On the eve of Donald Trump’s inauguration, there has obviously been a lot of tariff-related noise from the President-elect.

Still this writer’s base case remains that this is primarily a negotiating tactic and that the Trump administration will end up not implementing anything like the 60% tariffs he has previously threatened China with.

Clearly, appointed Treasury Secretary Scott Bessent has indicated as much in his comments as regards Trump’s tariff agenda.

On this point, Bessent has called for gradual tariffs in his previous interviews and has described Trump’s threat on higher tariffs on Chinese imports as a “maximalist negotiating position” typical of a New York property developer.

With Trump in Power the US Dollar Has Likely Peaked

Aside from the use of tariffs as a negotiation weapon to achieve other policy aims, be it setting up production in America or stopping immigration from Canada and Mexico, there is also the issue that tariffs will be inflationary for ordinary Americans.

And it seems reasonably clear that the surge in inflation during the Biden administration was perhaps the major reason for the Republicans winning both the presidential and legislative elections.

Being in America of late has again reminded this writer just how expensive the place is in US dollar terms, let alone in foreign currency terms.

It is also the case that Trump has said he does not want a strong dollar, which is what he is likely to get if the full force of tariffs is implemented.

For such reason, the guess is that the US dollar is likely to peak with the Donald’s return to the White House; though this writer is for now still assuming that Elon Musk’s plan to cut US$2tn from federal spending will not actually happen, however commendable such an outcome would actually be.

For those who have not seen it, it is recommended to read the op-ed published in the Wall Street Journal by Elon Musk and Vivek Ramaswamy setting out the cost cutting agenda with a set deadline of 4 July 2026 (see Wall Street Journal article: “Elon Musk and Vivek Ramaswamy: The DOGE Plan to Reform Government”, 20 November 2024).

Clearly, if the US$2tn cost cuts are achieved, it would be highly deflationary and very dollar bullish.

Indeed it would also be very bullish for Treasury bonds, thereby turning the prevailing narrative here for the past three years on its head.

