Pushing on a string as regards the mainland Chinese economy was the theme discussed here recently (see Pushing on a string: China’s consumer demand problem, 26 August 2022).

And there has been more such pushing of late with more interest rate cuts announced in recent weeks.

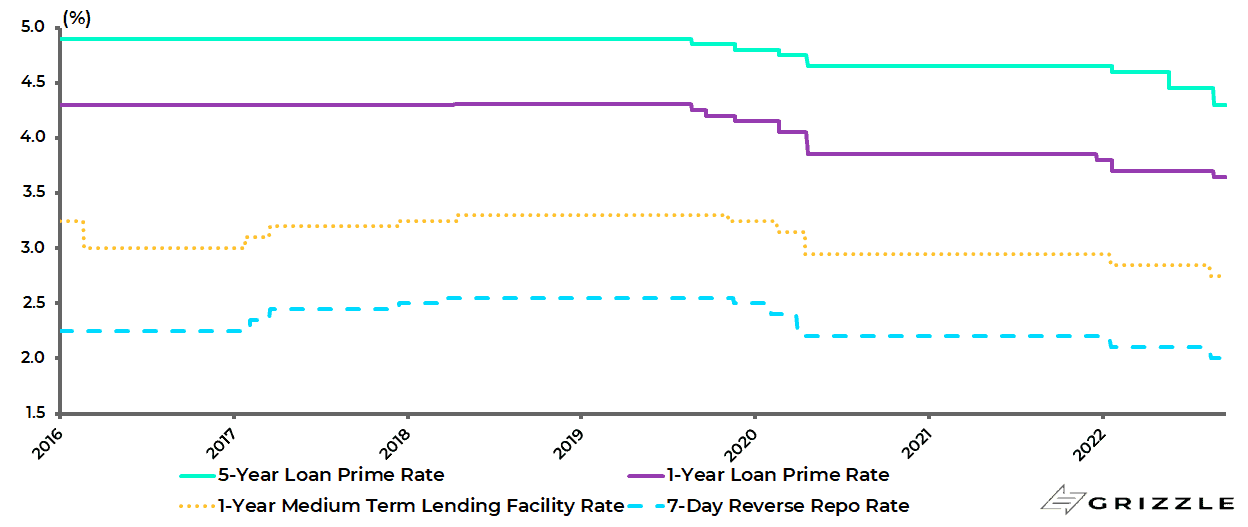

The PBOC, for example, cut the one-year loan prime rate, which is used to price corporate loans, and the five-year loan prime rate, the benchmark rate for pricing mortgages, by 5bp and 15bp, respectively, to 3.65% and 4.3% late last month.

China interest rates

The policy response is clearly driven by the growing slump in the residential property market which is primarily the unintended consequence of Covid suppression.

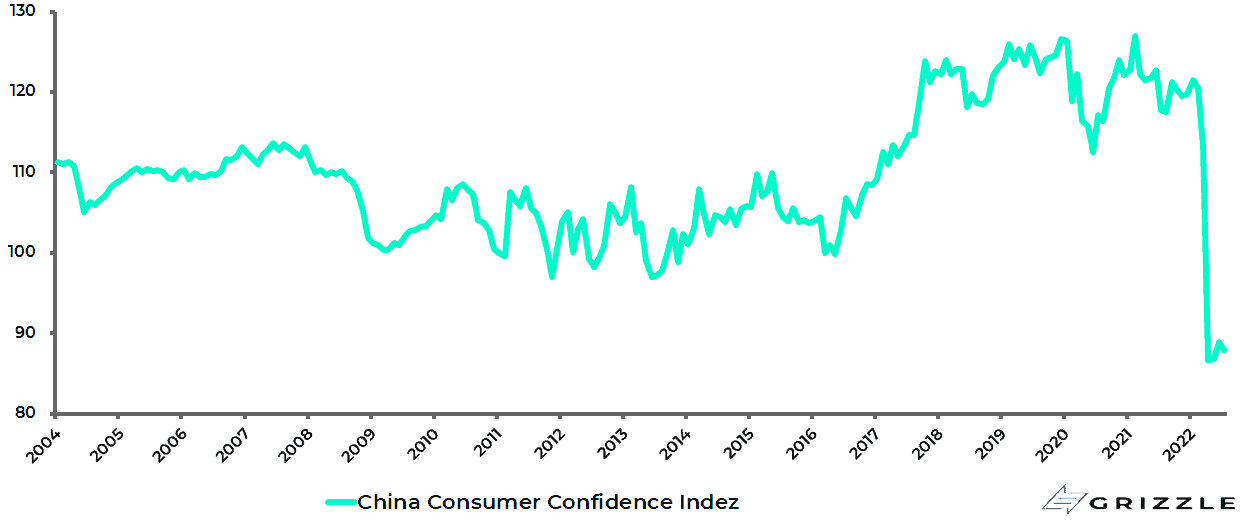

Chinese middle class consumer confidence has been badly damaged by the lockdowns, and the fear of more lockdowns to come, in terms of people’s ability to lead a normal life and earn income.

