The fixed income market has been the best way for equity portfolios to hedge the undoubted negative impact on growth of the Wuhan Coronavirus.

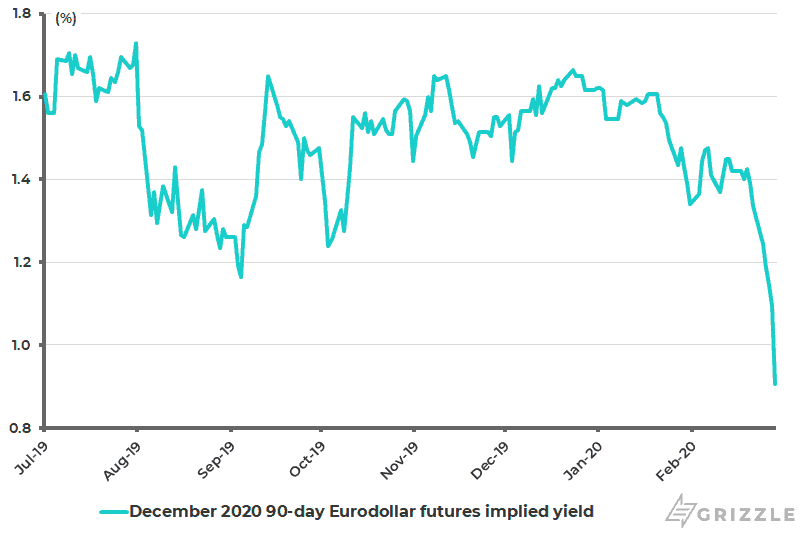

The Eurodollar future is now discounting a 75bp cut in the federal funds rate this year (see following chart), as opposed to zero cuts before the virus newsflow hit. Both the U.S. and Chinese government bond yield curves have flattened significantly.

