As financial markets bet about the policies of the Trump administration, be it DOGE spending cuts or threatened tariffs, it is worth highlighting again the dramatic transformation going on in Argentina.

Argentina was discussed here 12 months ago (see Is Argentina’s Economic Experiment Working?, 18 March 2024).

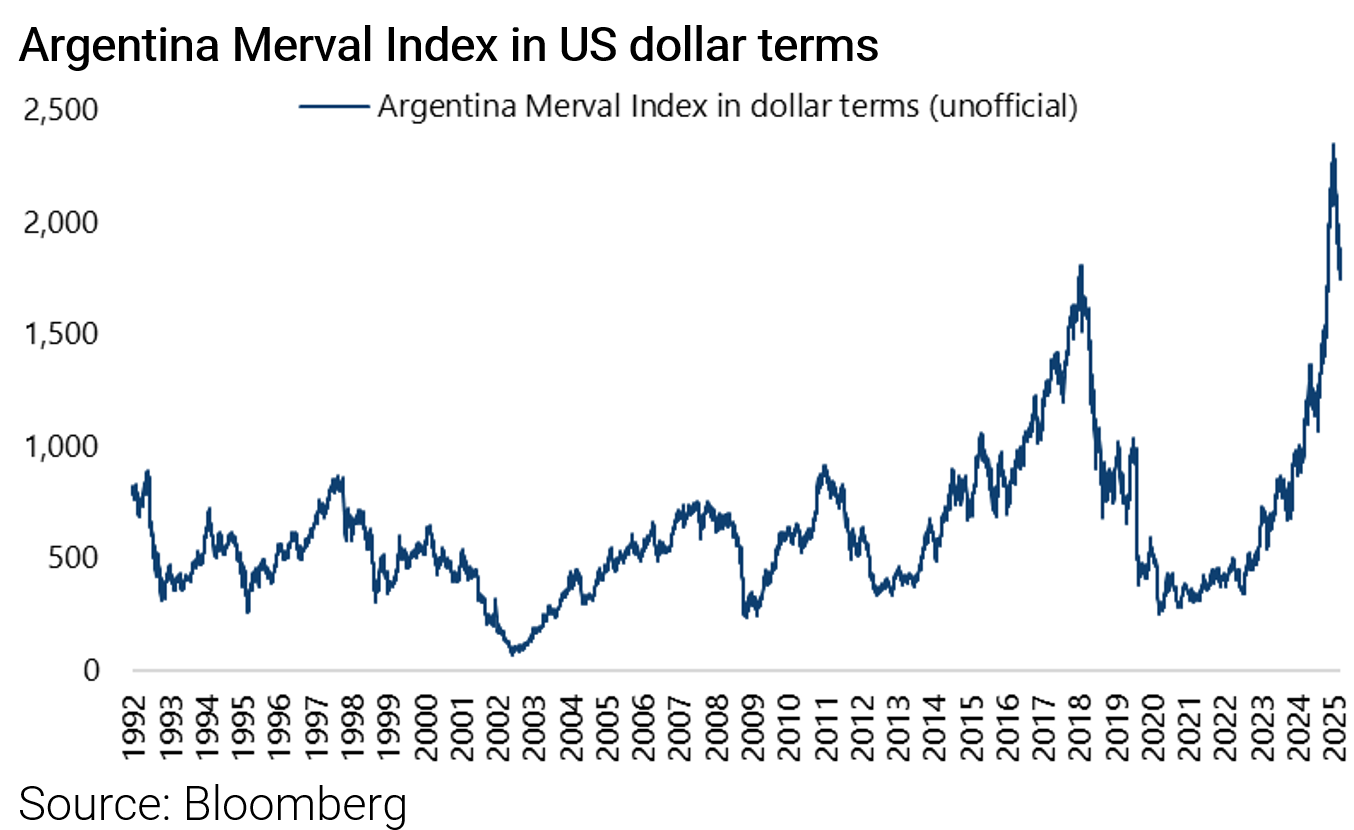

The bullish view on Argentine assets outlined then was more than confirmed by the surge in Argentine asset prices in 2024, both equity and debt.

The Merval Index rose by 122% in US dollar terms last year, while the Bloomberg Argentina US dollar sovereign bond index increased by 102%.

For the record, the Merval Index is down 12% in US dollar terms year-to-date, while the Argentina sovereign bond index is down 1.5%.

A more recent visit to Buenos Aires earlier this year has so far confirmed that President Javier Milei has surpassed the expectations not only of his critics but also of supporters of his programme.

In particular, the Argentine president has proved highly pragmatic politically in terms of the implementation of his radical policies even though his political party, La Libertad Avanza (LLA), has only 39 seats out of 257 in the Chamber of Deputies, the lower house of the National Congress.

Meanwhile, the macro adjustment has also surpassed all expectations, in terms of both how dramatically inflation has dropped but also how relatively unpainful the economic downturn has been.

