AMC Entertainment Holdings Inc. surged 4.34% after hours on Tuesday June 9th following their first quarter fiscal 2020 earnings release, thanks to strict liquidity measures and plans of reopening soon.

The company reported Non-GAAP EPS of -$2.22 which is higher than the street estimate of -$6.75, but lower by 126.5% year over year thanks to the pandemic.

Total revenue was $941.5M which is higher than the analyst estimate of $941.42M, but decreased by 21.6% year over year.

Net income decreased further by 1571.5% year over year to -$2,176.3M, mainly due to a significant impairment charge of $1,851.9M.

The Pandemic Effect

The movie industry has been hit hard by the pandemic, particularly theaters. Due to being highly levered, AMC faces a daunting challenge in paying back the interest to those loans especially since they were not EBITDA positive in the reported quarter.

However the company has taken drastic measures in preserving and raising liquidity following the signing of the Coronavirus Aid, Relief, and Economic Security Act (the “CARES Act”) on March 27, 2020.

Liquidity enhancement measures taken include the following but not limited to…

- Suspension of non-essential operating expenditures

- Reduction in corporate-level employment costs

- Agreement with landlord, vendors and other business partners in deferring rent for the time being

- Halting dividend payments and share repurchases for the duration of 2020

- Receiving $500 million from the issuance of 10.5% first-lien notes due 2025 on April 24, 2020 (will be discussed in detail further below)

Although this quarter performance was a disappointment due to the pandemic, the post market surge seems to suggest that investors are optimistic about the future of this company thanks to the above measures and their plans to reopen almost all of their theatres globally by July.

Can the company still Afford to Pay Interest Following the lockdown easement?

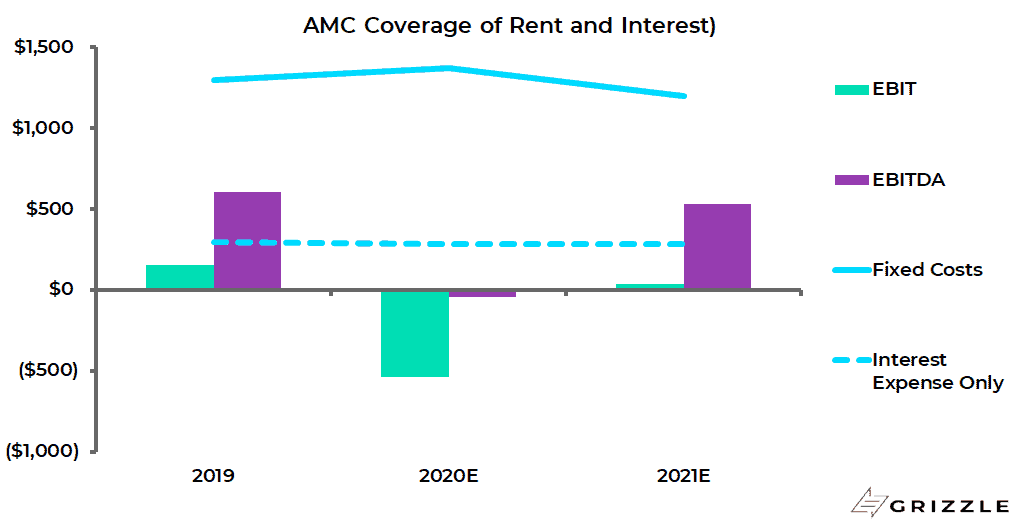

Positive EBITDA typically indicates whether a company can pay its interest payments.

The following addresses this concern if AMC is able to operate at 80% capacity this coming July based on their 2019 third-quarter revenue and expense adjustments.

* 2019 Q3 Revenue at 80% or 20% reduction in revenue.

** First costs related to Depreciation and Merger & Acquisitions were deducted from the 2019 Q3 operating expenses before reducing it by 20%. Then Q1 2020 depreciation costs were added back due to recency.

*** Total Interest Expense includes Q1 2020 total plus quarterly interest charge from their new debt issuance of $500 million 10.5% first lien notes due 2025.

**** Tax assumed constant.

a M&A activity is assumed to be non-existent since operations are limited in capacity.

b Depreciation would remain the same as the amount reported in the first quarter.

c Impairment related charges are also assumed to be nil after they announced a significant charge this quarter.

According to the EBITDA of $110.1 million calculated above, AMC could be able to afford its debt since its interest expense is $14.2 million lower.

However, if AMC fully reopens but cannot keep the theaters at least 80% full, the company is at risk of defaulting on its debt obligations.

Interest expense is already dangerously close to the EBIT generation of the business and when we include the cost of rent, the company looks to be structurally unprofitable.

Additionally prior to the $500 million cash raise, the company was due to deplete its cash reserve by the end of the second quarter according to our calculations. Thankfully this cash injection has saved the company from that scenario by giving it another 12 months of cash runway space.

However AMC is not alone, its peer Cinemark Holdings Inc. who faces similar challenges these days, also raised cash by issuing $250 million 8.75% senior secured notes on April as well. This helped Cinemark to extend its cash runway space by another 9 quarters to 24 quarters too.

Peer Valuation

In terms of its valuation, at first glance AMC’s shares are trading much lower than its peer Cinemark Holding Inc.:

This is largely due to the fact that investors favor Cinemark’s higher dividend payout than AMC. But current circumstances have also forced Cinemark to suspend their dividend payment as announced by the company in April.

Additionally one would think that according to this chart AMC has an opportunity to converge its PS multiple with Cinemark at least to a certain extent, but they should not forget that AMC is highly levered.

Blockbusters to the rescue!

There is no doubt that the pandemic has created new subscribers to streaming services such as Netflix and Disney+ who can watch a variety of shows and movies in the comfort of their own home and safe from the spread of the virus at least until a vaccine is found.

This could lead to lower than expected customers to theatres around the world once the lockdown eases.

However, theatres including AMC believe that the upcoming summer blockbuster releases such as the much anticipated Tenet, DC’s Wonder Woman 1984, and Marvel’s Black Widow will incentivize people under a limited capacity as mentioned before to buy tickets and experience the movie to its fullest extent.

If that is the case, then theatre operators like AMC believe that they will ultimately restore much of the lost ticket sales and prior pandemic growth in the coming quarters.

Final Thoughts

The pandemic has certainly put a dent in AMC Entertainment Holdings Inc. causing its revenue to tank and net losses to increase.

However, the company’s plans to reopen this coming July and the $500 million cash raise has boosted optimism in the company’s survivability and its ability to pay its debts.

The company expects that its lineup of summer blockbuster releases will encourage people to buy tickets starting from July but the threat of the virus spreading remains until a vaccine is found.

In the meantime if investors have doubts in the success of the company’s reopening plans or if the company delays reopening altogether, it would be wise to hold on to their capital until the release of the company’s third-quarter earnings ending in September to see how bad things truly are.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.