Declining Treasury Bond Yields

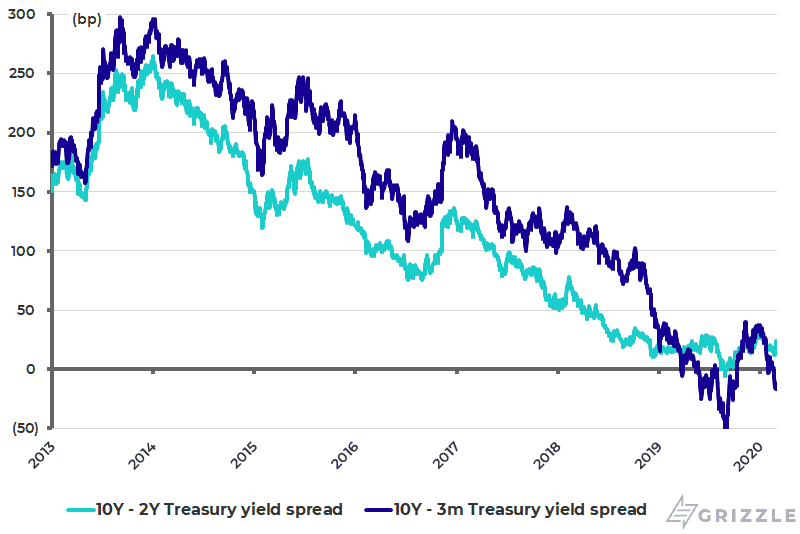

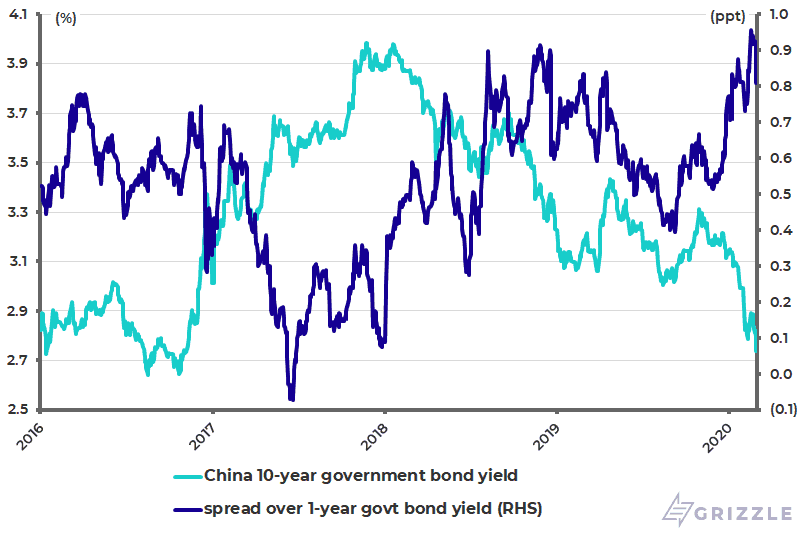

The U.S. 10-year 2-year Treasury bond yield spread and the 10-year 3-month Treasury yield spread have declined from 35bp and 37bp respectively at the start of this year to 24bp and -12bp, though up from the recent lows of 12bp and -17bp reached earlier last week (see following chart). While the spread between China’s 10-year and 1-year government bond yields has also declined by 15bp since Feb. 17 to 81bp, with the 10-year yield falling by 16bp to 2.74% over the same period and down 40bp year-to-date (see following chart).

December 2020 90-day Eurodollar Futures Implied Yield

U.S. Yield Curves

China 10Y-1Y Government Bond Yield Spread

The Effect of the Coronavirus on Markets

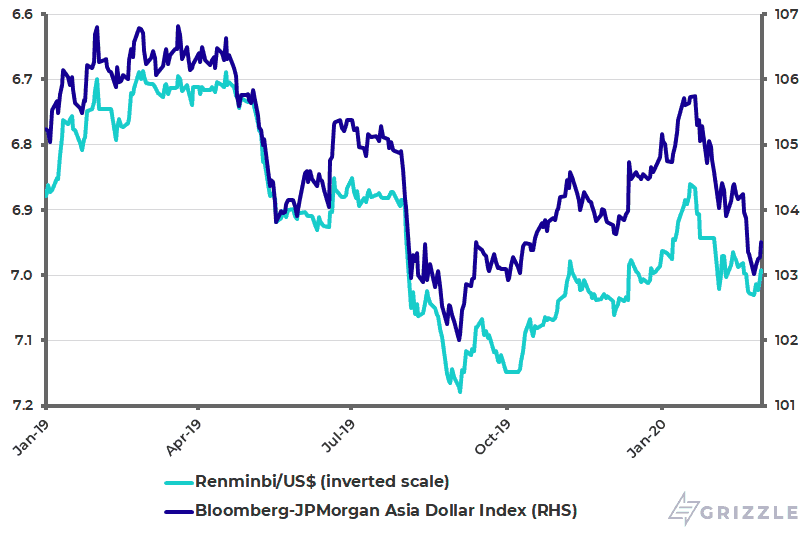

So, the outbreak of the virus has hit the pro-cyclical positions adopted by many investors at the start of this year. Chinese equities were breaking out technically just before the virus came to the world’s attention in mid-January, Asian currencies had started to rally against the U.S. dollar led by the renminbi, while oil and gas stocks got a bid, helped by the assassination of Iranian general Qassem Soleimani.

