We believe the lithium market is one of the most attractive in the mining & materials sector, and we view SQM (NYSE:SQM) as the most undervalued, high-quality company in the space. The macro tailwinds are compelling, however, it’s the valuation disconnect that makes this one of the most attractive risk/reward propositions in the market today in our view.

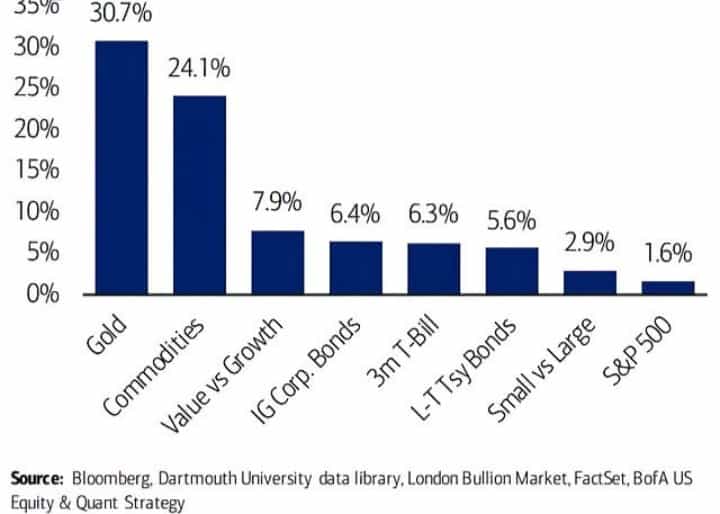

Metals Protect Against Inflation

The last time inflation ran this hot was in the 70s, it was a period when commodities worked very well, 24% annual returns.

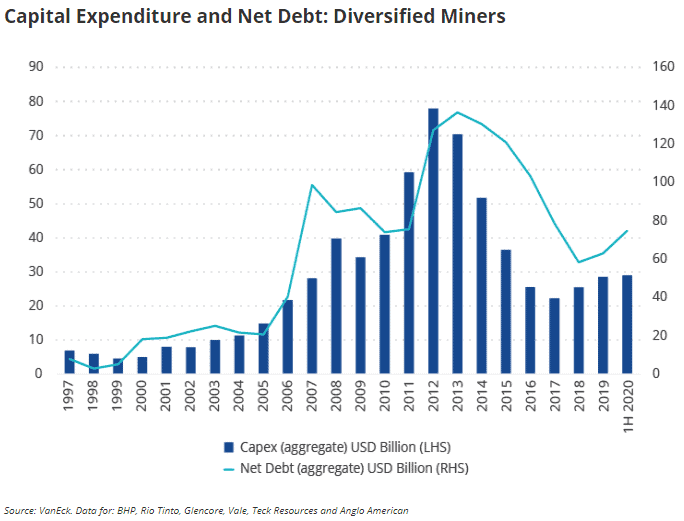

The setup looks just as attractive right now with mining capex at cycle lows, the supply to meet demand simply isn’t there.

