Macro Battleship has lauded the merits of investing in emerging markets. This week the focus will be on one specific country, namely Vietnam. This is a booming economy driven by surging foreign direct investment (FDI) and a stock market that has finally become investible from the standpoint of foreign investors.

Stretched Over the Near-term, Sizable Long-term Upside Remains

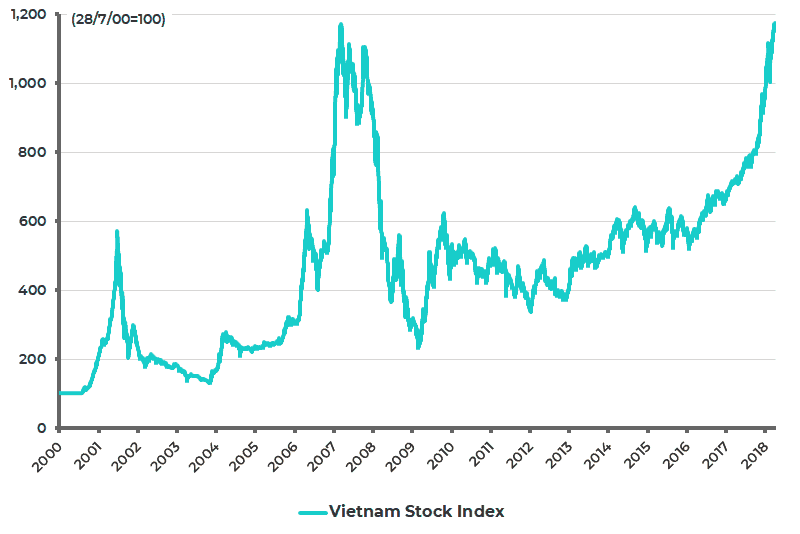

The benchmark Vietnam Stock Index is up 76.6% in the past 15 months and is now marginally above its 2007 peak (see following chart). Is the story peaking? Maybe in the short-term given high valuations for the leading stocks, most particularly if global markets correct again.

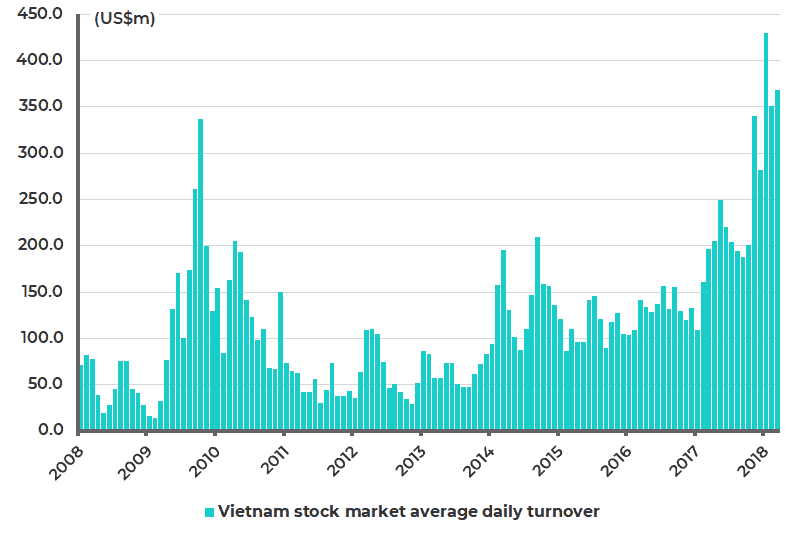

Still, the overall market is not so extended, trading at around 17x forecast 2018 earnings in the context of 25% forecast earnings growth. Meanwhile average daily trading volumes have been surging (see following chart) as the market has risen with the stock market capitalization now totaling US$191 billion.

Vietnam Stock Market

Vietnam Stock Market Average Daily Turnover

Next Stop: Inclusion for MSCI Emerging Markets Index

Amidst this bullish backdrop, there are growing hopes that the market will be included in the MSCI Emerging Markets Index on a two-year view. But this will require action on two fronts, foreign ownership limits and privatization.

The first is by far the most important with the limit still 30% for bank stocks and 49% for many other companies. Still there has been one positive development. Companies can since September 2015 unilaterally raise their foreign limits if they’re not in core strategic sectors such as banking and telecoms. And so far about 30 companies have elected to do so.

What about privatization, or ‘equitization’, as it is called in Vietnam? Here there has finally been significant progress over the past year after years of disappointment.

