Base effects mean the real test of whether the pickup in inflation will prove transitory or not will only become clearer in the second half of this year, which is also why the Federal Reserve did not feel compelled to address tapering issues more directly at the last FOMC meeting in mid-June.

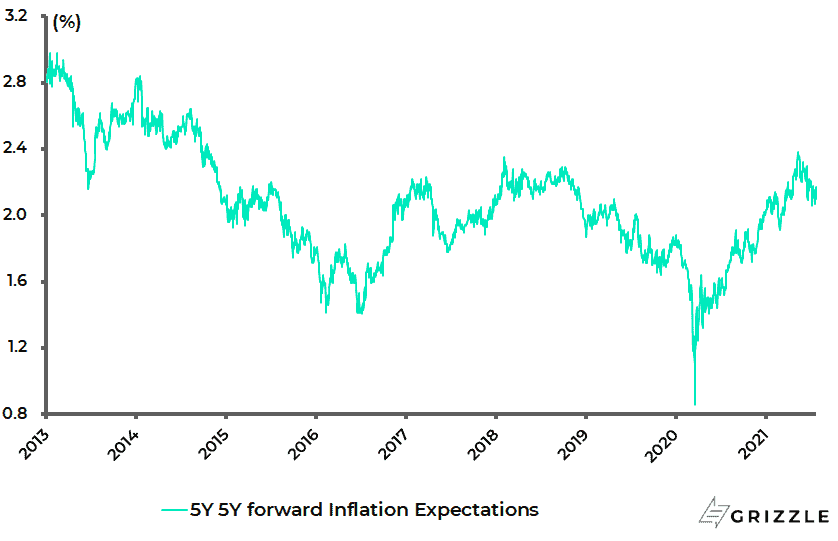

Indeed, the decline in market-driven inflation expectations in recent weeks has undoubtedly further reduced the near-term pressure on the Fed.

US 5-year 5-year forward inflation expectation rate

Still, it is important to note that non-market inflation expectations continue to remain elevated.

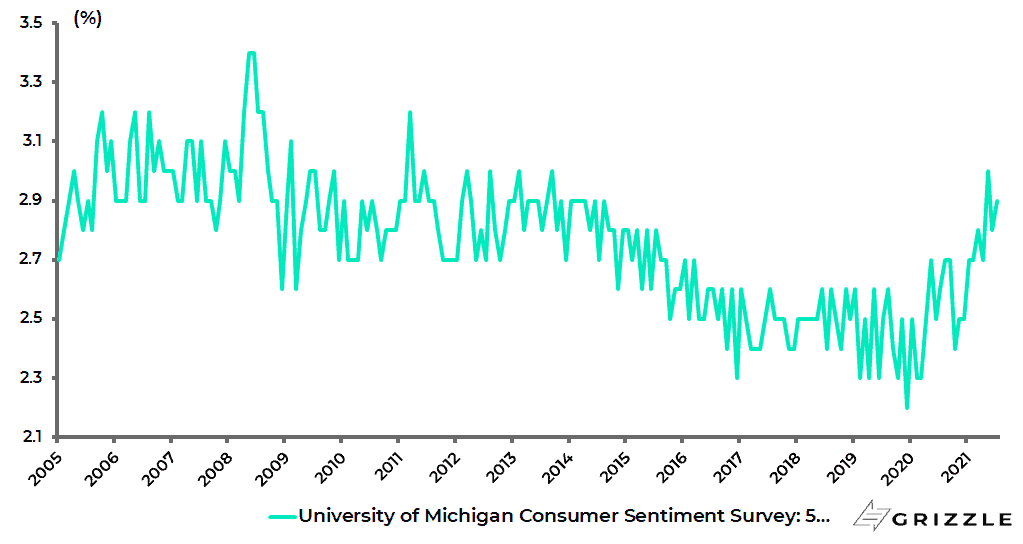

The University of Michigan’s 5-year inflation expectations declined from 3.0% in May to 2.8% in June and a preliminary reading of 2.9% in July.

