Strong US Economy a Negative for US Stocks

Stock markets have calmed down of late. But bulls on Wall Street should be concerned if the American economy turns out to be as strong as many of them seem to think. This is because there is no way equity valuations in the US can handle the sort of monetary tightening that will result.

This writer remains highly skeptical that growth and inflation are really going to accelerate in the manner hoped for, though Donald Trump’s infrastructure ambitions have the potential to deliver another positive catalyst in 2019 following the jolt provided this year by tax cuts. But it still looks likely that financial markets are heading for a big inflation scare, with the correction earlier this month over one strong wage number a prelude of what is to come.

GE: The Posterchild of Corporate Financial Engineering

Meanwhile it is worth going into a little more detail about the consequences of so many years of financial engineering in America. The result is a scary lack of tangible book values on American corporate balance sheets as Wall Street has focused only on profits, taking reported earnings per share at face value.

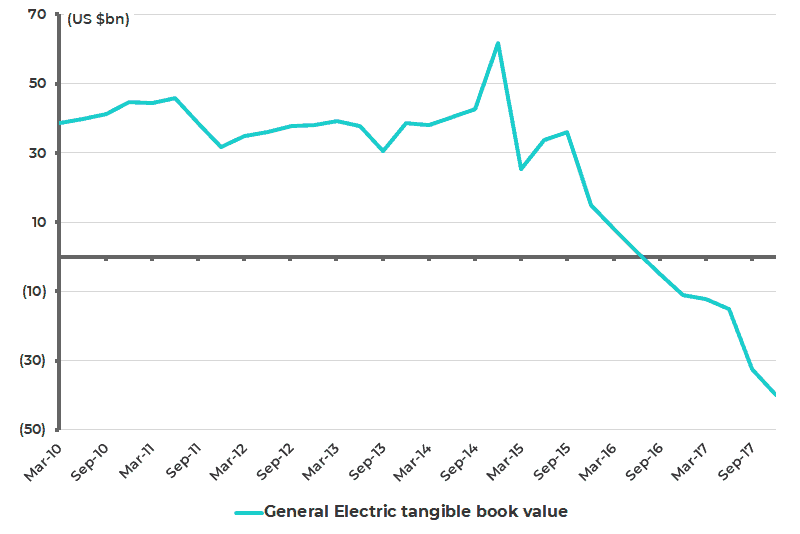

An admittedly extreme example of this phenomenon is General Electric (GE). At the beginning of 2012 General Electric was sitting on tangible book value of US$32 billion. That figure had turned into a negative US$40 billion by the end of 2017 (see following chart).

How did this happen? Part of the explanation is that since 2012 GE has generated US$48.7 billion in net profits, as at the end of 3Q17, but had bought back US$36.6 billion of stock and paid out US$50.5 billion in dividends over the same period.

General Electric Tangible Book Value

General Electric Share Price

If GE is an extreme example, and its share price has suffered as a consequence (down by 53% since July 2016), the lack of tangible book value on a S&P 500 basis is also quite shocking. The S&P 500 ex-Financials Index now trades on 26x tangible book value, compared with only 1.8x for Japan’s benchmark Topix ex-Financials Index, according to Bloomberg (see following chart).

S&P 500 Ex-Financials and Topix Ex-Financials Price to Tangible Book Ratios

Yet the underlying financial vulnerability of corporate America, suggested by this statistic, is only likely to be exposed by significantly higher interest rates.

For now the US stock market, which is still up 1.1% year-to-date despite the correction earlier this month, is benefiting from a forecast 19% increase in earnings in 2018 primarily as a result of tax reform. This has had the effect of making US equities look less expensive based on consensus analyst forecasts. The S&P 500 now trades at 17x consensus 12-month forward earnings.

Corporate Execs Set to Continue Trend of Buying Back Shares vs. Investing in their Businesses

Now it is the case that US tax reform, of which the biggest feature is big cuts in corporate tax, is meant to encourage American companies to invest more in the real economy and less on financial engineering, of which the best example in recent years has been corporates borrowing to buy back their shares. This has had the practical effect of boosting return on equity, a relevant point for many corporate executives whose remuneration is often based on RoE.

This is why it is interesting that the latest evidence suggests that share buybacks have picked up again following the passage of tax reform, after slowing a little in the past two years.

American companies have announced a record US$171 billion worth of share buyback plans this year through February 15, according to estimates by research firm Birinyi Associates. This is up from US$76 billion in the same period last year and the previous record of US$147 billion in the same period in 2016.

