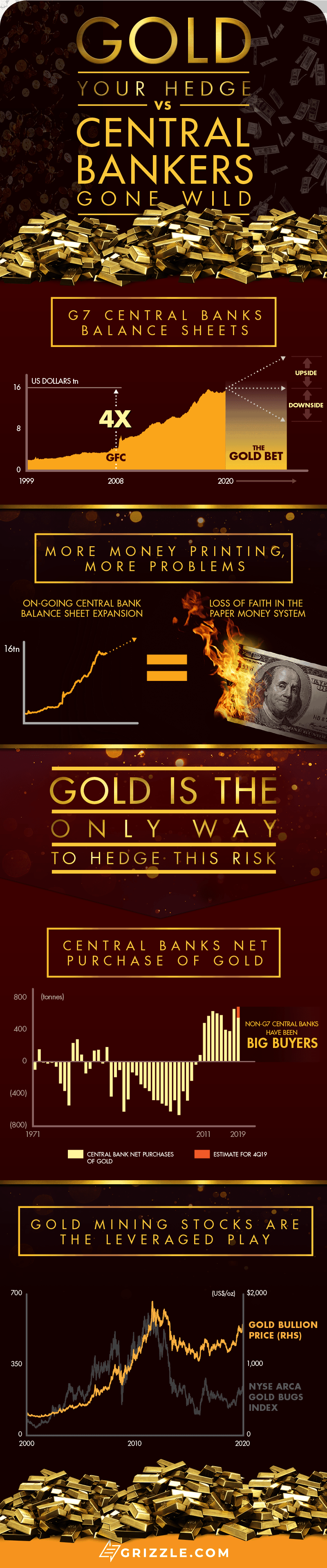

Gold has corrected by 2.4% off the intraday high of US$1611/oz on Jan. 8 triggered by the assassination of Iranian general Qassim Soleimani on Jan. 3 (see following chart). This is no surprise to me since the main reason to have a structural investment in gold is not to hedge the risk of rising geopolitical tensions but rather to bet on the view that G7 central banks will not be able to normalize monetary policy.

Gold Bullion Price

The Rise of Gold

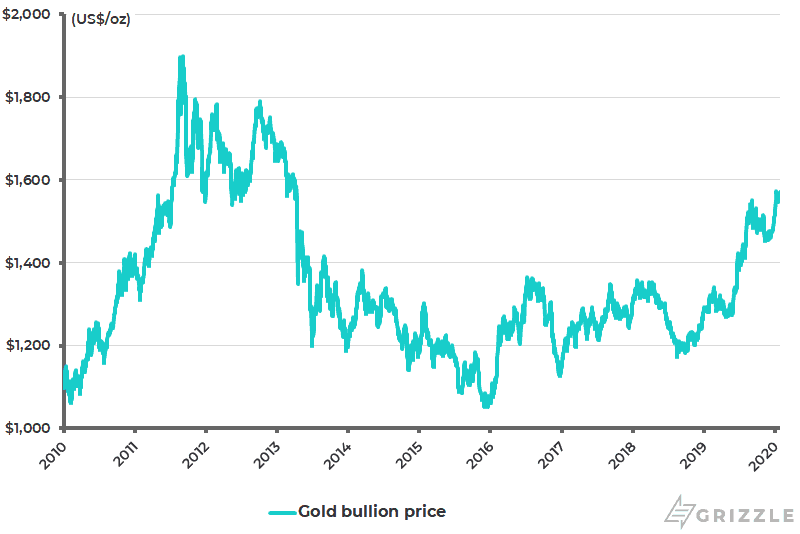

The main story in the markets last year was the Powell Fed’s abandonment of its attempt to normalize monetary policy. This is why it is entirely appropriate that gold rallied in 2019 and why it’s a very positive signal for the gold price that gold stocks outperformed to the extent they did.