University of Michigan consumer sentiment survey: 5-year expected inflation

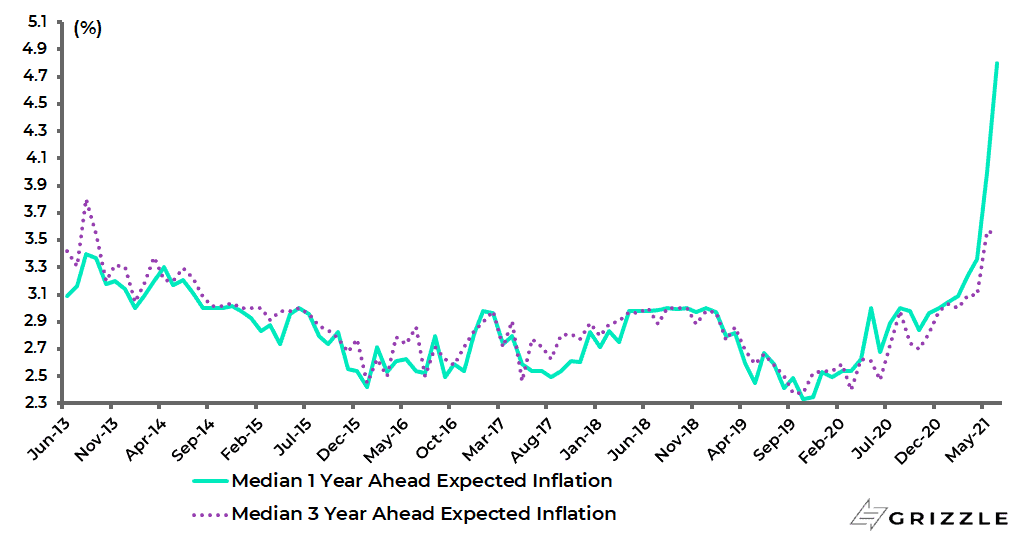

While the New York Fed’s latest survey of consumer expectations released on 12 July shows that one-year ahead inflation expectations rose from 4.0% in May to 4.8% in June, the highest level since the survey began in 2013, inflation expectations at the three-year time horizon remain unchanged at 3.6%, the highest level since August 2013.

New York Fed survey of consumer expectations: Inflation expectations

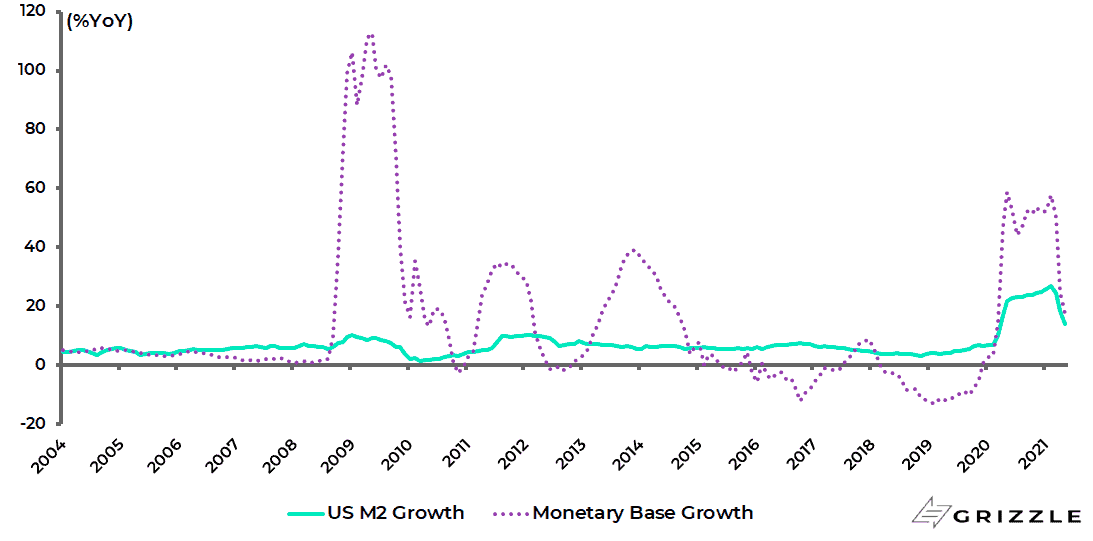

Money Printing Hasn’t Translated to Broad Money Supply Growth, Yet.

The key fundamental issue here remains whether the activist fiscal and monetary policy response to the pandemic has created a different dynamic from what transpired after the global financial crisis.

In this respect, it has long been argued here that quantitative easing since late 2008 has primarily led to asset price inflation as reflected in the contrasting trend between broad and narrow money supply growth.