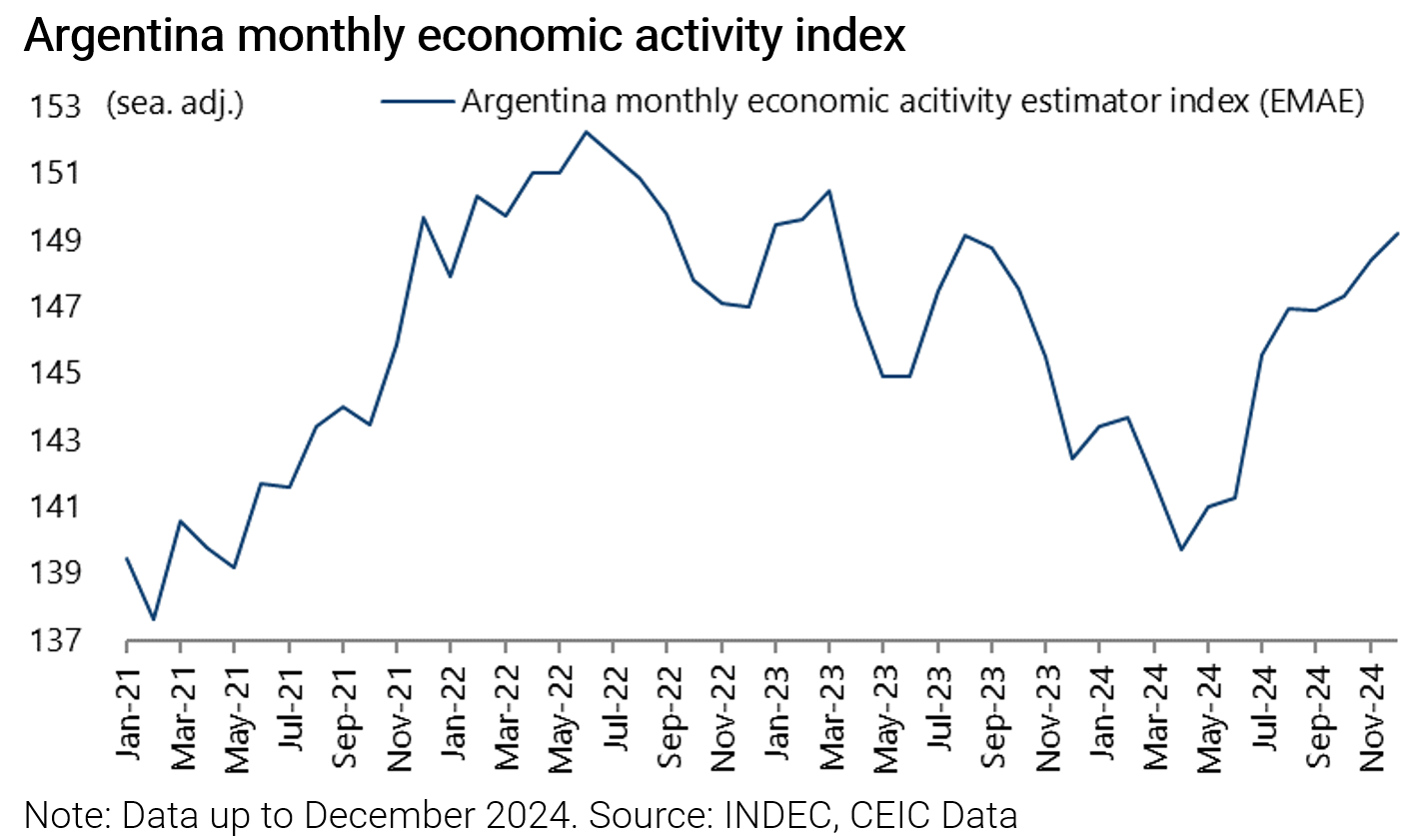

Growth began to pick up from as early as May last year, with the consensus forecasting a 2.9% decline in real GDP in 2024 and 4.3% growth in 2025.

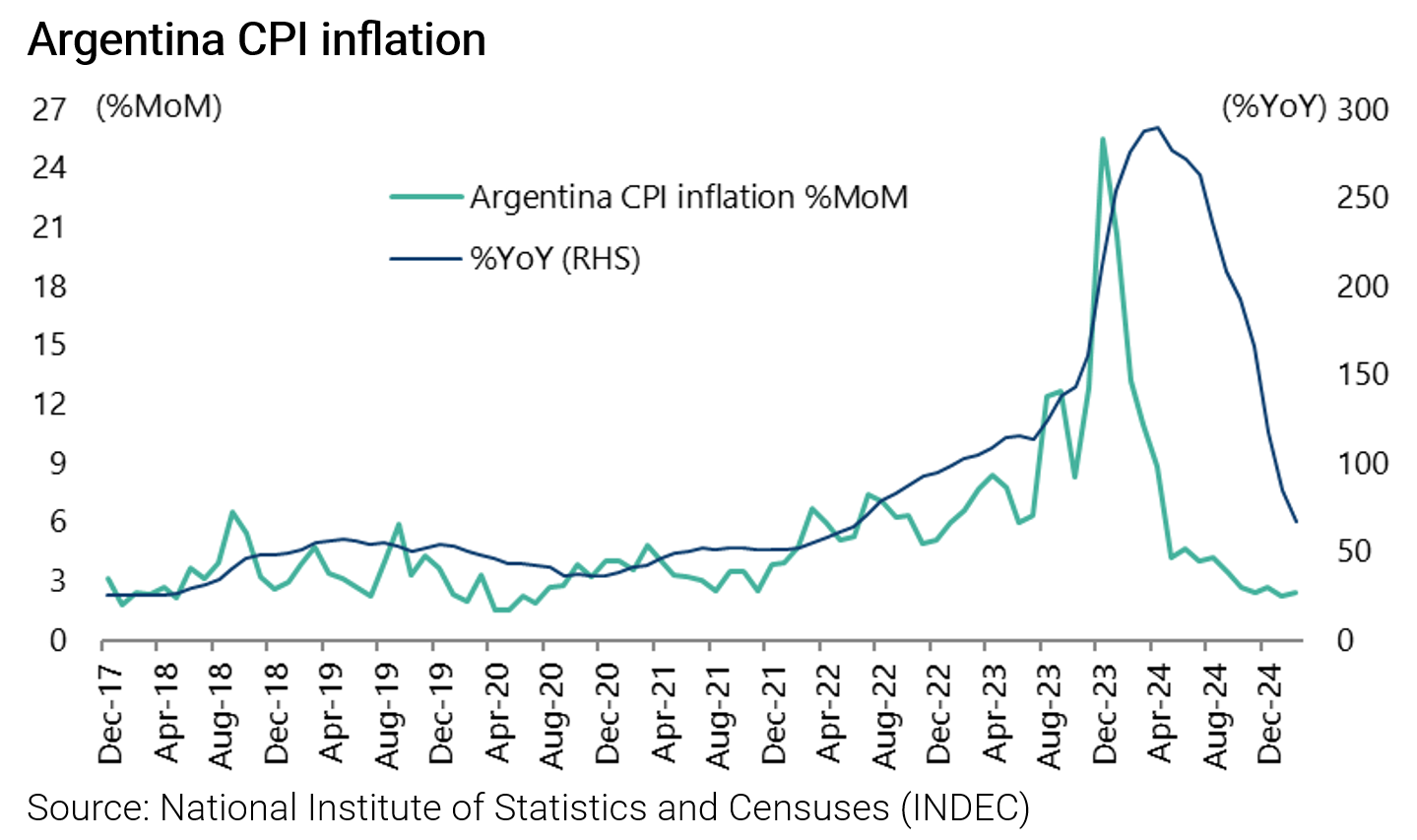

While inflation is down to 2.4% a month in February compared with the 25.5% monthly inflation rate which Milei inherited when he took office in December 2023.