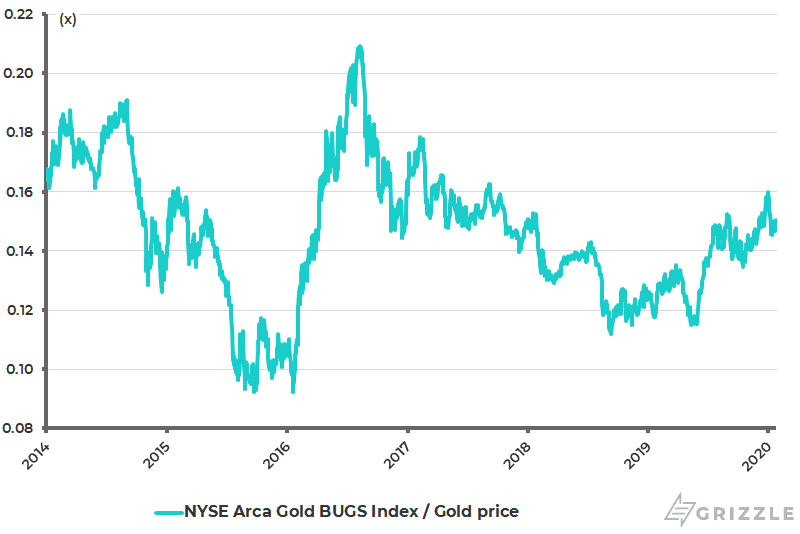

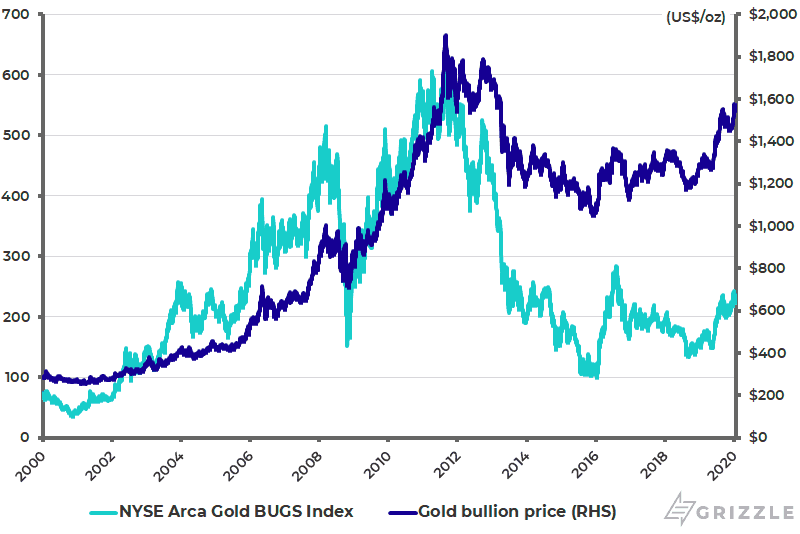

Gold bullion rose by 18.3% last year while the NYSE Arca Gold BUGS Index surged by 50.7% (see following chart). The main reason for gold’s rise was the decline in U.S. real rates. The real 3-month T-bill rate, deflated by core CPI inflation, fell from 0.3% in May 2019 to a negative 0.7% at the end of 2019 (see following chart).

NYSE Arca Gold BUGS Index Relative to Gold Price

U.S. Real Interest Rates Deflated by Core CPI Inflation

It’s Easy to Expand the Balance Sheet But Not So Easy to Contract It

The long-term case for gold is that the G7 central banks will not be able to exit unconventional monetary policy. This is because the view here remains that central banks, including most importantly the Federal Reserve, will not be able to exit from unconventional monetary policy in a benign manner and will ultimately remain committed to ongoing balance-sheet expansion in one form or another, just as both the ECB and the Fed renewed balance sheet expansion last year.

Such policies will increasingly risk discrediting those central banks which have pursued unconventional monetary policy since the global financial crisis, threatening the stability and indeed integrity of the current fiat-paper-money system. As for gold mining stocks, they remain the geared way of investing on such a view. They were trading at the end of 2015 at 2002 levels, when the gold price was only US$310/oz. They are now trading at November 2005 levels when the gold price was around US$480/oz (see following chart).

NYSE Arca Gold BUGS Index and Gold Price

The fundamental view here remains that it is much easier to enter unorthodox monetary policy regimes than to exit from them. Indeed, the longer-term risk is that unorthodox monetary policy spreads from the developed world to the emerging world, though hopefully such an outcome can continue to be avoided.

Is the Dollar Paper Standard on Its Last Legs?

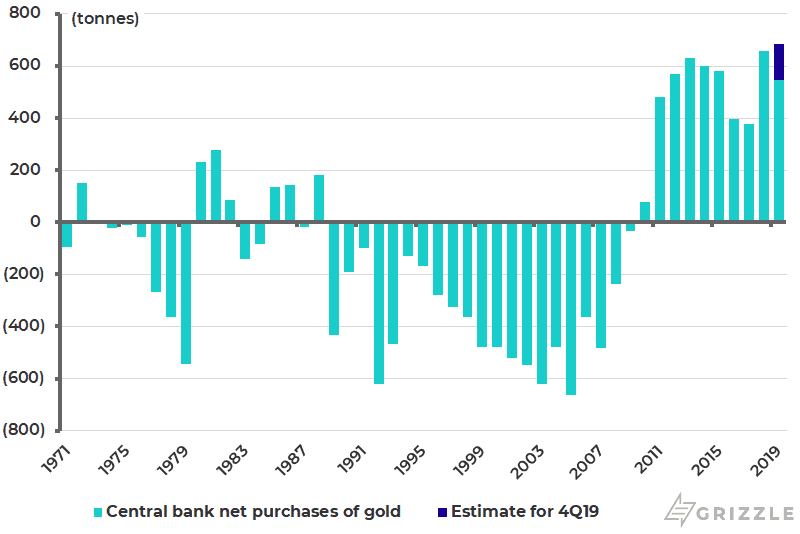

If this is the long-term view, that many central banks now share the view that the dollar paper standard is living on borrowed time is suggested by the big increase in central bank buying of gold last year. Central bank net purchases of gold rose by 11.6% YoY to 547.5 tonnes in the first three quarters of 2019, according to the World Gold Council (see following chart).

Based on the average net buying of 136.5 tonnes in the fourth quarters of the previous six years, Bloomberg estimates that central bank net purchases of gold will have reached a new record of 684 tonnes in 2019, up from the previous record of 656 tonnes reached in 2018.

Global Central Bank Net Purchases of Gold

However, it should be noted that the central banks buying gold were not the G7 mob who, as already noted, have been indulging in the hugely irresponsible exercise in unorthodox monetary policy over the past decade and more. In this respect, it is to the credit of the People’s Bank of China that it has maintained a consistent criticism of quantitative easing ever since the policy was first launched in late 2008 by former Fed chairman Ben Bernanke, as reflected in an article written by then PBOC Governor Zhou Xiaochuan in a BIS publication in 2009 (see BIS article: “Reform the international monetary system” by Zhou Xiaochuan, March 23, 2009).

Zhou called in that article for reform of the world’s monetary system. That proposal remains as sensible as ever more than ten years on. But the likelihood is that such a reform will only be forced by a crisis. And gold remains the best way of hedging such a crisis, the timing of which is unknowable.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.