The consumer confidence index collapsed from 113.2 in March to a record low of 86.7 in April and was still only 87.9 in July.

China consumer confidence index

While there is now a generalised reluctance to buy property on a pre-sale basis from private sector developers because of legitimate concerns that they will not complete the project, as reflected in the previously discussed mortgage boycott issue (see Pushing on a string: China’s consumer demand problem, 26 August 2022).

Home buyers in more than 300 projects have reportedly been boycotting their mortgage payments to banks because of delays in construction of their homes.

The problem is that the only way really to address this issue properly is a U-turn on Covid suppression, and there remains no evidence of this from President Xi Jinping as yet.

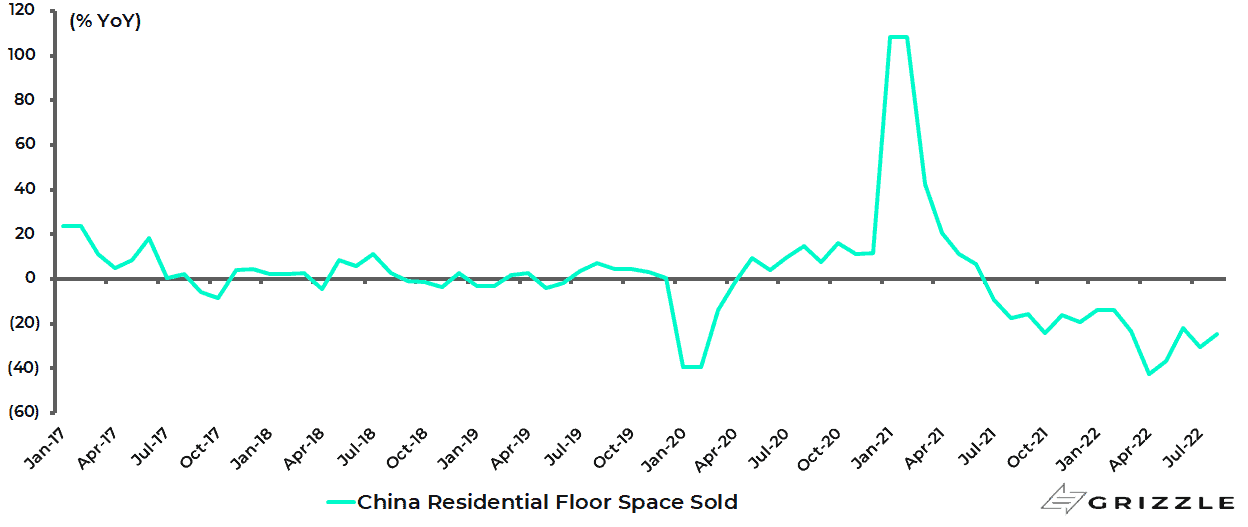

Meanwhile the latest property data has shown no sign of a pickup.

Sales of residential property floor space nationwide declined by 24.5% YoY in August, while the data in the first two weeks of September for the top 25 cities, which account for about 15% of the total market, shows a further 34% YoY decline.