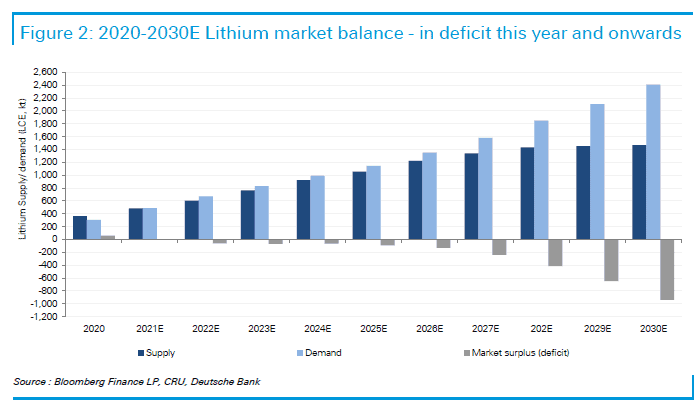

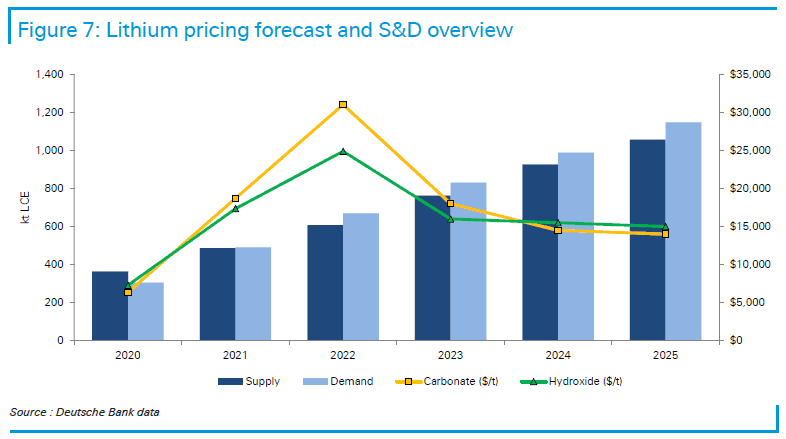

Lithium: Attractive Supply & Demand Outlook

The lithium market is currently in deficit (demand exceeding supply) and is forecast to continue to be in a deficit position till the end of the decade.

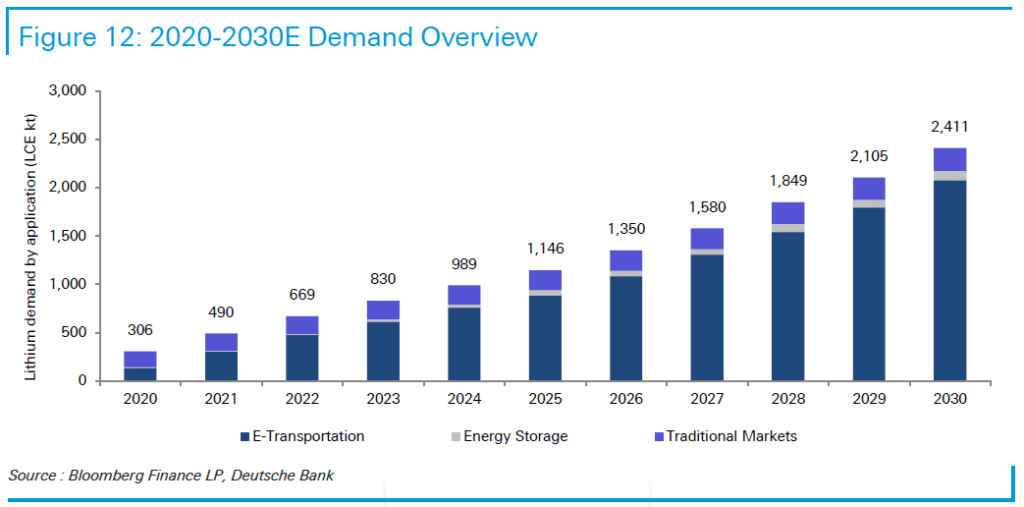

The strong demand for electric vehicles underpins the bullish outlook for lithium. Over the next decade lithium demand will increase 5x by 2030 primarily driven by the strong demand from electric vehicle batteries.

This backdrop is very supportive of strong lithium prices over the coming years.

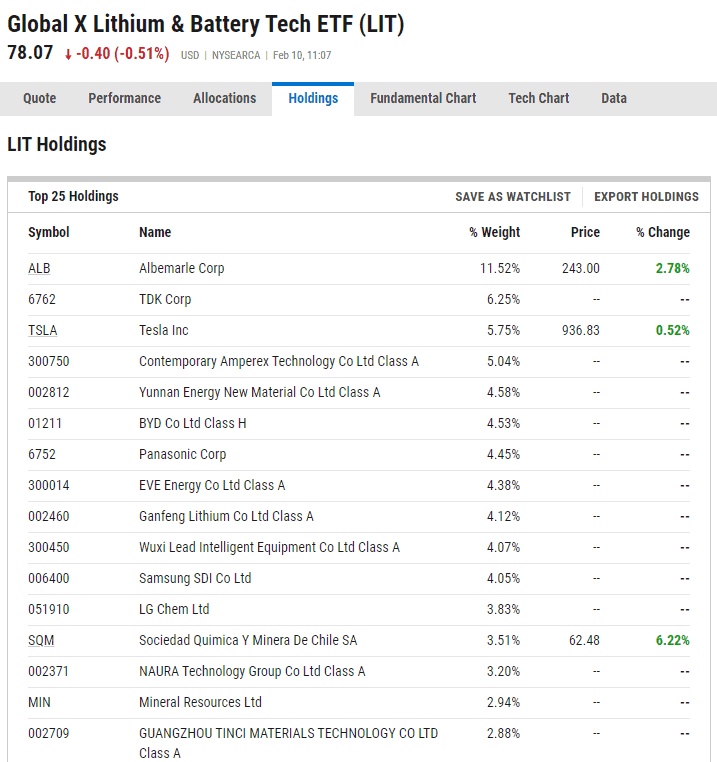

The Curious Case of the $5 billion Lithium & Battery ETF

As retail traders and advisors rushed to gain lithium exposure last year they poured billions into the Global X Lithium & Battery Tech ETF (NYSE:LIT).

