What about the U.S. presidential election next year? It remains way too early to start pontificating on outcomes. But, at this point, it makes sense to observe that Elizabeth Warren is by far the most credible candidate offered by the Democrats. And, she is probably the candidate The Donald would least like to go up against. By contrast, he will probably regard the nominal leader in the Democrat polls, “Sleepy Joe” Biden, as a pushover. In this respect, the Biden family are as likely to be damaged by the impeachment launched against the 45th American president as much as Trump himself.

It is hard to conceive 20 Republicans voting against Trump in the Senate. Meanwhile, the obvious way forward for Warren is for the eccentric Bernie Sanders to retire from the fray later in the primary season and endorse Warren.

A Revived U.S. Stock Market

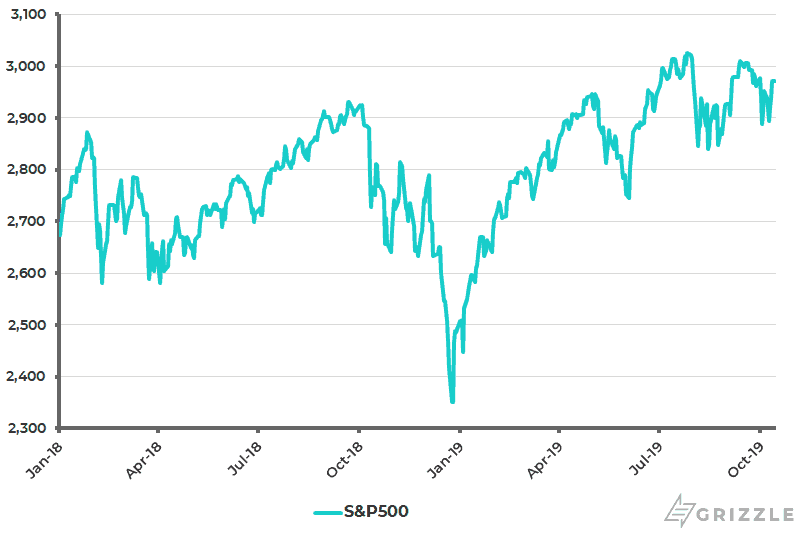

Meanwhile, expectations of Friday’s news of a delay in the implementation of the tariff hike scheduled for Oct. 15 have helped revive the American stock market of late, with the S&P500 only 1.9% off its record high reached in late July (see following chart). I would remain scared to short the S&P500 because of the risk of further progress on trade, as well as the continued reality of renewed Fed easing. But I would also not want to own it.

The collective insanity driving current U.S. stock market behaviour was highlighted in an article in the Financial Times late last month, which noted that the standout hedge fund trade this year has been “computer-driven trend-followers” (see Financial Times article: “Tail Risk: Why robots see no logic in betting against central bankers” by Laurence Fletcher, Sept. 25 2019). The article stated: “Such funds do not balk at highly priced assets but instead latch on to trends in the market, wherever they lead. That has been a smart strategy.”

S&P500

Reported Earnings Don’t Line Up With Actual Profit

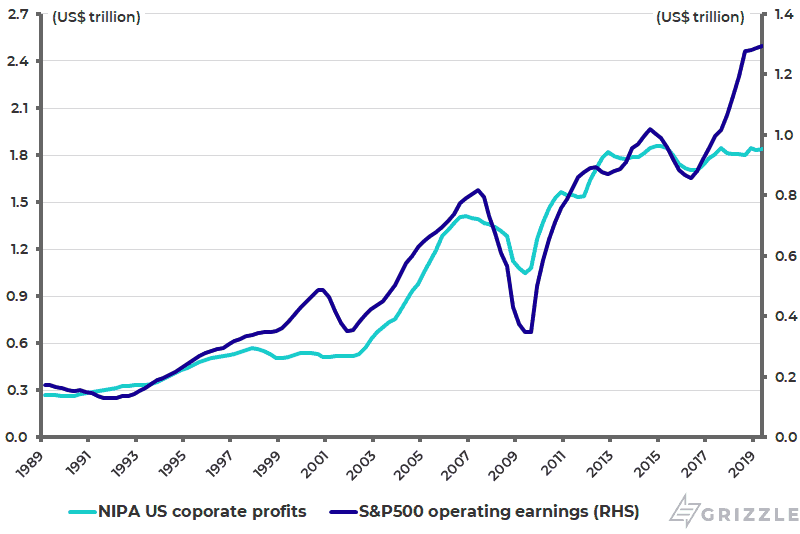

Such a comment speaks for itself. I will simply point out, once again, that the 10-year-old equity bull market is primarily about leveraged financial engineering. The fundamental risks can be highlighted by the unprecedented gap between the macro measure of profits recorded in the national accounts and reported profits.