The monthly economic activity index bottomed in April 2024 and has since risen by 6.8%.

This is all in the context of the macro adjustment process implemented by the self-described anarcho-capitalist, of which the core anchor has been a dramatic fiscal adjustment.

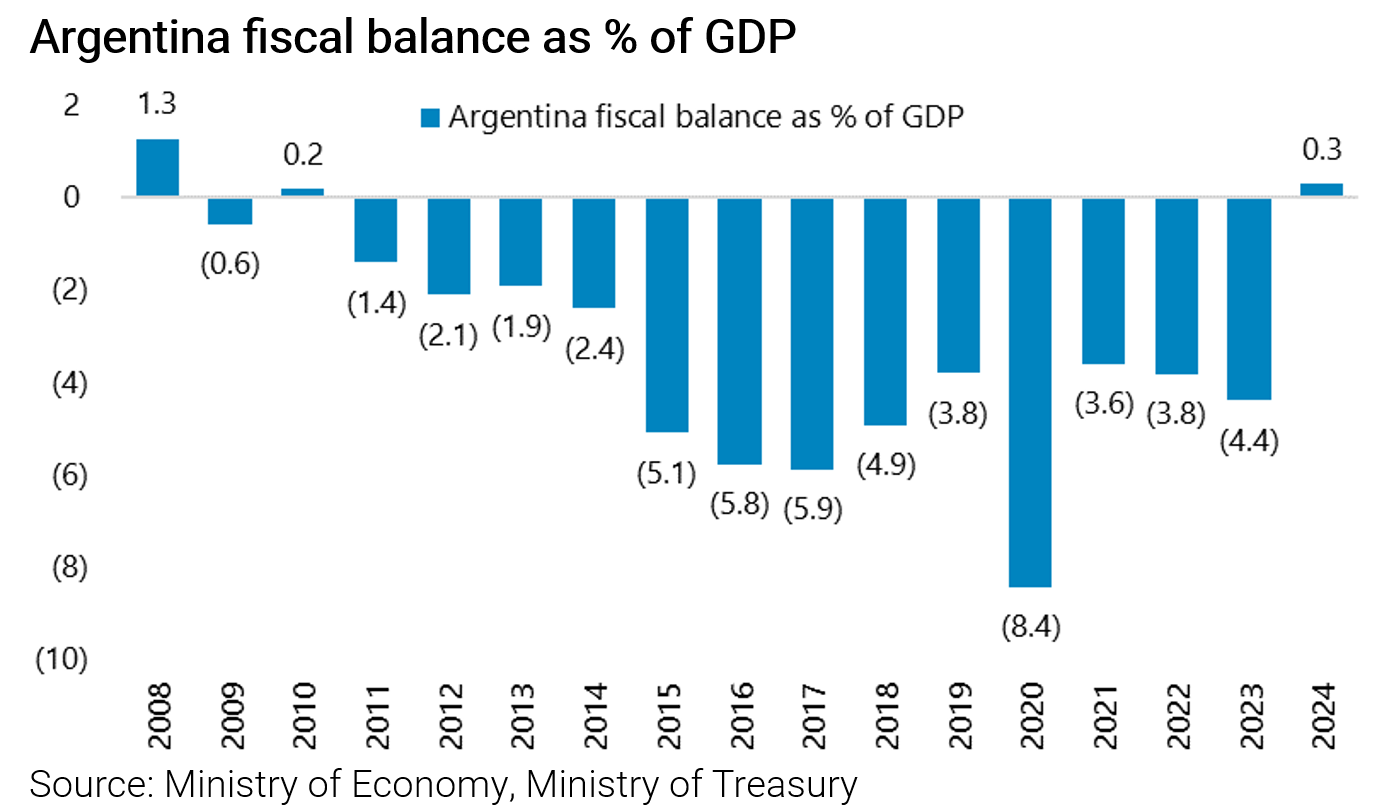

Based on the official numbers, Argentina saw its fiscal deficit contract by five percentage points last year.

To be precise, the fiscal balance improved from a deficit of 4.4% of GDP in 2023 to a surplus of 0.3% of GDP in 2024, the first fiscal surplus since 2010.

But if the US$63bn of central bank interest-bearing liabilities at early December 2023 is also taken into account, the fiscal contraction is probably more like ten percentage points of GDP, as the central bank has been cleansed of the bad habit of quasi-fiscal financing.

This fiscal adjustment is way more than what the IMF was proposing, which gives the Milei government a powerful story to tell in terms of its current negotiations with the IMF.