China residential floor space sold %YoY

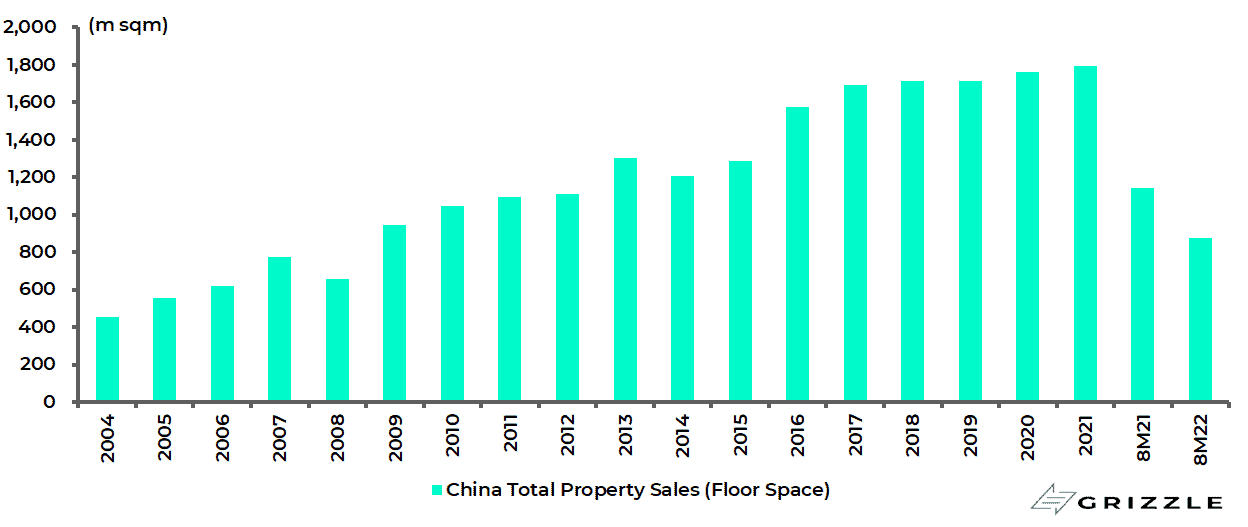

The downside risk now is for total property sales this year to be as low as the 2015 figure of 1.28bn sqm compared with average annual property sales of 1.71bn sqm in the last six years.

Total property sales declined by 23% YoY to 879m sqm in the first eight months of this year.

Assuming the same pace of decline for the rest of the year, property sales will fall to 1.38m sqm in 2022, the lowest level since 2015.

China total property sales

Housing Activity is Slowing Rapidly

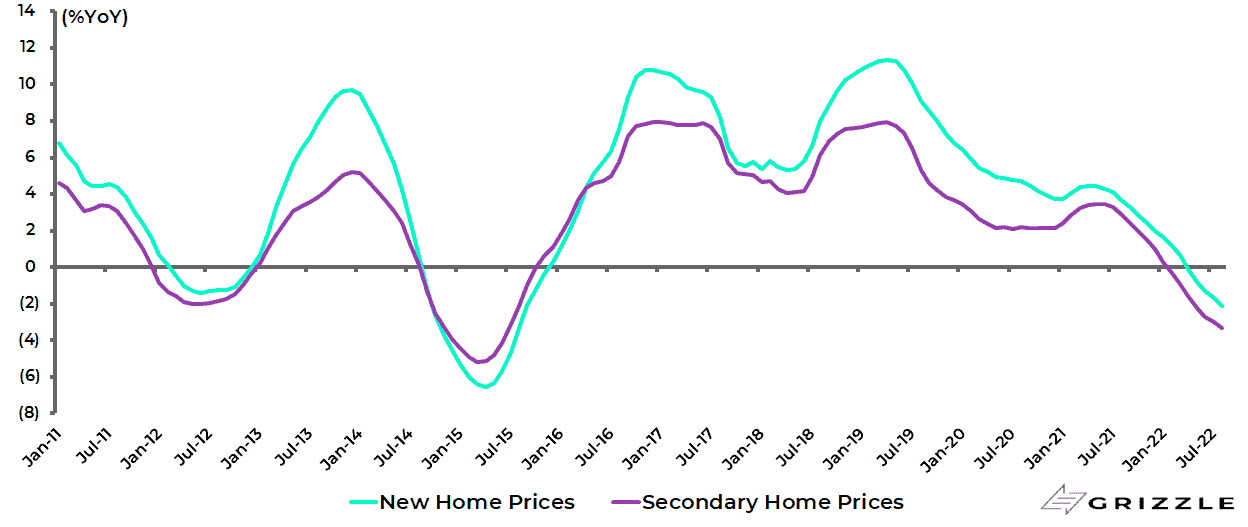

Meanwhile, home prices are now declining on a year-on-year basis.

New home prices in the 70 cities surveyed by the National Bureau of Statistics declined by an average of 2.1% YoY in August while secondary home prices were down 3.3% YoY.