US broad and Narrow Money Supply Growth

By contrast, what was so interesting about the monetary easing last year was that it triggered broad money supply growth which suggested that money was going to the real economy and not just on asset speculation.

This in turn would suggest a likely pickup in velocity, which is what needs to happen if inflation is to prove less transitory than what the central bankers expect.

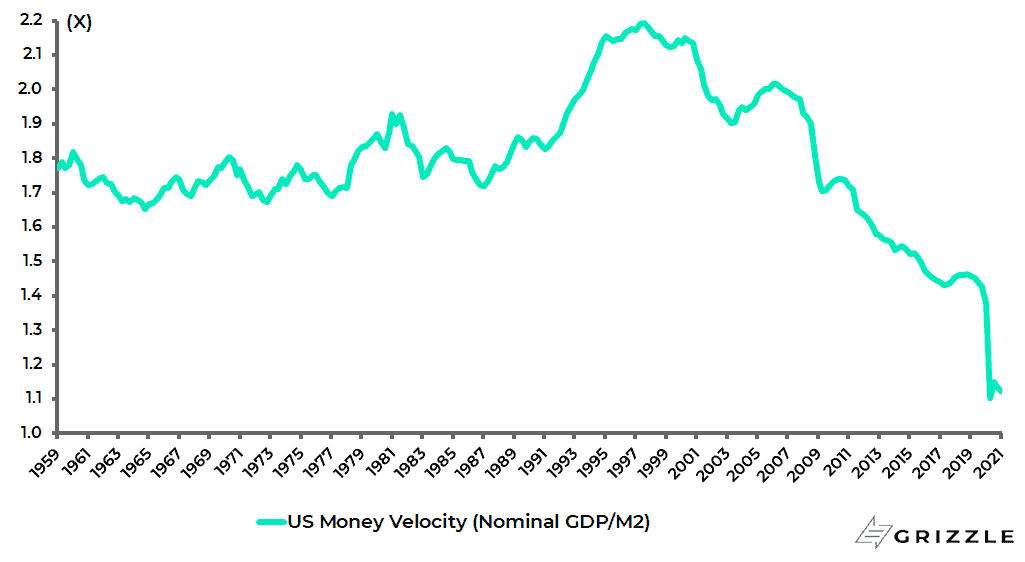

In this respect, it is the case that post-2008 quantitative easing coincided with an ongoing decline in velocity.

US M2 velocity declined from 2.02x in 2Q06 to 1.12x in 1Q21.

US M2 (Money Supply) Velocity

This is why it is critical to keep a close eye on the credit multiplier, or the lack of one.

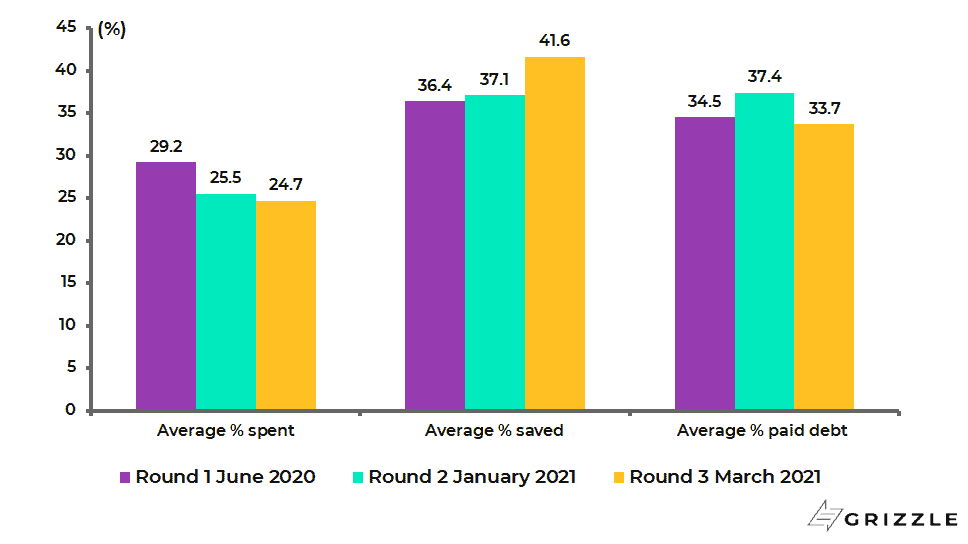

Will Americans Spend their Stimulus Checks?