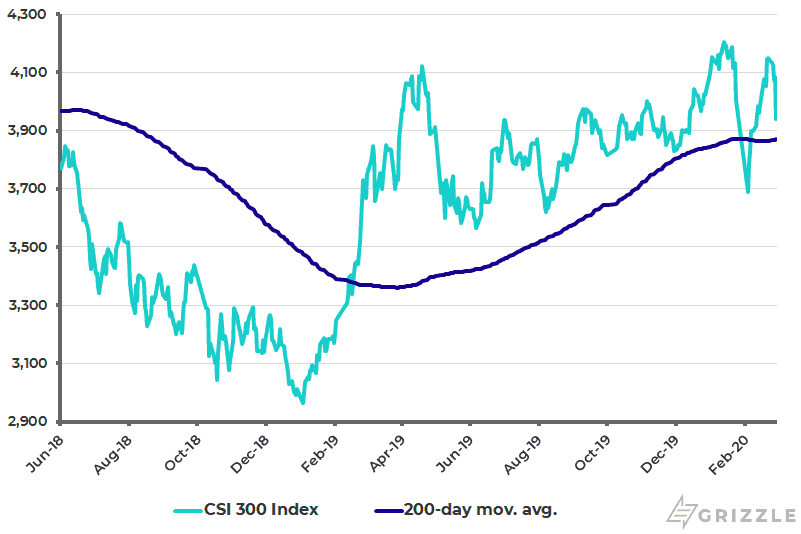

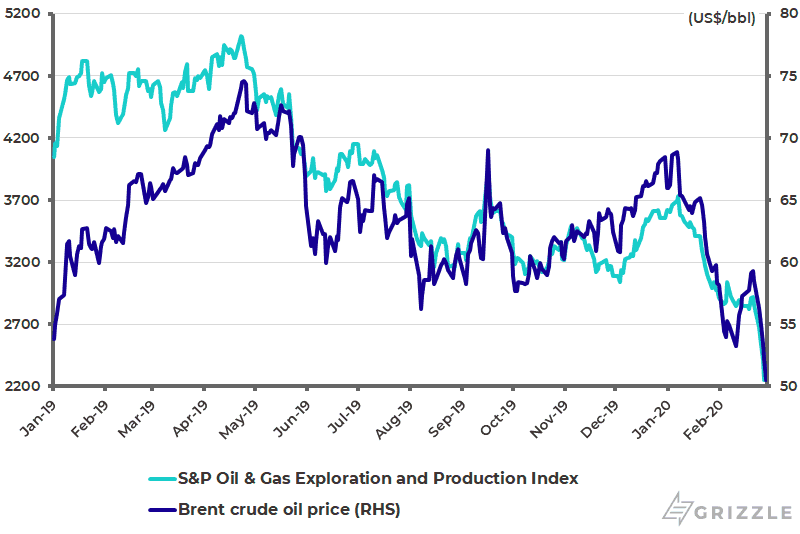

All these trades have since reversed and then some most spectacularly in the case of the oil price (down 23% since Jan. 20); though it has been a positive that the Shanghai stock market resumed trading as scheduled after the end of China New Year on Feb. 3 (see following charts).

China CSI 300 Index (A shares)

Asia Dollar Index and Renminbi/US$ (Inverted Scale)

Crude Oil Price and U.S. Oil Stocks

Just How Much of a Problem is the Coronavirus Now?

The critical issue now is whether the virus hits Chinese growth for only one quarter or whether it is longer. The positive point here is that the rate of infection has peaked while the main damage has been contained in Hubei province which is, unfortunately, a healthcare disaster.