China new and secondary home prices in 70 major cities %YoY

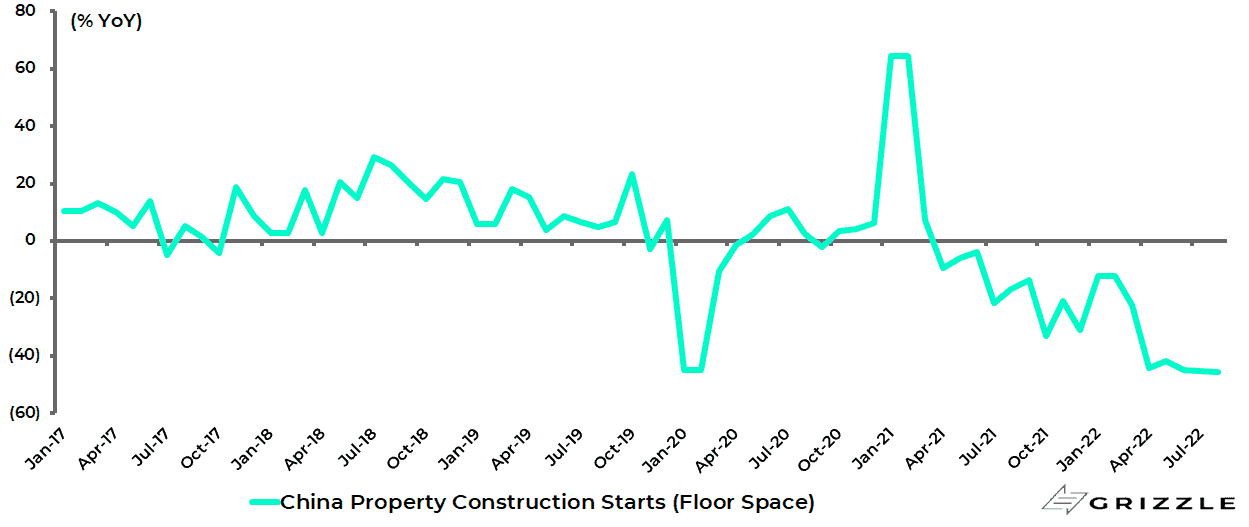

The growing financial problems for private property developers, in terms of declining sales and rising indebtedness, is leading to an even more dramatic decline in construction.

Property construction starts declined by 37% YoY in the first eight months of this year and were down 46% YoY in August.

China property construction starts (floor space)

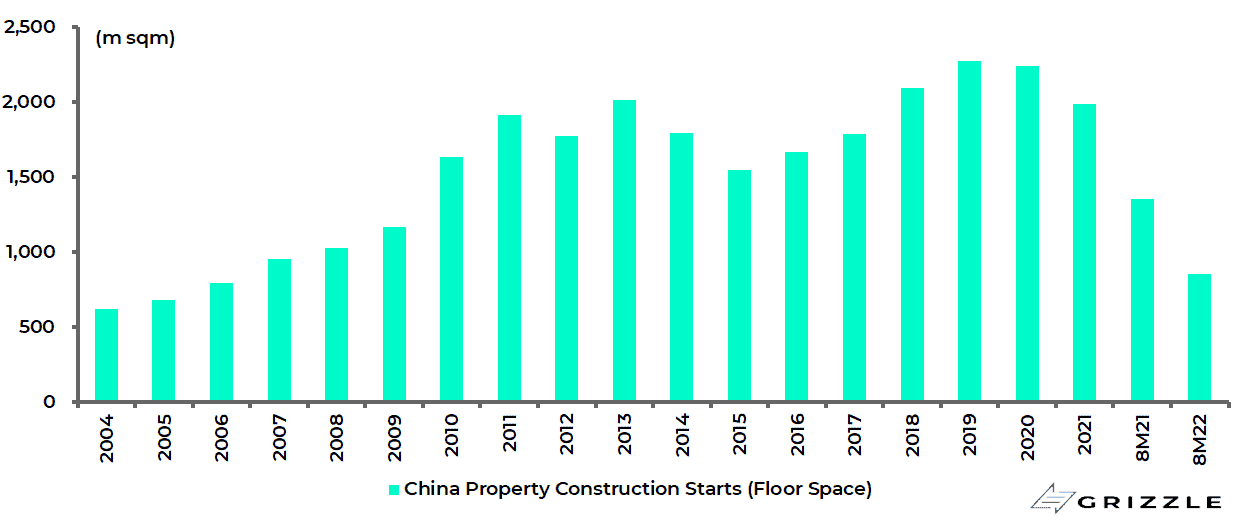

The weakness in construction preceded the renewed downturn from Covid suppression because of the Three Red Lines policy targeting leveraged developers launched in August 2020.

Property construction starts started declining on a year-on-year basis in April 2021, while property sales began to decline YoY in July 2021.