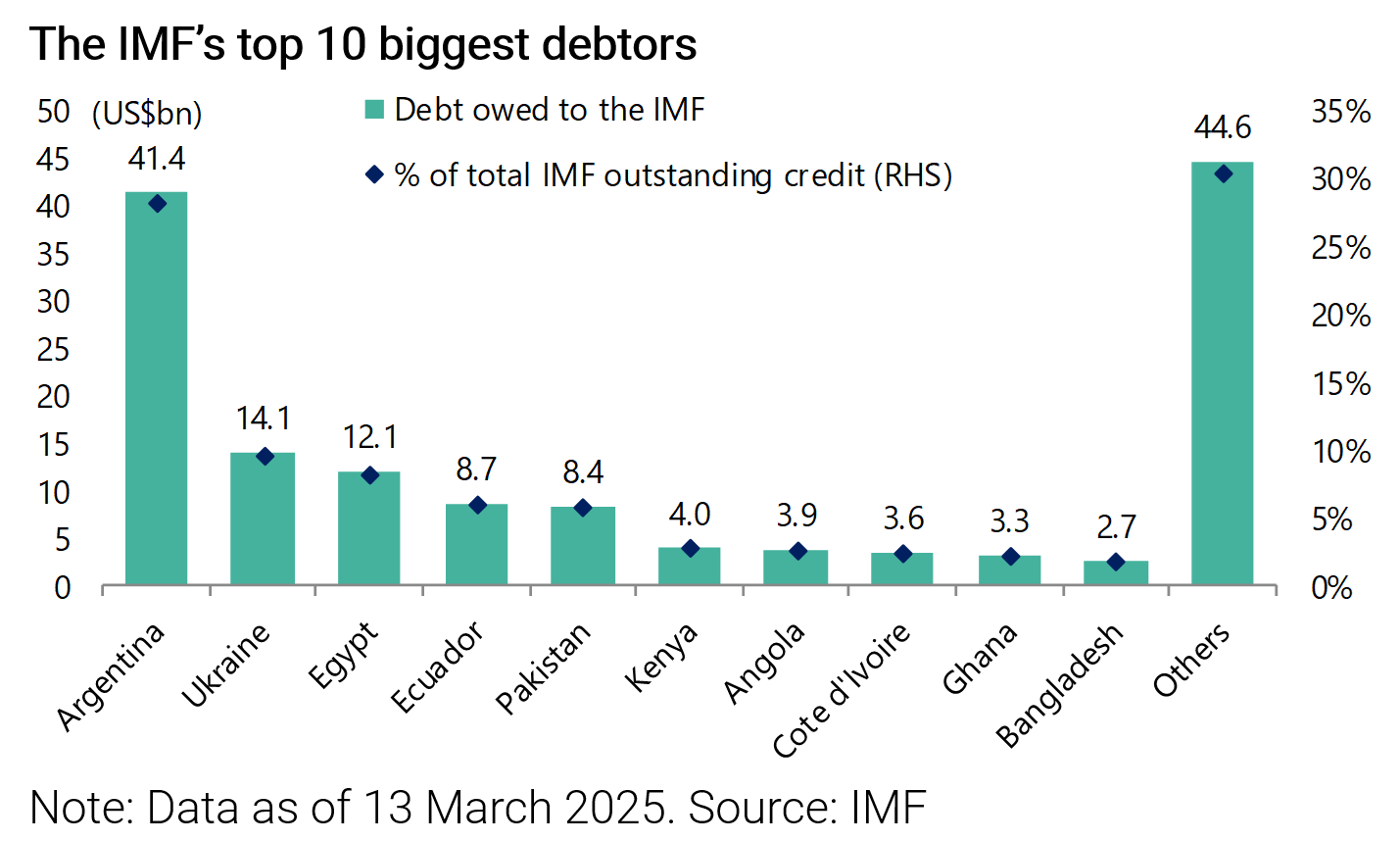

Argentina is the IMF’s biggest borrower with a total outstanding debt of US$41bn as of 13 March or 28% of total IMF credit outstanding.

How has this adjustment been achieved without a severe political backlash and also without an economic collapse?

One strength of Milei’s position politically is that he only promised economic pain to the electorate in his successful presidential campaign in 2023.

He therefore has the mandate for a policy which has ended the bad habit of financing the government by printing money, and the related bad habit of defaulting, which has essentially been the Argentine way since convertibility blew up in late 2001 after eight years of relatively healthy growth.

Real GDP growth averaged 5.9% between 1991 and 1998.

Milei has achieved the goal of fiscal equilibrium via such measures as abolishing subsidies, ending public works spending, and cutting all discretionary transfers to the provinces while pensions were not adjusted for inflation last year.

Still, there has been one specific exception where he allowed a welfare benefit to rise in real terms in 2024.

That was a child benefit.

He also generated huge goodwill by abolishing the system where third-party agents, known as piqueteros, decide to whom subsidies and benefits are paid.

Indeed, such agents had the right to determine if a benefit was paid to an individual.

Moreover, applicants had to turn up to an office every six months to get the relevant document rubber stamped and renewed.

The intermediaries also often took a cut of the benefit and, in many cases, demanded recipients take part in street demonstrations as another form of payment for services rendered.

This system, which developed in the post-convertibility era, has now been shut down.

This means ordinary people are now in some cases receiving more money direct than they used to, given the disappearance of what one contact described to this writer as the “managers of prosperity”.

This was clearly a very brave move by the 54-year-old Argentine president, given the vested interests he will have hurt via such a policy.

But it has won him huge popularity, especially apparently among the young.