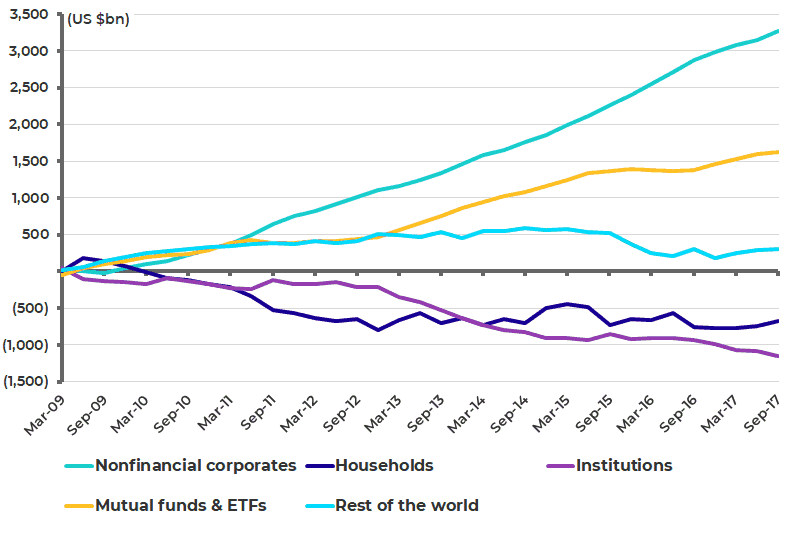

Post the Financial Crisis — Corporations Have Been the Largest Buyer of US Stocks

Remember corporates, via share buybacks, have been the main buyers of shares in the U.S. since 2009. Non-financial corporates have repurchased a net US$3.3 trillion worth of US equities since 2009, according to the Federal Reserve’s flow of funds data (see following chart). By contrast, households and institutions (insurers and pension funds) have sold a net US$672 billion and US$1.2 trillion respectively over the same period, while mutual funds and ETFs have bought a net US$1.6 trillion.

Cumulative Net Purchases of US Corporate Equities

Note: Non-financial corporates’ net repurchases of corporate equities. Data up to 3Q17.

Inflation Figures will Drive Near-Term Direction of the Market

Returning to the near-term direction of markets, a key data point for obvious reasons will be the next average hourly earnings growth data point, which is due to be reported on March 9. The view here is that if US wage growth continues to accelerate in the manner reported last month (up 2.9%YoY), then markets will assume inflation is coming back even if core CPI does not pick up in a commensurate manner.

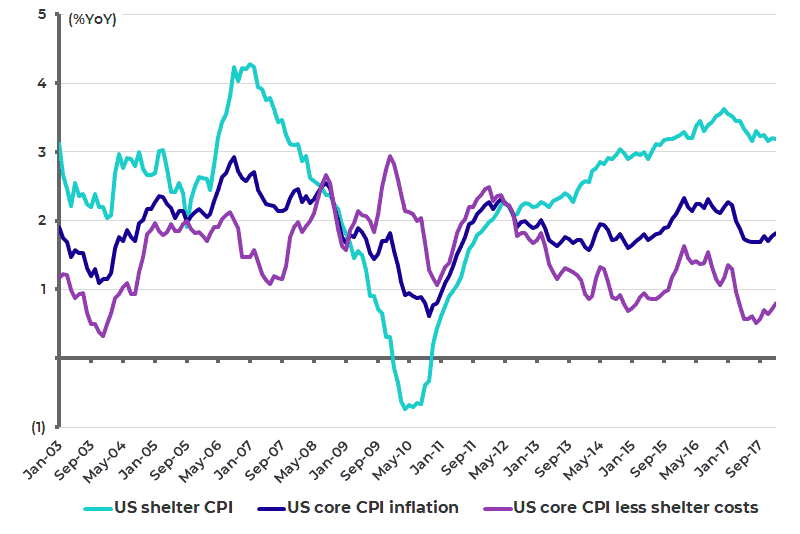

That said, the latest US inflation data released on February 14 has provided more than enough evidence for the return of inflation story to keep running for now, with the Bureau of Labour Statistics (BLS) describing the pricing pressures as ‘broad based’. Headline and core CPI rose by 0.5%MoM and 0.3%MoM respectively in January, up from 0.2%MoM in December. But on a year-on-year basis core CPI remained unchanged at 1.8% YoY (see following chart).

US Average Hourly Earnings Growth

US Core CPI Inflation

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.