Still Covid suppression has now made the collapse in construction much worse.

This is why, if the initial downturn was deliberately induced by the authorities, the collapse in activity this year certainly was not.

Hence the increasingly frantic efforts to ease, be it rate cuts or local governments dispensing with home buying restrictions.

The average effective first-home mortgage rate has already declined by 129bp in the first seven months of this year to 4.35% in July, prior to last month’s 15bp cut in the five-year loan prime rate, and is down 139bp from the recent high reached last September, according to a survey of 103 major cities by Beike Research Institute.

While the minimum mortgage rate for first-home purchases has declined by 55bp so far this year to 4.1%. More than 20 cities have also reduced down payment requirements for second-home buyers so far this year with an increasing number of larger cities joining in.

For example, Nanjing, Suzhou, Wuxi and Fuzhou announced last month down payment cuts of 10-20ppts for second-home buyers.

This, to this writer, is a more effective easing than rate cuts.

A further decline in construction starts of the same severity seen in the first eight months of this year would lead to construction starts declining to 1.25bn sqm in 2022, down from 2bn sqm last year.

This would be the lowest figure since 2009.

China annual property construction starts

A Collapse in Land Sales is Bad for Local Government Budgets

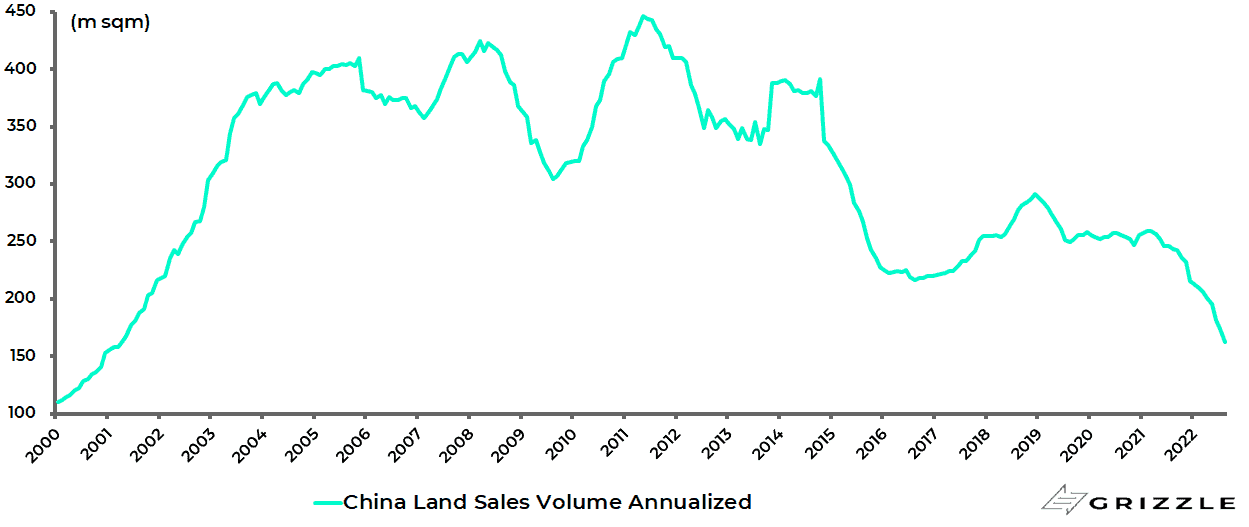

This collapse in construction activity is naturally feeding through to a decline in the volumes of land purchases by developers.

This already fell by 49.7% YoY to 54m sqm in the first eight months of 2022.

China land sales volume annualised

Assuming the same level of decline for the rest of the year, land purchases will decline to 109m sqm, which would be the lowest level since 2000.

Such a decline clearly has broader macro consequences because of the traditional dependence of local governments on land sales for 30-40% of their revenues.