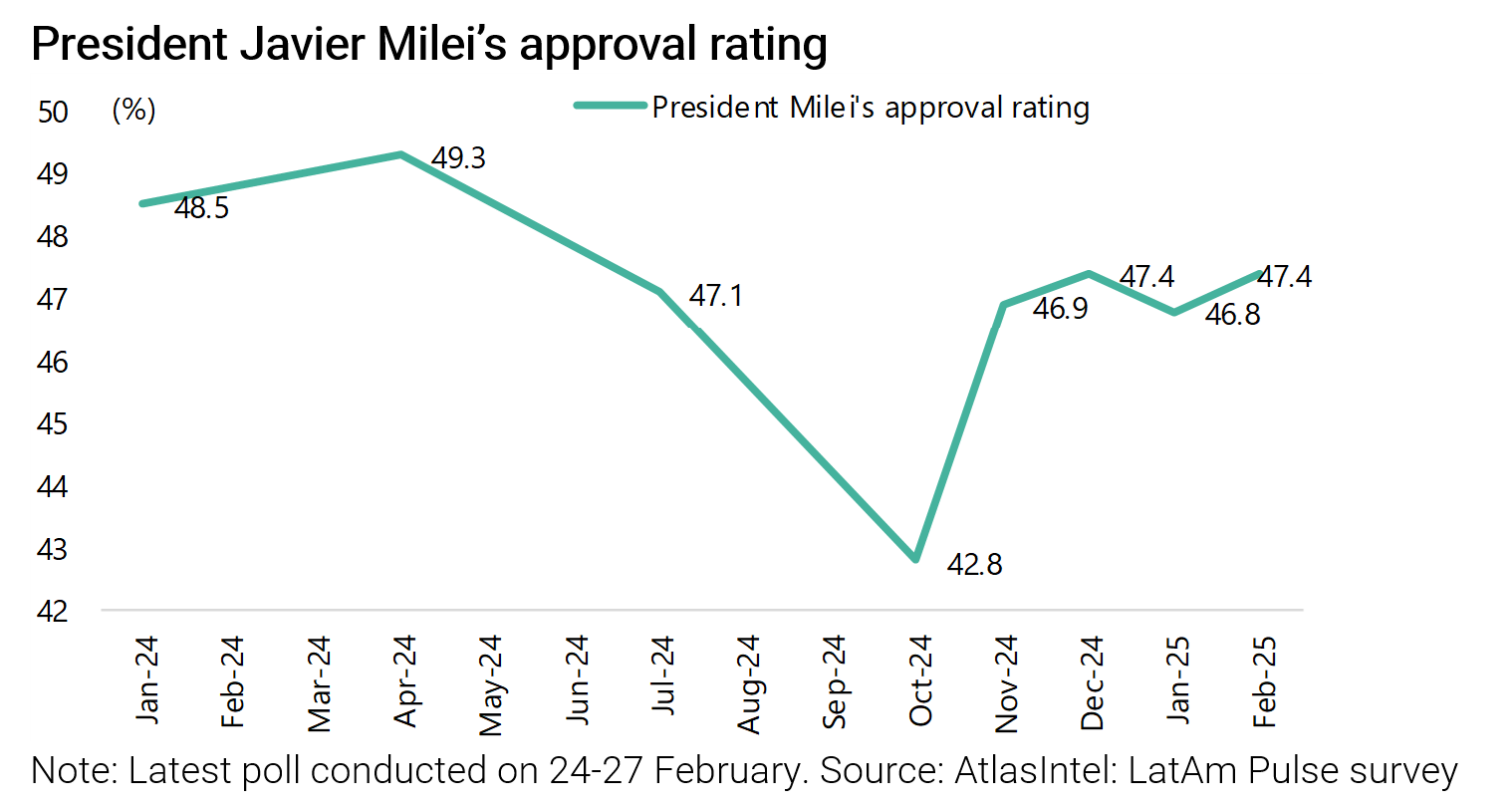

Milei’s approval rating is currently running at 47%, according to one pollster.

All this is why the base case is that Milei, or at least the political party he leads, will do well in the mid-term elections, which are due to be held in October.

The key point is that if his party can get one-third of the seats in either one of the legislative chambers, then the Congress cannot obstruct an executive order.

At present, such an electoral outcome looks eminently achievable.

The Chances of Argentina Opening Up to Foreign Investment

Still, in the near term, the focus of the market is on whether Argentina will conclude an IMF deal and whether this will lead to an opening, or at least a partial opening, of the capital account.

Clearly, opening the capital account is a politically risky move, most particularly shortly before an election, which is why if it is going to happen it will likely be by May at the latest.

On this point, Argentina’s government published a decree on 11 March backing a new IMF program, the most concrete step yet towards sealing a new deal.

Importantly, a decree only requires support from one chamber of Congress for approval, unlike as regards bill.

Still, in the absence of such new money, no such dramatic move is likely, given that the foreign reserve position is only an estimated negative US$4bn on a net basis after subtracting the central bank’s foreign currency liabilities.

This is because the central bank has been focused primarily on supporting the currency rather than reserve accumulation, given the desire to keep inflation on a downward trend heading into the election.

Gross foreign exchange reserves were US$27.96bn as of 12 March.

It is the case that Argentina has been repaying debt of late, in stark contrast to its track record as a serial defaulter.

The country made a US$4.34bn foreign debt repayment on 9 January, the largest debt repayment in three years.

Argentina has defaulted on its debt nine times since independence in 1816, including three times this century.