The continuing decline in the loan-to-deposit ratio of US commercial banks in the first quarter signaled the lack, for now, of such a multiplier in action, but this occurred during a period when the American economy was still in lockdown while household deposits were boosted by transfer payments.

A key issue now is the extent to which the transfer payment windfall is spent or saved, given that eligible Americans have received three rounds of stimulus cheques worth up to US$3,200 since April 2020.

New York Fed survey data published in early April suggests that consumers are expected to spend an average 24.7% of the latest stimulus cheques being sent out since mid-March, down from 25.5% for the second round received in January and 29.2% for the first round last year.

By contrast, they are expected to save 41.6% of the latest stimulus cheque, up from 37.1% in January and 36.4% last year.

While about one-third of the payments are expected to be used to PAY DOWN DEBT.

How American households use their stimulus cheques

It should be noted that these results are based on surveys of over 1,000 respondents who received or expected to receive stimulus cheques.

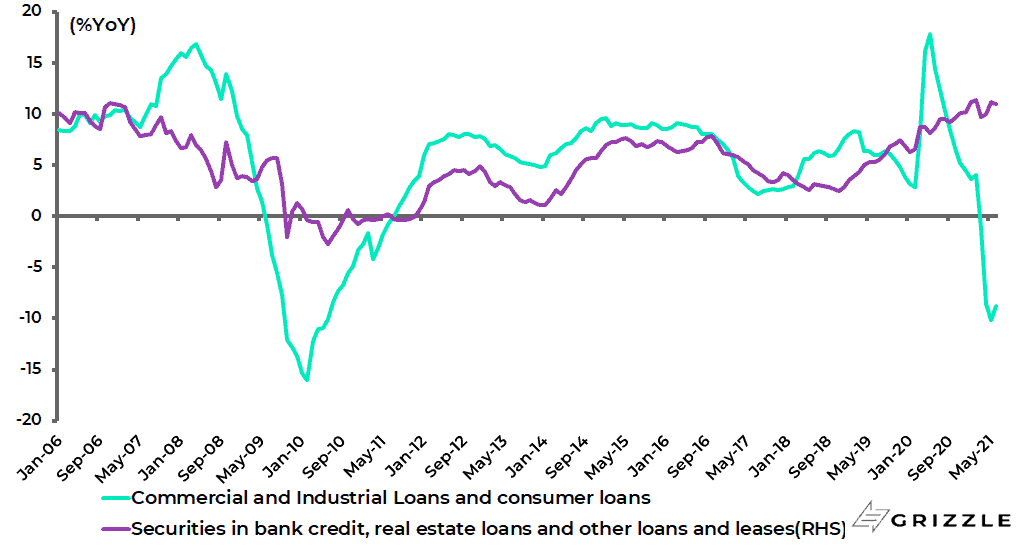

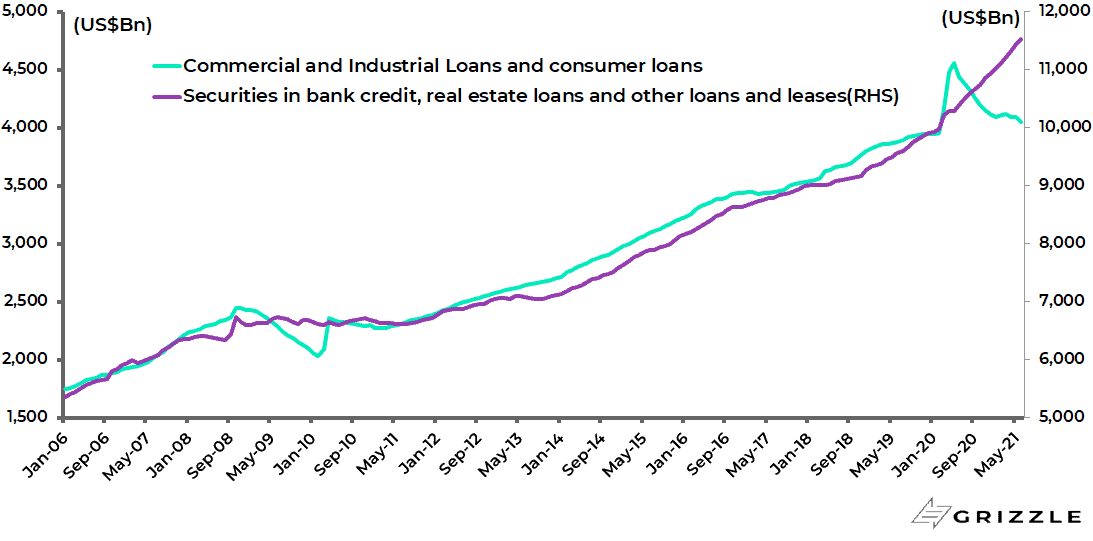

US Bank Lending a key Catalyst to Turn Money Printing into Inflation

It is also important to keep a close eye on the breakdown of the US bank credit data for evidence of more loans going into the real economy via, say, loans financing capex in the case of corporates or via consumer loans in the case of households, as opposed to lending to finance asset purchases.

Thus, aided by various forms of loan guarantees, commercial and industrial (C&I) loans and consumer loans rose by 17.8% YoY in May last year but have since slowed to 4.8% YoY at the end of 2020 and were down 10.2% YoY in May 2021 and 8.8% YoY in June primarily due to the base effect.