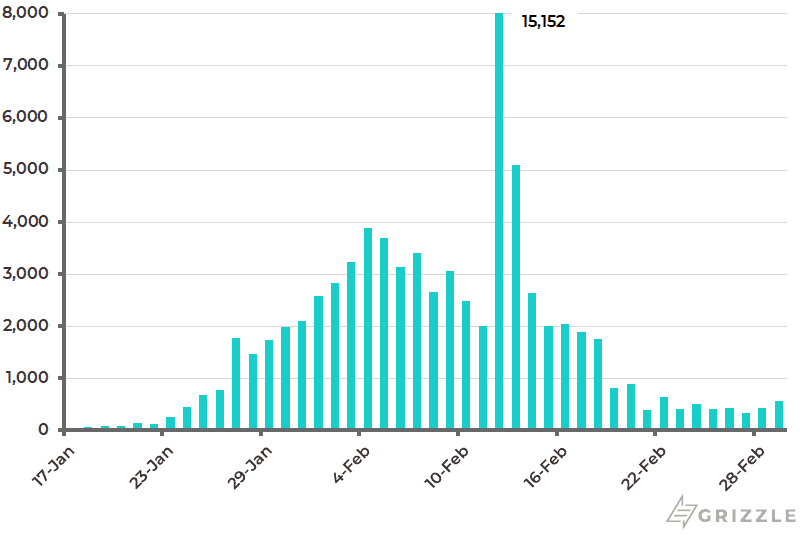

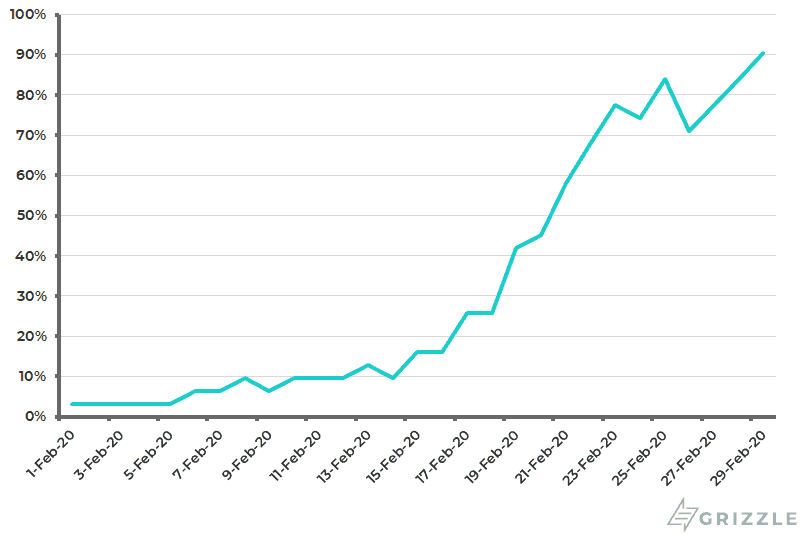

Thus, daily new confirmed cases in mainland China have declined from a peak of 3,887 on Feb. 4 to 573 cases on Saturday (see following chart), of which 570 cases were from Hubei province and only 3 new cases outside Hubei. As a result, 28 or 90% of the 31 provinces had no new cases on Saturday (see following chart). Hubei now accounts for 84% of the cumulative 79,824 infection cases in mainland China. Hubei has a population of 59 million.

The other point to note is that when the virus peaks the Chinese economy will be the one that bounces back fastest and hardest given this is where the restriction on movement has been the greatest. And for now the base case, if it was necessary to bet on it, is that the Coronavirus’ economic impact will likely prove to be primarily a one-quarter affair for China.

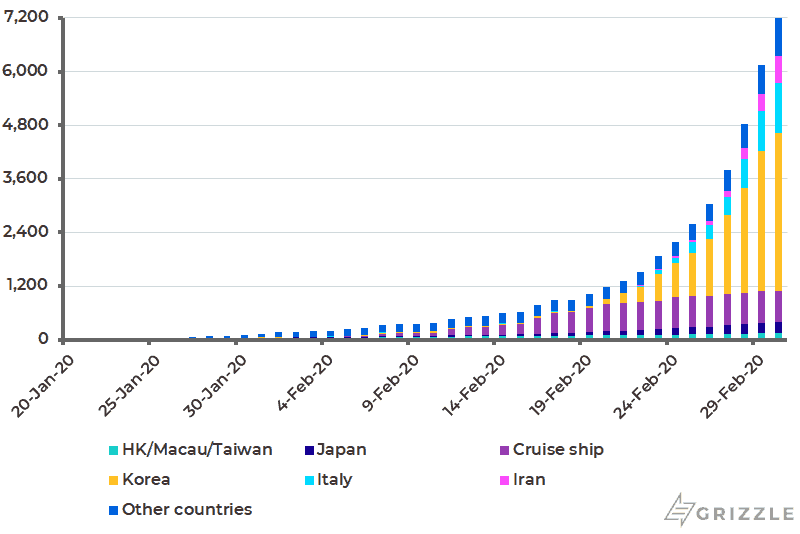

Having said that, even if that base case is right, the other threat is what has caused the panic selloff last week in Anglo-Saxon dominated financial markets? That is the increased infections outside China. On this point, as of Saturday, 77% of all infection cases globally were in Hubei and 92% in mainland China. The comparative data two weeks ago were 82% and 99%. Total infection cases outside mainland China have surged from 767 cases two week ago to over 7,198 cases as of Sunday morning (see following chart).

And the problem for markets is that it is far easier to control the spread of the virus in a political system like China’s rather than in Western liberal democracies. This is why investors will be hoping that the virus, which is a form of extreme viral flu, burns itself off when the weather turns warmer in the northern hemisphere.

Daily New Coronavirus Confirmed Cases in Mainland China

Share of Chinese Provinces with New Confirmed Cases

Coronavirus Cumulative Confirmed Cases Outside Mainland China

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.