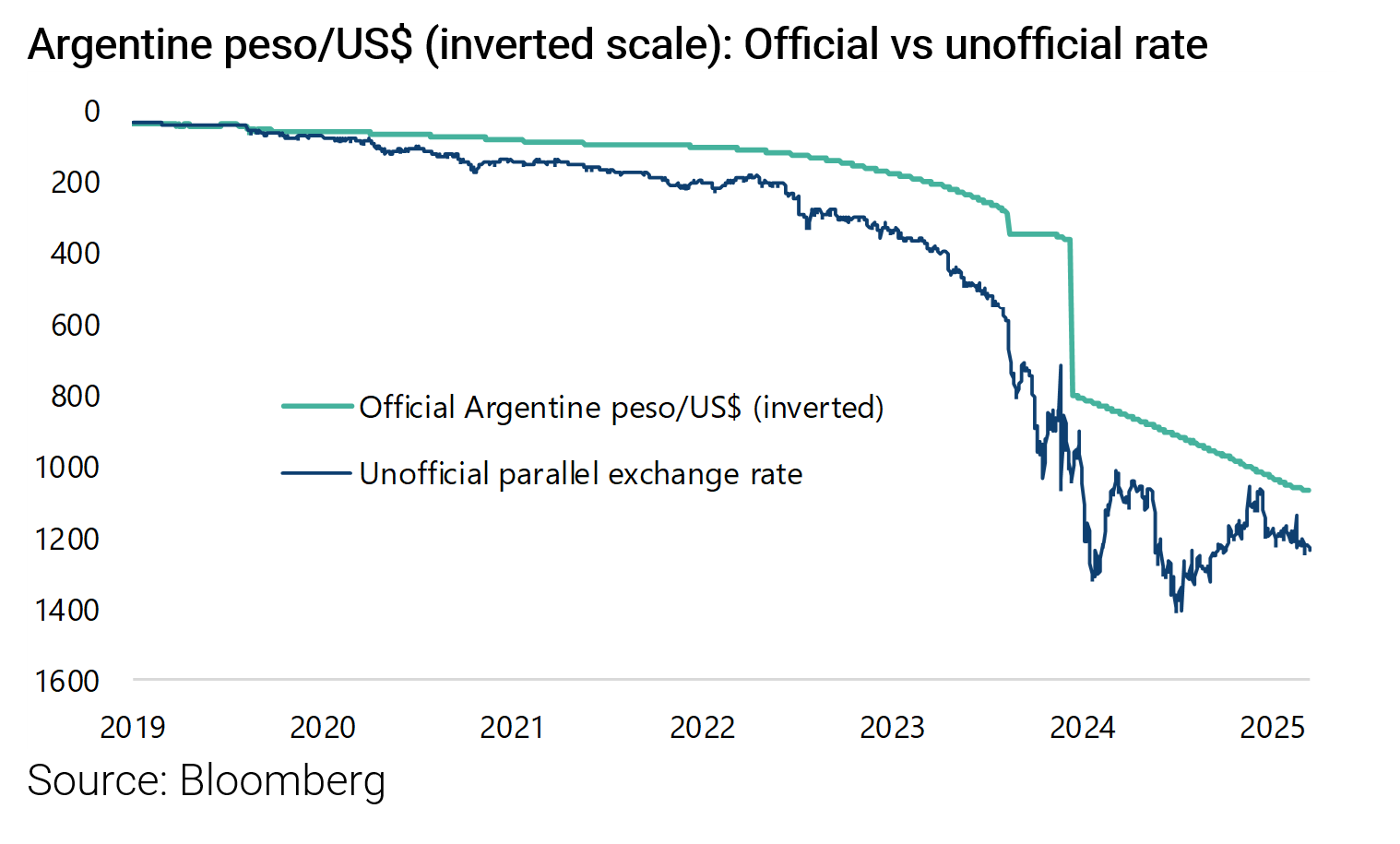

In this respect, it is the case that appreciation of the currency is a core part of the current adjustment process.

The currency has been depreciating by 2% a month against the US dollar since the start of 2024 following a 55% depreciation in December 2023, based on the official exchange rate.

This was reduced to only 1% monthly from 1 February.

As for the more important unofficial parallel exchange rate, it has appreciated by 14% since bottoming in early July 2024.

A strengthening currency also makes sense, given what has happened in fiscal policy, which is also the exact opposite of condition in Brazil of late, as discussed here recently (see Brazil Deep Dive: Is This Market Worth Your Time?, 5 March 2025).