US bank credit growth (breakdown for loans to the real economy and credit for asset purchases)

Still the outstanding level of C&I loans and consumer loans remains 2.5% above the pre-Covid level in February 2020.

The state of play on such “real economy” lending should become clearer when the base effect moves out of the data in 4Q21.

By contrast, US banks’ securities holdings, real estate loans and other loans and leases, which could be construed as lending to finance asset purchases, have continued to rise, up by 11% YoY in June, compared with 6.6% YoY in February 2020.

US Bank Credit Outstanding

This suggests that the asset speculation game is far from over.

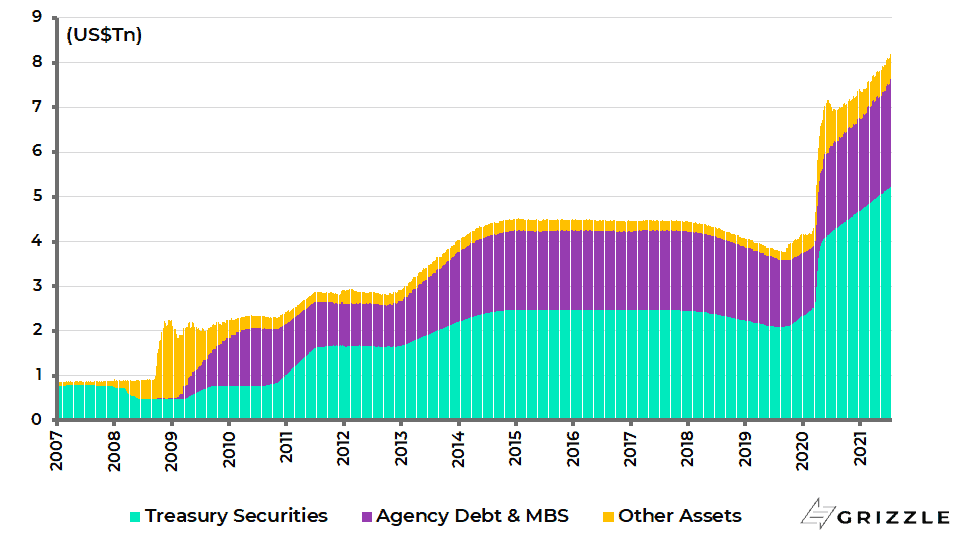

In this respect, it needs to be remembered that quanto easing continues in the sense that the Fed is still expanding its balance sheet at a rate of US$1.3tn or 18% a year and, as already discussed, quanto easing drives asset inflation.

Federal Reserve balance sheet

Still it should again be stressed that a new form of political and fiscal activism is now in evidence, a trend which has been accelerated by the pandemic.

This was on show in the G7 meeting in June with the relevant governments signing up to what could be described as a new social democrat consensus to spend taxpayers’ money to address fashionable concerns.

Indeed the message sent was essentially that no amount of spending is too much if it is to address the two perceived ills facing modern mankind; namely global warming (‘the race to zero’) and inequality (‘levelling up’).

If this is the overriding political context in the Western world it is, in this writer’s view, a resulting political reality that the central banks will be expected to finance such spending if tax revenues are not forthcoming.

This is what they did on a ‘needs must’ basis last year in response to the soaring fiscal deficits triggered by the policy response to the pandemic.