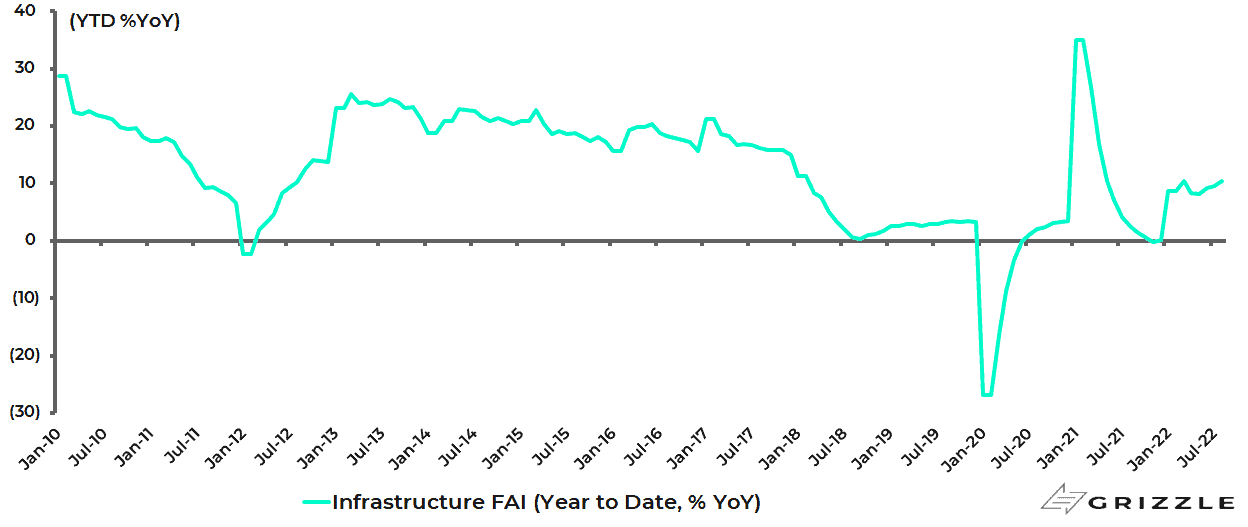

If the residential property market remains a growing concern, increased infrastructure investment is to some extent a support for the economy with fixed asset investment in infrastructure growing by 10.4% YoY in the first eight months of 2022.

China infrastructure fixed asset investment growth

Infrastructure accounts for up to 20% of steel consumption.

Still, if increasing infrastructure stimulus is a positive this year it certainly cannot offset the negative multiplier consequences of the downturn in the Chinese residential property sector which has legitimate claim to be viewed as the single most important sector in the world economy.

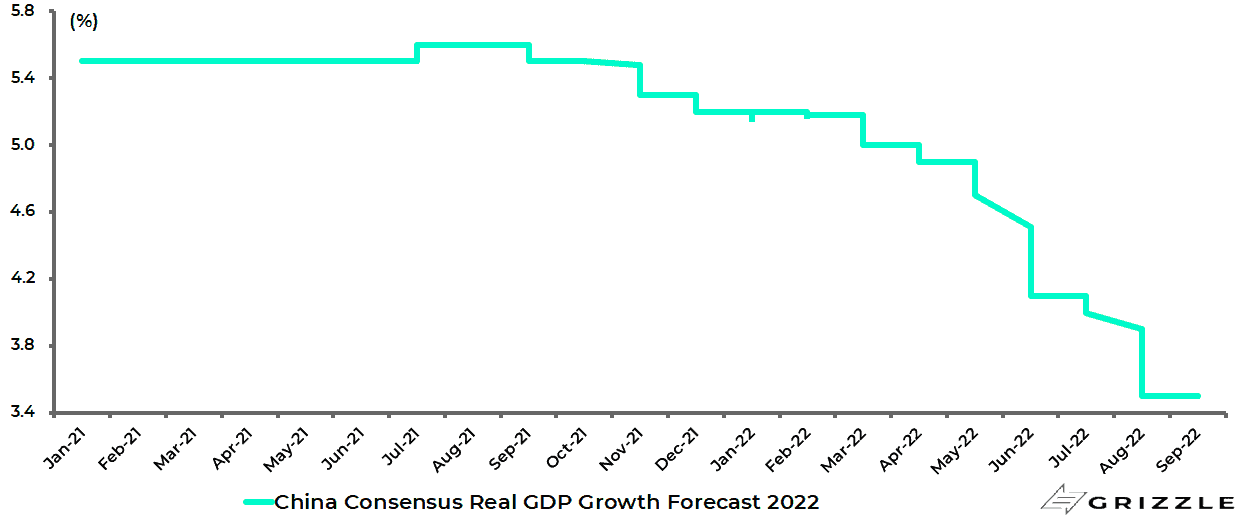

Unsurprisingly, the accumulating evidence of a worsening downturn in residential property has also caused further cuts in consensus growth forecasts for Chinese real GDP growth in 2022.

They have now been cut from 5.6% in September 2021 to 3.5%.

China consensus 2022 real GDP growth forecast

Remember it was only in March that Premier Li Keqiang announced a growth target for this year of 5.5%.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.