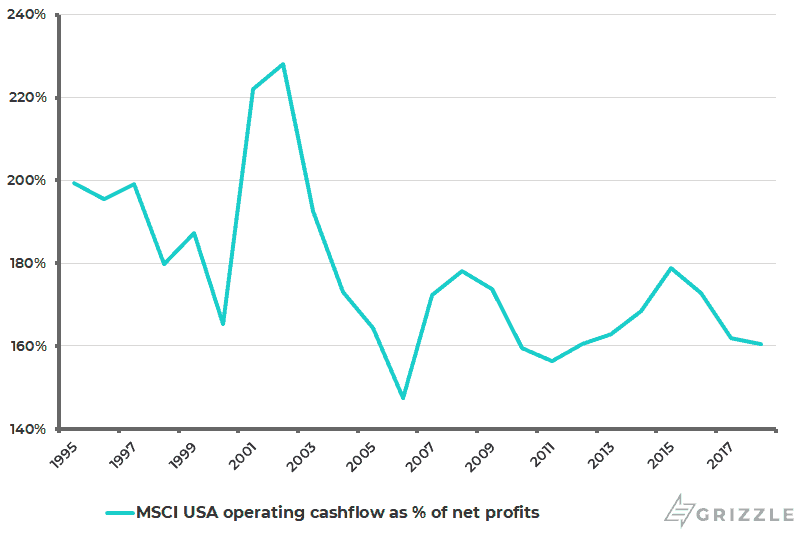

The S&P500 operating earnings have risen by an annualized 16% over the past three years, while the national accounts’ measure of U.S. corporate profits after tax is up only an annualized 2.4% over the same period (see following chart). Another way the same risk can be highlighted is the decline in operating cashflow as a percentage of reported earnings. The MSCI USA universe’s operating cashflow to net profits ratio has declined from a peak of 228% in 2002 to 160% in 2018 (see following chart). This is all happening at a time when U.S. profit margins looked to have peaked and non-financial corporate sector debt is at a record high.

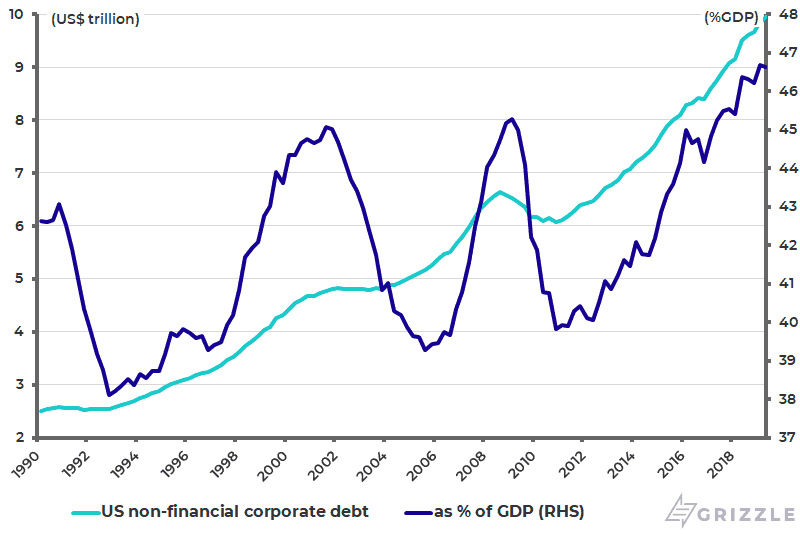

The S&P500 operating profit margin rose from 8% in 4Q15 to a record 12.1% in 3Q18 and was 11.4% in 2Q19. U.S. non-financial corporate sector debt rose by 4.6% YoY to a record US$9.95 trillion or 46.6% of GDP at the end of 2Q19 (see following chart).

U.S. Corporate Profits After Tax and S&P500 Operating Earnings

MSCI USA Operating Cashflow as % of Net Profits

U.S. Non-financial Sector Corporate Debt

If the fundamental risks in U.S. equities are obvious, the obvious catalyst to trigger a problem has been removed, namely monetary tightening. In fact, the Fed is likely to cut again this month. In the meantime, investors, many of them machines, can continue to take the reported EPS at face value. So-called high frequency trading accounts for 50% of average daily trading volume and active fund managers for less than one-third. “Passive” investors, or indexing, comprise the bulk of the balance.

The other medium-term risk for the American stock market is the, for America, very socialistic policies of Warren if she is elected. With the election still a year away, this is not an immediate issue. But will Americans really vote for socialism?

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.