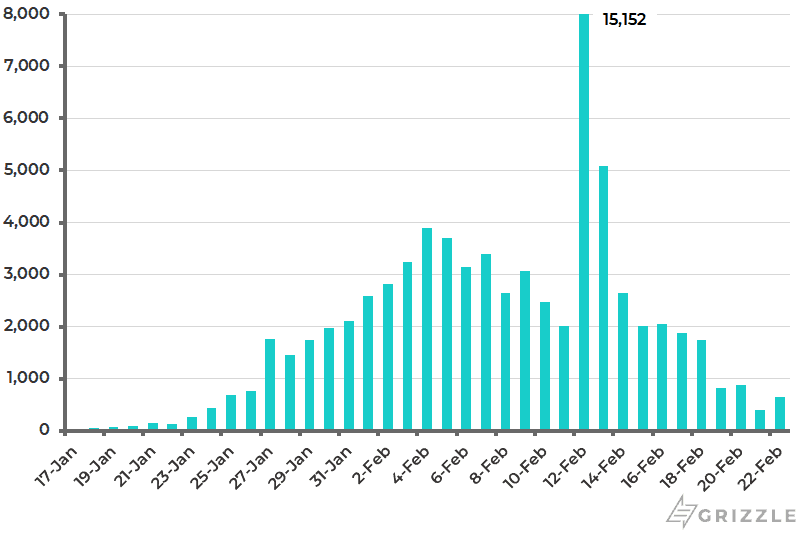

The coronavirus continues to dominate the headlines for understandable reasons. It is increasingly clear that new cases in China have peaked. The number of new confirmed cases in mainland China has declined to 397 on Feb. 21, the lowest level since Jan. 23, and was 648 on Feb. 22, according to the National Health Commission (see following chart).

Number of New Confirmed Coronavirus Cases in Mainland China

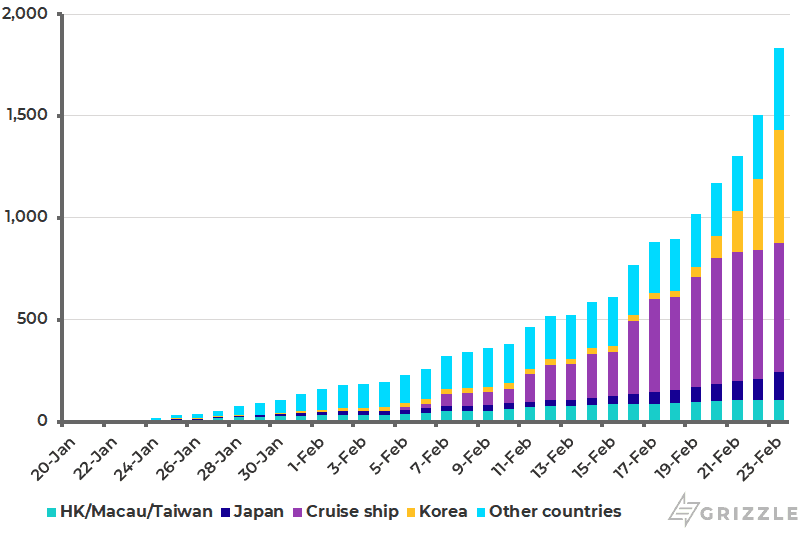

The issue now is the extent to which infections spread outside China. Thus, there are now 1,835 cases outside mainland China, including 106 cases in Hong Kong, Macau, and Taiwan, 556 cases in Korea and 634 cases on a cruise ship off the Japanese coast (see following chart).

Coronavirus Cumulative Confirmed Cases Outside Mainland China

EU Damaging Its Economy Through Decarbonization Efforts

Meanwhile, virus aside, I remain amazed by the potential macroeconomic implications of the Eurozone’s stated agenda to decarbonize its economy. The suicidal implications for the German auto sector was discussed in this column last week (German Auto Sector Threatened by Strict Emissions Regulations, Feb. 19, 2020).

But, similarly, there are plans afoot, in the form of various regulations and directives, to decarbonize other energy intensive sectors, including chemicals, steel and cement. All this is going to cost a lot of money, in terms of investment in so called “sustainable” energy. The European Union’s current estimate is €260 billion of additional annual investment to meet the current 2030 climate and energy targets, equivalent to 1.5% of 2018 GDP, according to the European Commission.

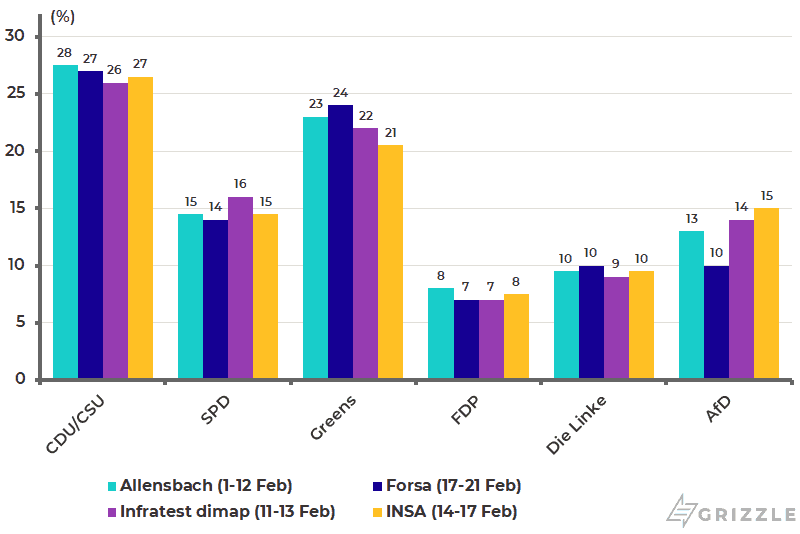

The above raises the issue of who is going to pay for it? German taxpayers or the European Central Bank (ECB) via direct monetization in a green version of Modern Monetary Theory? That will be the subject of much political debate though clearly momentum will pick up for such policies if the Greens enter the German federal government. This is a growing possibility given that the party currently commands 22-24% support in the opinion polls (see following chart). Indeed the Eurozone already has the precedent of a right-wing and green coalition government in Austria.