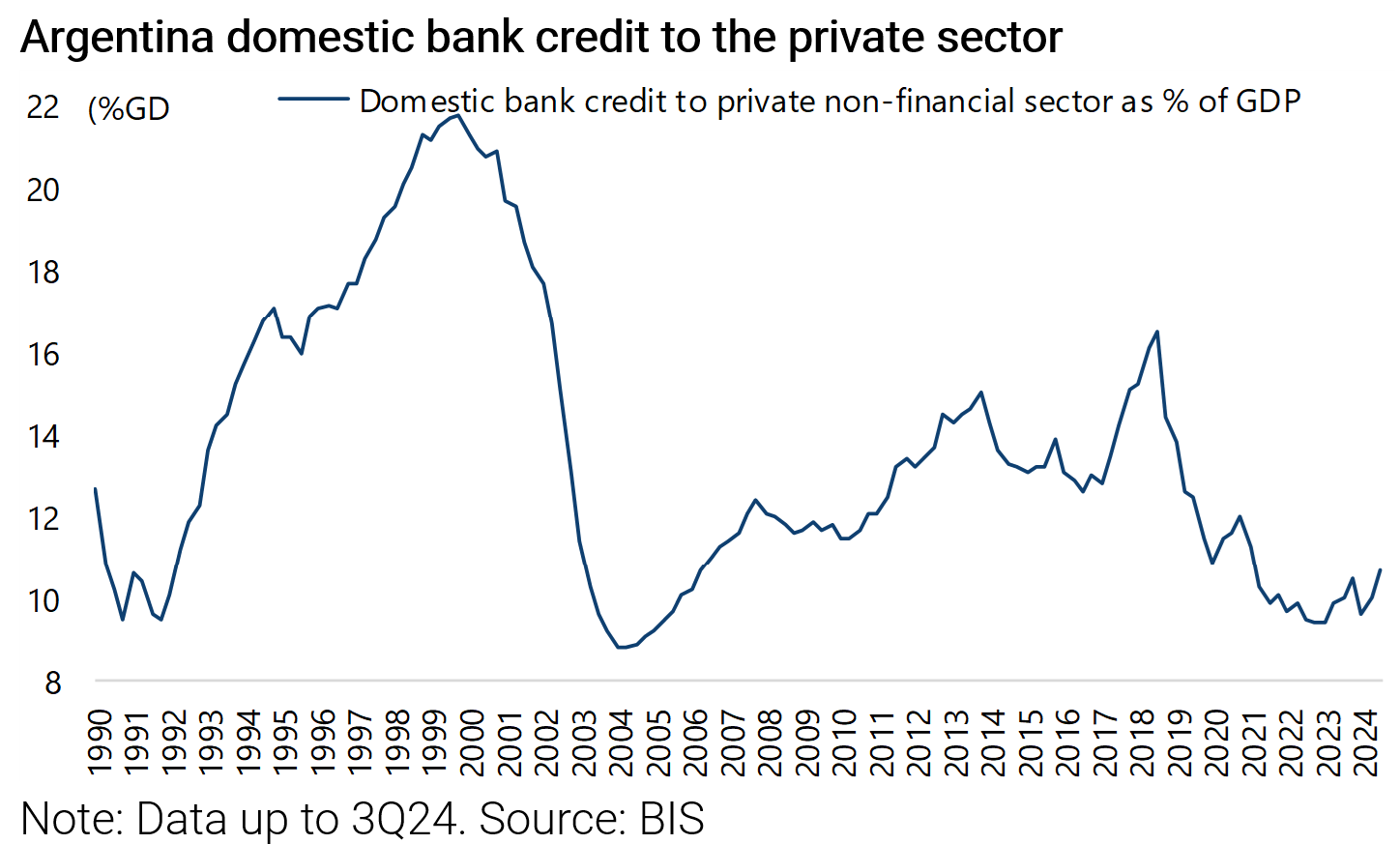

The Banking System is Lending Again

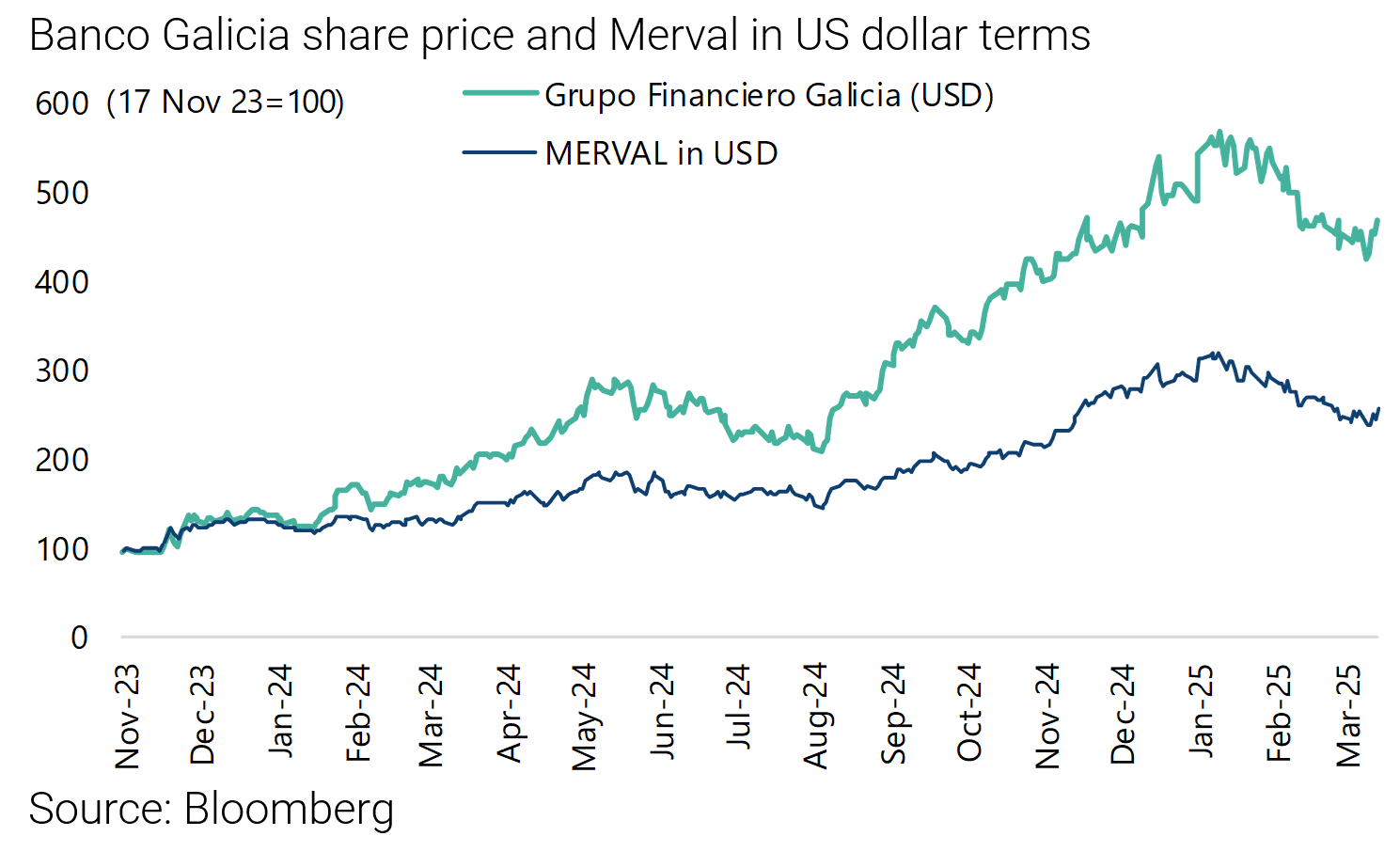

Meanwhile, the banking system has also begun to lend again after years of sitting on government bonds.

Total loans to the private sector were about 10% of GDP at the end of last year.

This writer heard a forecast of 40% real loan growth this year.

While mortgage lending has started to come back, with 20-year mortgages being offered at inflation plus 7%.

The expectation of an accelerating credit cycle is why banks have led the stock market rally since Milei’s victory in the presential election in November 2023.

Banco Galicia, the country’s leading private sector bank, is up by an impressive 370% in US dollar terms since then, compared with a 156% rise in the Merval index.

The potential upside is clear from the fact that loans to GDP were 22% of GDP at the end of 1999.

By the end of this year, they should be about 13%.

Milei’s Priority in 2025…

Meanwhile, if Milei has exceeded all expectations in Argentina, the task for this year is to consolidate those gains.

