increased level of uncertainty in the daily conduct of life, are probably best gauged by the results of the PBOC’s quarterly survey of urban depositors which saw expectations for incomes and employment plunge to the lowest levels in more than a decade in 2Q22.

The future income confidence index declined from 50% in 1Q22 to 45.7% in 2Q22, the lowest level since 1Q01, while the future employment expectation index fell from 50.5% in 1Q22 to 44.5% in 2Q22, the lowest level since 1Q09.

PBOC Urban Depositor Survey: Future employment and income expectations

Note: Diffusion Index. Source: PBOC

Consensus growth forecasts are now for 3.7%.

This is an example of the mixed signals which have come out of China’s central government in recent months, which is something this writer has not seen before in more than 25 years of monitoring China close up.

Meanwhile, Li changed his tone last month saying in a speech in July to a virtual event organised by the World Economic Forum that China will not employ large-scale stimulus to try and hit the economic growth target.

All of the above is the result of China under Xi continuing to be run primarily around politics, not economics.

The question is whether this is a permanent state of affairs or whether a return to more pragmatic policies will prevail once the issue of leadership succession is secured.

It has to be admitted that the answer to that question is not clear.

Meanwhile, aside from the question of leadership succession, where this writer is still assuming status quo, the other critical unanswered question will be the exact personnel makeup of the Politburo Standing Committee, the seven-member group that really run the country.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.