Latest German Opinion Polls

A Possible Silver Lining from Decarbonization

The one potential positive of this possible return to a Soviet-style planned economy in Europe 30 years after the fall of the Berlin Wall, at least initially, is that all this spending could trigger a positive demand shock, in a Keynesian sense, before the likely downside of this politically driven malinvestment becomes apparent. And it is quite possible that some form of a green bubble will have occurred in the interim.

The question then for the European economy is whether this positive dynamic will counter the negative supply shock already facing the German auto sector, the largest sector in the Eurozone’s largest economy. It is certainly a possibility if the political consensus can be achieved in the Eurozone to spend all this money. Still, I would rather focus in the short term on the negative given the auto sector has to start meeting the electric car production targets now which means, for example, that many employees in German auto component companies are at severe risk of losing their jobs.

This also raises an issue which was completely ignored by the green poseurs at the annual gathering of the Davos mob last month. That is that the decarbonization agenda will hit lower income people hardest. A lead indicator of what is to come was the gilets jaunes protests in France since November 2018 which were triggered initially by diesel taxes on light agricultural vehicles. But, amid all the climate angst triggered by what could be termed the “Greta effect”, there remains minimal discussion in the developed world at least of the damage these policies will inflict on ordinary people.

In this respect, the advocates of green policies have not paid enough attention to thinking how to compensate ordinary people hurt by such policies, who otherwise will only be more likely in future to vote for the populist right represented by Donald Trump. A good example is the threat posed by “climate” activism to the continued existence of cheap air travel.

The EU’s Green Agenda vs the UK and U.S.

America is not going to follow Europe’s green agenda under Donald Trump, if he is re-elected, and nor is a pragmatic China. The differences between the current American and European approach were highlighted in an exchange between U.S. Treasury Secretary Steven Mnuchin and ECB President Christine Lagarde at Davos (see Financial Times article: “Lagarde and Mnuchin clash over growth” by Chris Giles, Jan. 25, 2020).

Mnuchin argued, correctly in my view, that access to cheap energy was more important for growth than investment in green technologies. Mnuchin stated: “The world is dependent on having reasonably priced energy over the next 10 or 20 years or we’re not going to create jobs and we’re not going to create growth.” This point is particularly true in developing countries.

The above discussion about the likely negative impact on growth of the Eurozone’s decarbonization agenda is also the reason why Britain is better off out of the Eurozone than in as a consequence of Brexit which finally occurred on Jan. 31.

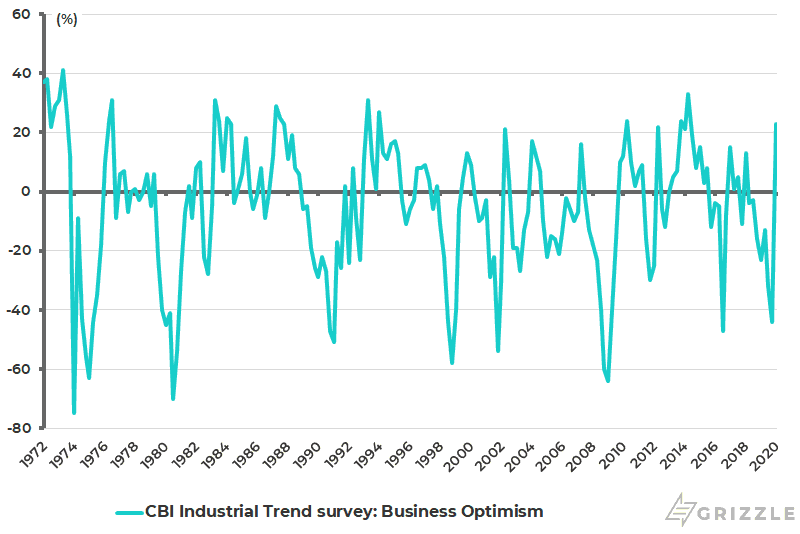

In this respect, it is worth highlighting that the latest quarterly Confederation of British Industry (CBI) Industrial Trend survey showed the biggest rise in business optimism on record. Thus, the survey of 300 UK manufacturing companies reported that business optimism rose by 67% from a negative 44% in the three months to October to a positive 23% in the three months to January, the highest level since April 2014 and the biggest increase since the quarterly data series began in 1972 (see following chart).

UK CBI Industrial Trend Survey: Business Optimism

Still financial markets continue to be concerned about a so-called “hard Brexit”. These concerns stem from the fact that, though Britain has now left the EU, the UK’s future trading relationship with the EU has yet to be agreed; though the deadline for such an agreement is Dec. 31, 2020. In this respect, it has always been my view that the alleged economic costs of Brexit have been grossly exaggerated. Indeed the gusto with which the Eurozone is re-embracing economic planning in the cause of greenery means that Brexit should prove positively liberating from an economic standpoint.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.