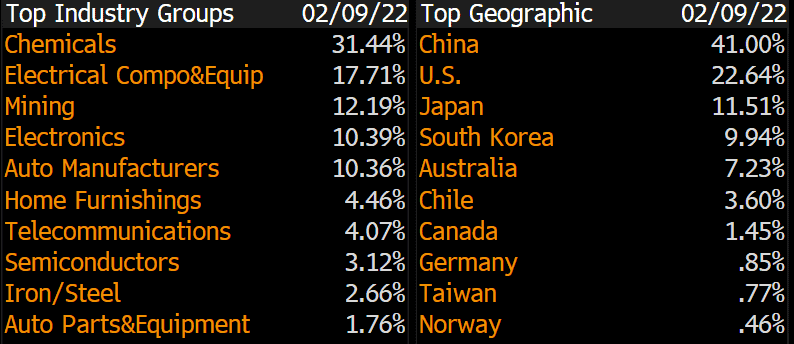

Yet the most basic scan of the holdings should have raised red flags to potential investors; the top holdings are dominated by Chinese domiciled companies.

In fact, China dominates the geographic exposure of the ETF at 41%, a sector distribution that leaves us scratching our heads – a lithium ETF with 4.4% exposure in home furnishings, really?

LIT ETF Sector & Country Exposure

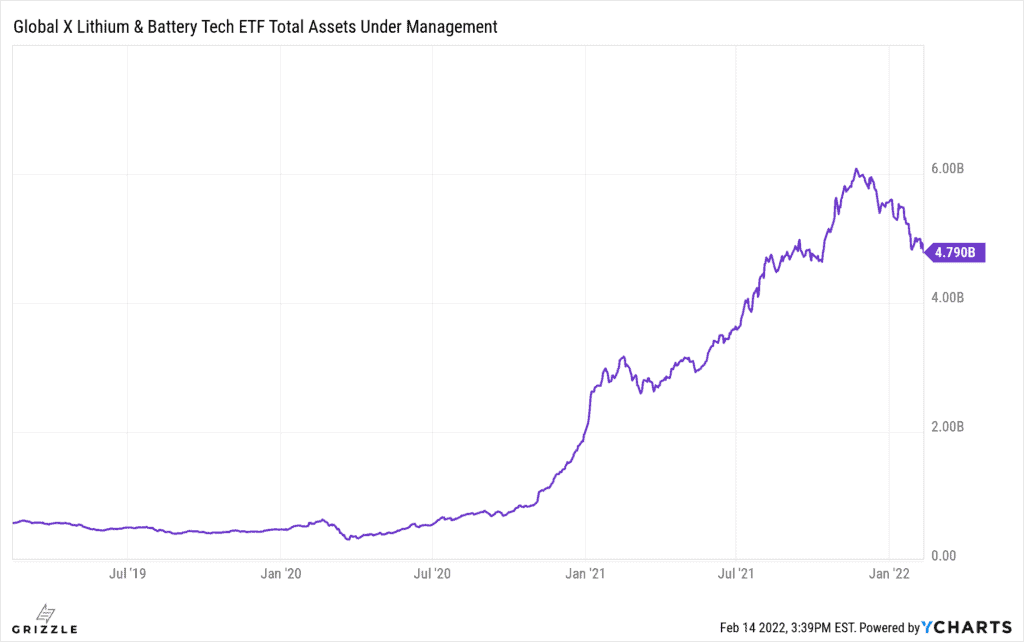

This ETF’s AUM grew 10x in 2 years; in what we can surmise as blind retail fast money, buying whatever was said on the tin and not bothering to look inside.

This scale of hot money has created significant valuation dislocations in the lithium sector.

Simply put, too much money when into opaque Chinese producers and not enough into legitimate producers.