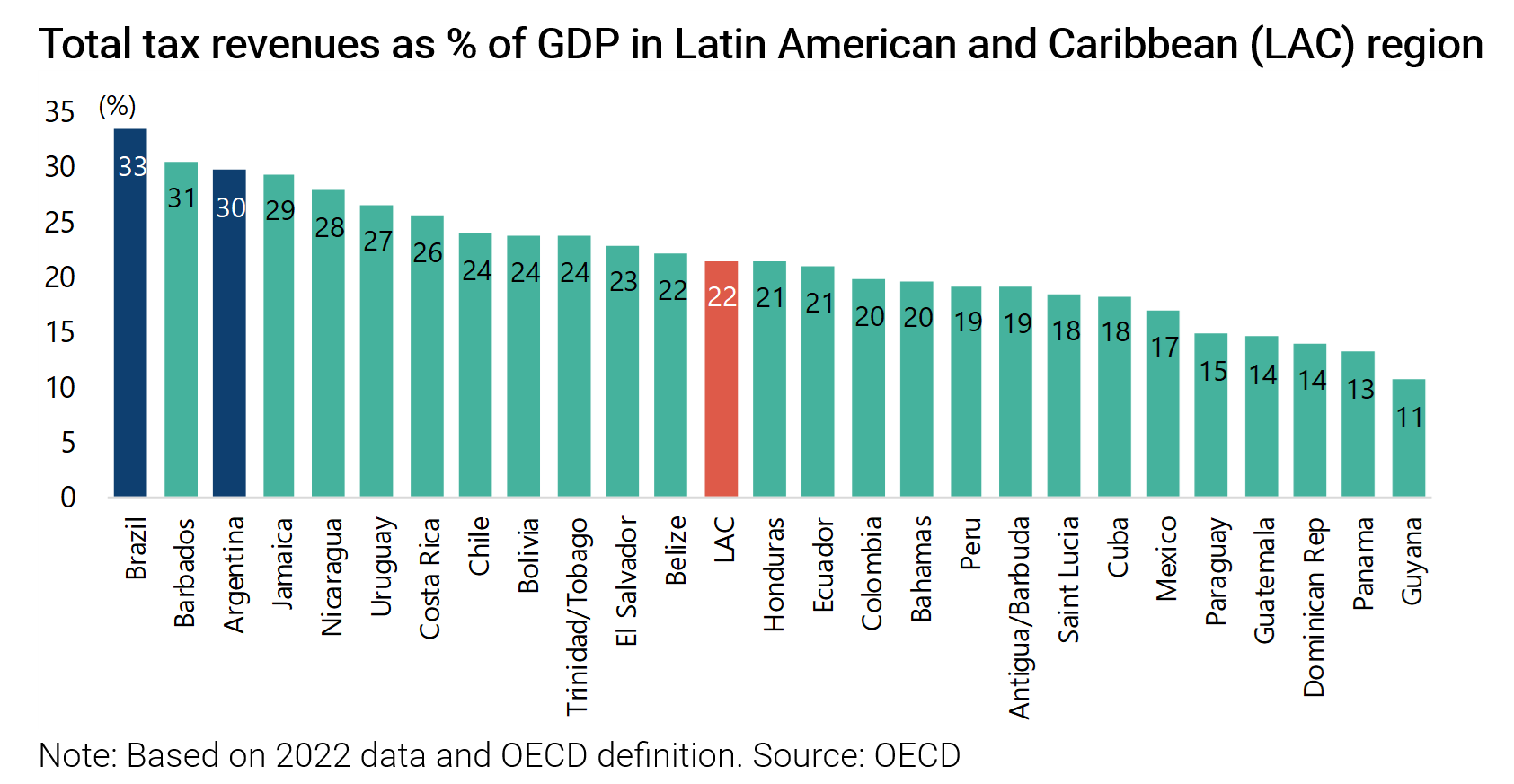

The first priority is, clearly, to maintain the fiscal discipline.

This means keeping the restraint on spending, as tax revenues are a too high 30% of GDP, according to OECD data.

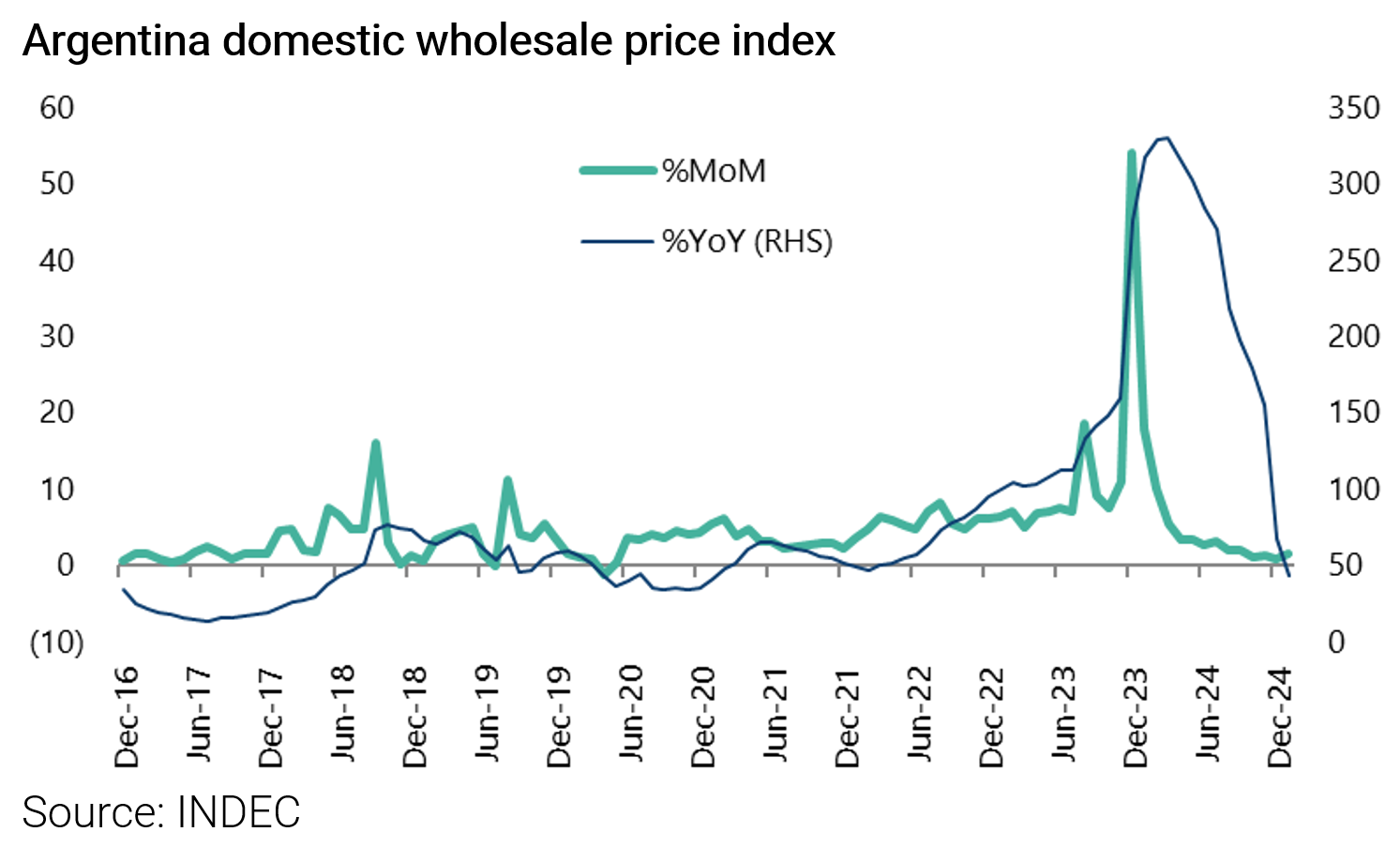

High inflation in recent years has reduced the real burden of these taxes by means of delayed payments.

But this is no longer the case with the sharp decline in inflation.

Indeed, domestic wholesale price inflation was only 0.8% MoM in December, the lowest monthly inflation rate since May 2020, and was 1.5% MoM in January.

About Author

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.