This is how, for example, to view the related surge in the Fed balance sheet and the US fiscal deficit last year and indeed so far this year.

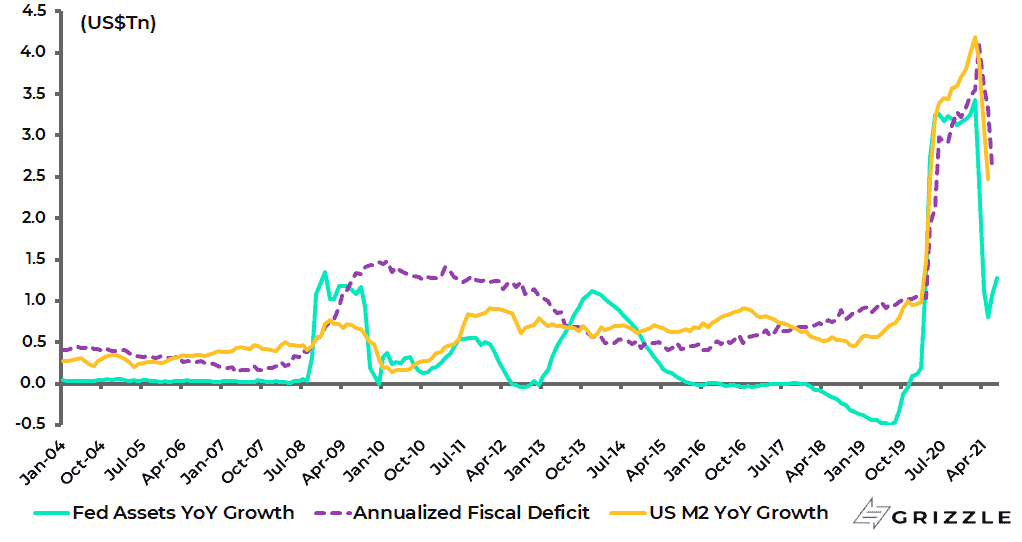

The Fed balance sheet increased by US$3.2tn last year and is up US$877bn so far this year, while the US fiscal deficit totaled US$3.35tn in 2020 and US$1.665tn in the first six months of 2021.

US Annualised Fiscal Deficit and YoY increase in Fed Assets and M2

Advocates of modern monetary theory (MMT) would like to make this central bank financing of government explicit rather than implicit, as is the case now.

Whereas the central banks would like to maintain the official narrative that they are still pursuing their traditional mandates as regards inflation and employment; though even here the game has changed significantly in the Fed’s case with the licence to overshoot the 2% inflation target and the commitment to “full and inclusive” employment.

Still if markets remain, understandably in the short term, focused on central bankers’ every word and action, the game is changing.

This is because the central bankers are in the process of becoming less important in the sense that, so far as this writer is concerned, when the pressure is on they will be forced to accommodate financially the need for more government spending.

Indeed this can be seen in the mission creep politically motivated central bankers have begun to embrace in their desire to re-invent themselves and thereby remain relevant.

Already having faced legitimate criticism from both the political right and left for driving inequality via their quanto easing policies, which as already noted have indeed propelled asset price inflation, they naturally want to change the narrative by linking monetary policy to the fashionable green/climate agenda in some form or other.

The early indication is that this is likely to take the form of central banks buying so called green bonds, offering the potential carrot of near free debt financing for borrowers who meet entirely arbitrarily conceived green criteria.

This mission creep has been criticised correctly by the likes of former US Treasury Secretary Larry Summers and former Bank of England governor Mervyn King as extending beyond central bankers’ traditional monetary policy remit, and therefore beyond their level of competence.

In fact, such critics argue that the central bankers have already put at risk their anti-inflation credentials.

But this is clearly the direction of travel politically.

Still all of the above will not come to a head until the bond market, and inflation expectations, are again signaling rising inflation concerns.

For it is such a renewed sell-off in the bond market that will test the Fed’s metal, in terms of whether it really is willing to turn orthodox, or whether it does the opposite by imposing some form of yield curve control to blunt the message sent by rising bond yields.

And clearly the latter outcome would send the signal that central banks are really determined to inflate their way out given the ever greater levels of outstanding debt.

Such a signal would in turn increase the risk of a pickup in velocity.

This is, of course, why central bankers almost never talk about it.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.