LIT ETF Assets Under Management

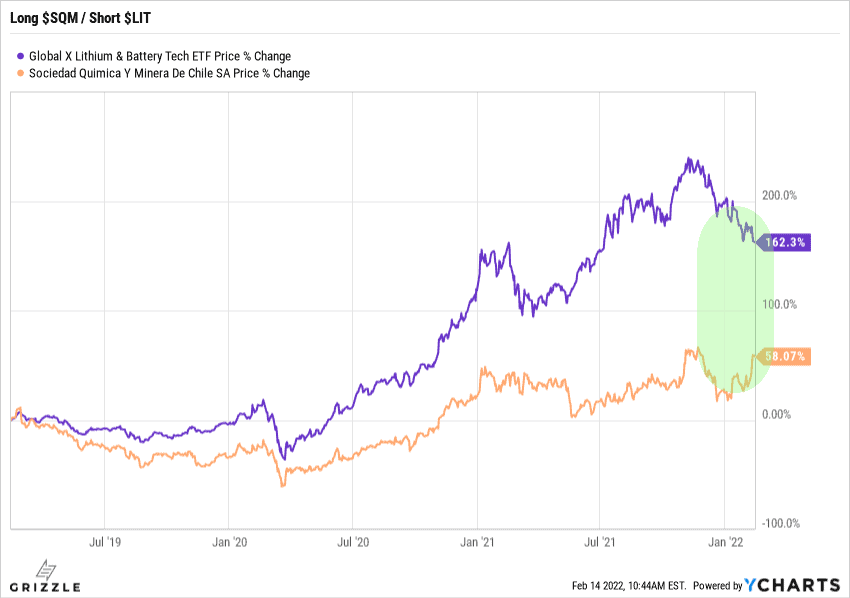

SQM – The Big Lithium Valuation Catchup Trade

The thesis for SQM is very straightforward. One of the world’s top lithium producers, fundamentally undervalued versus it’s main competitor Albemarle (NYSE:ALB).

We believe there’s a switch trade for holders of the LIT ETF to SQM, additionally, we believe there’s an attractive long/short trade for hedge funds – Long SQM / Short the LIT ETF.

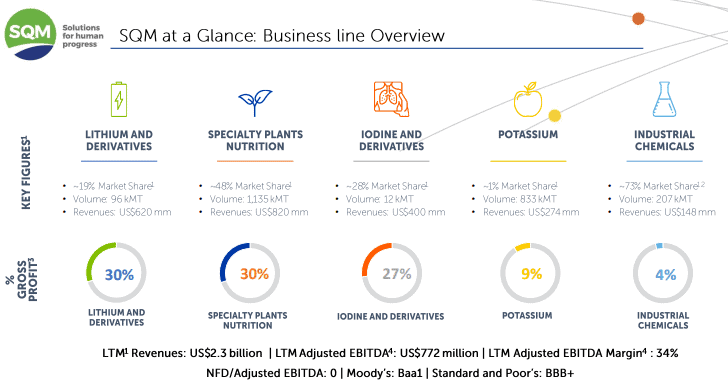

The lithium division represents 30% of SQM’s gross profit (last 12 months); by 2023 the lithium division will account for 51% of revenue and 59% of EBITDA.

SQM Gross Profit by Business

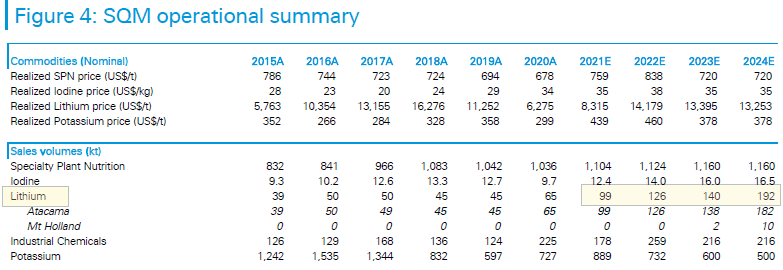

By 2024 SQM will have doubled its lithium production volume to 192 kt, this provides meaningful insulation against price volatility.

Revenue and profits can still grow even in the face of a reversion in Lithium prices.

The undervaluation thesis on SQM is very clear cut, versus Albemarle – SQM trades at a 60% discount on EV/EBITDA, 60% discount on P/E, and 70% discount on P/Cashflow.

Additionally, the company has a 30% Return on Equity; 19% higher than Albemarle.

We can comfortably get to a target price of $120/share vs. $64/share today – 90% upside.

SQM Valuation Disconnect to ALB

Disclosure: The Grizzle Growth ETF (Ticker: GRZZ), managed by the Author Thomas George, owns shares in SQM. Please visit Etf.grizzle.com for more details and disclosures about the fund.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.