State IPOs and other divestments have totaled US$8 billion since 2014. The largest deal was the US$4.8 billion raised from the sale of a 54% stake in state-owned brewer Sabeco last December. The privatization pipeline for 2018-19 is currently US$12.5 billion. In a further sign of an increasingly active capital market, there are US$3 billion of private sector IPOs and placements scheduled so far for this year.

Foreign Direct Investment the Crucial Driver

The looming supply may be a potential negative from the standpoint of current share prices. But the critical point is that Vietnam’s capital markets are finally beginning to catch up with the dynamism of the macroeconomic story, which is all about the FDI boom and the related consumption story represented by a growing middle class. The combination makes Vietnam by some distance the best macroeconomic story at present in Southeast Asia.

The reason why is that Vietnam has been by far the most successful of the economies in this region in attracting foreign direct investment in recent years as multinationals have looked to diversify away from a total reliance on manufacturing in increasingly expensive China.

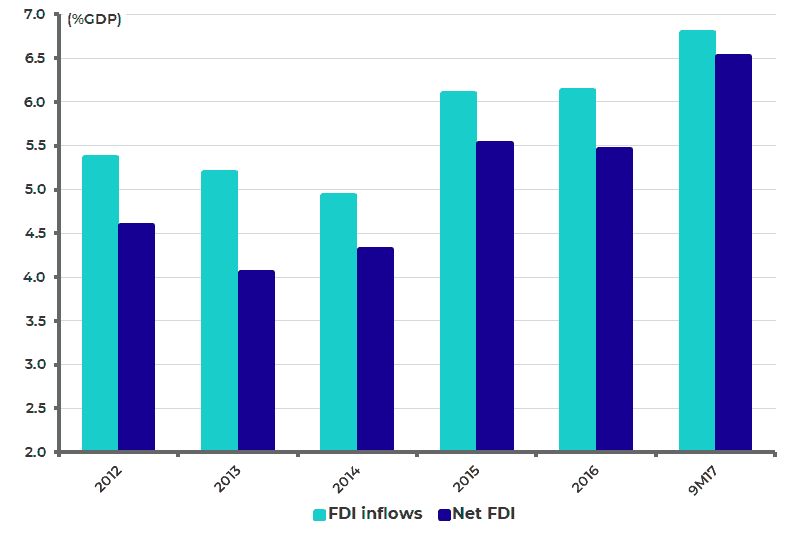

FDI inflows into Vietnam totaled US$10.1 billion in the first three quarters of 2017 or 6.8% of GDP, up from 4.9% of GDP in 2014, according to balance of payments statistics (see following chart). The dominant sector is communications technology with exports of mobile phones accounting for 21% of Vietnam’s total exports.

Vietnam Balance of Payments: FDI Inflows and Net FDI

Consumption Boasted by Stable Currency and Inflation

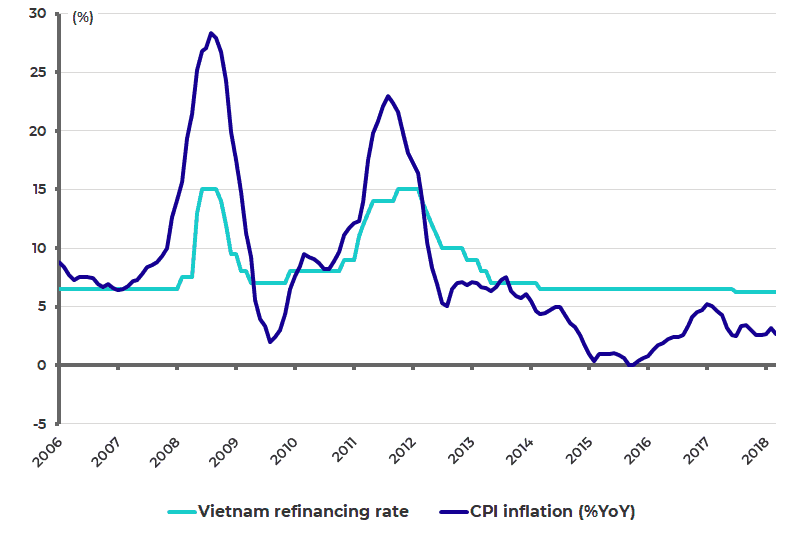

This macro backdrop is driving a consumption boom, helped by a stable currency and interest rates which remain way below the levels prevailing when inflation spiked seven years ago.

The State Bank of Vietnam’s refinancing rate is now 6.25% — down from the peak rate of 15% reached in 2011 and 2008. CPI inflation was 2.66% YoY in March, compared with the 28.3% and 23% peak levels seen in 2008 and 2011, respectively (see following chart).

The banking system has also been slowly working off a NPL problem left over from a previous boom-bust cycle. The NPL problem peaked at about 25% of loans in 2012 and is now estimated at about 8% of loans, a recovery process driven partly by loan write-offs and partly by new lending.

Vietnam Refinancing Rate and CPI Inflation

Strong but Stable Credit Growth Coupled with Current Account Surplus

Meanwhile, credit growth is back running at healthy levels relative to nominal GDP growth. Bank credit rose by 18% YoY in 2017, while nominal GDP increased by 11.2% YoY.

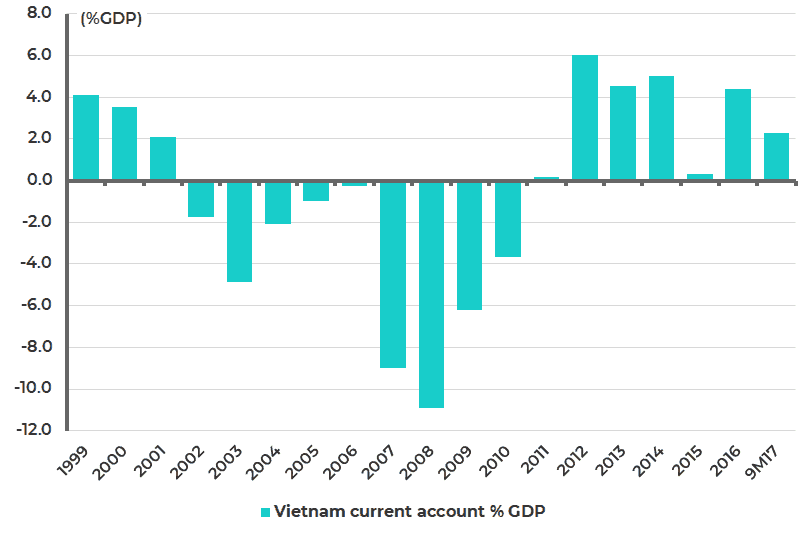

But there is no sign yet of the extended period of excessive credit growth that led to the previous bust. It’s also the case that a continuing stable ‘dong’, the name of the local currency, is supported by a current account surplus, which is the consequence of the FDI-driven export boom. Vietnam has been running an average current account surplus of 3.7% of GDP since 2012 (see following chart).

Vietnam Current Account as % of GDP

Improving Political Backdrop

Finally, a word is due on Vietnam politics, a topic that is generally not well reported in international media. Vietnam has of late had its own version of China’s anti-corruption campaign, albeit on a much less dramatic scale. The important development here was the January 2016 Five-Year Party Congress, which saw the surprise removal of former Prime Minister Nguyen Tan Dzung who was seen as too power hungry.

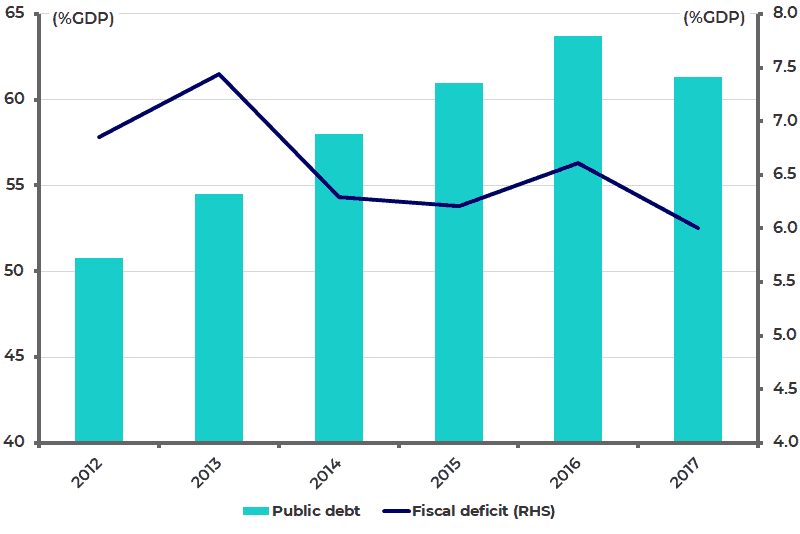

The result was a reassertion of collective leadership under Party General Secretary Nguyen Phu Truong, which has now resulted in a consensus on equitization, a process partly driven by the perceived need to boost government coffers as a result of fiscal deficits running at an average of 6.6% of GDP for the past six years (see following chart).

Vietnam Public Debt and Fiscal Deficit as % of GDP

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.