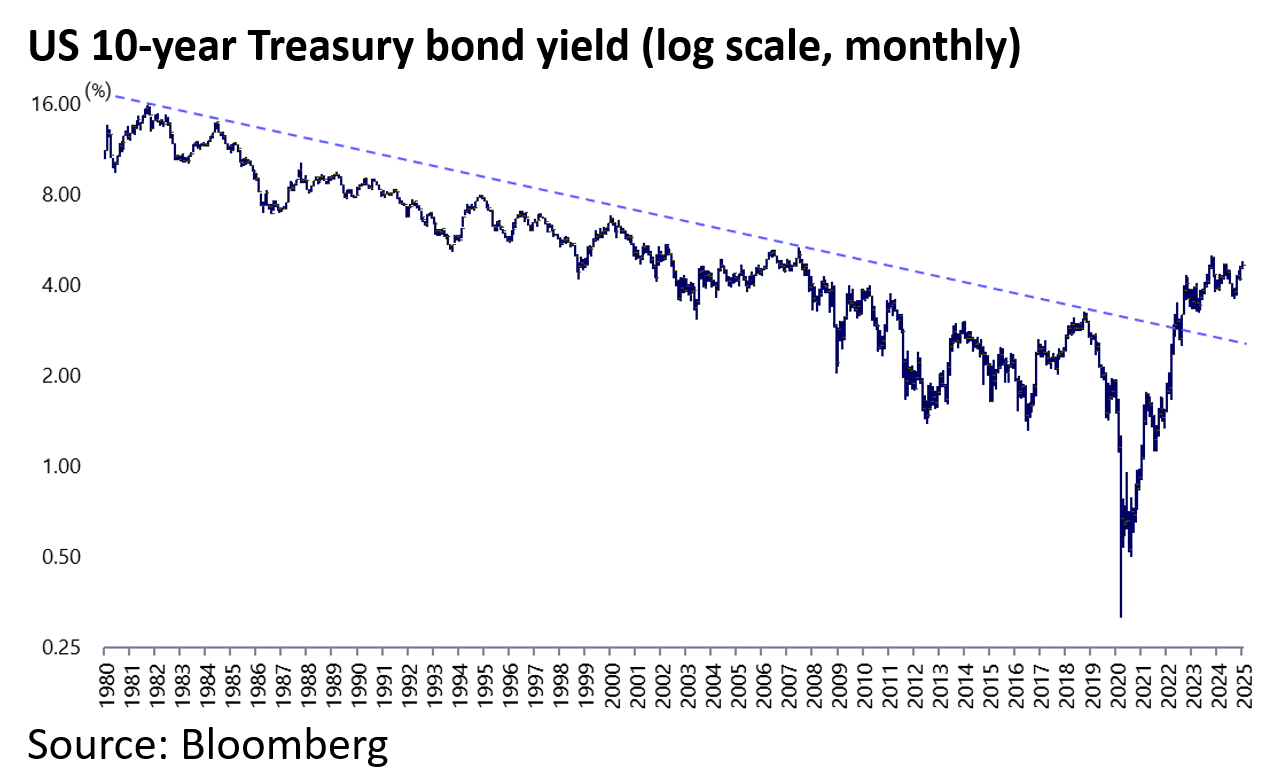

This writer has been arguing since March 2020, so far correctly, that Treasury bonds have entered a structural bear market.

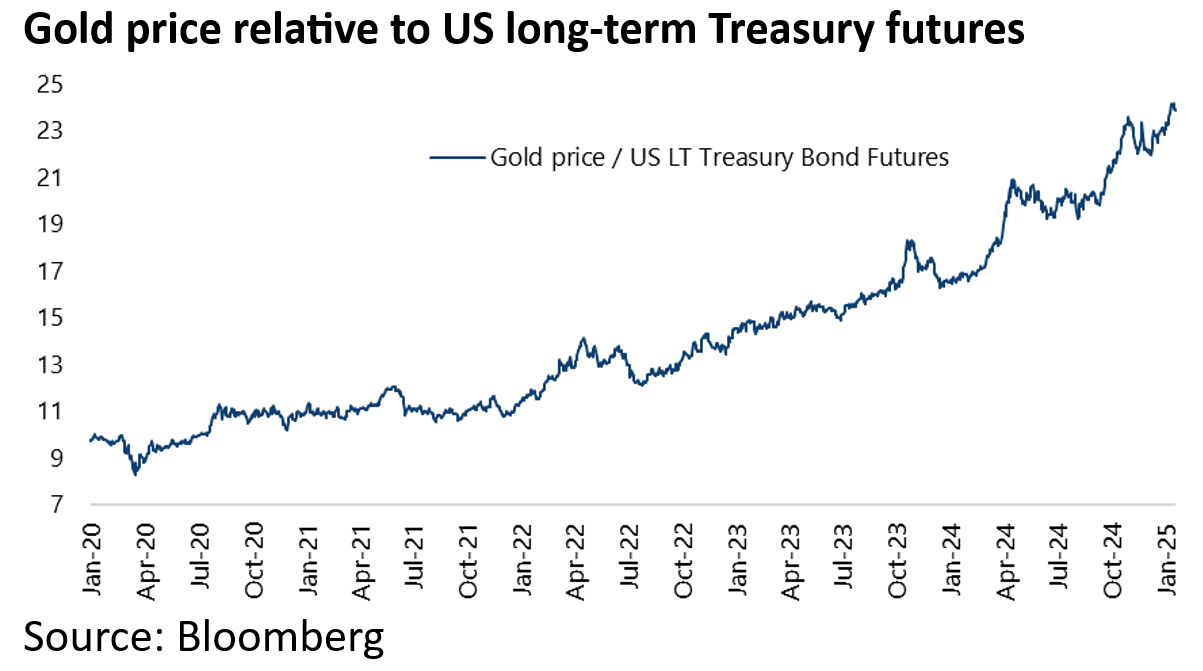

On that subject, the bear market in Treasury bonds against real money, namely gold, is shown in the chart below in what could be termed the currency debasement trade.

Meanwhile, it has to be wondered whether the US equity market also peaks, at least temporarily, ahead of Trump’s inauguration given the extent to which domestically orientated stocks have rallied on the deregulation theme.

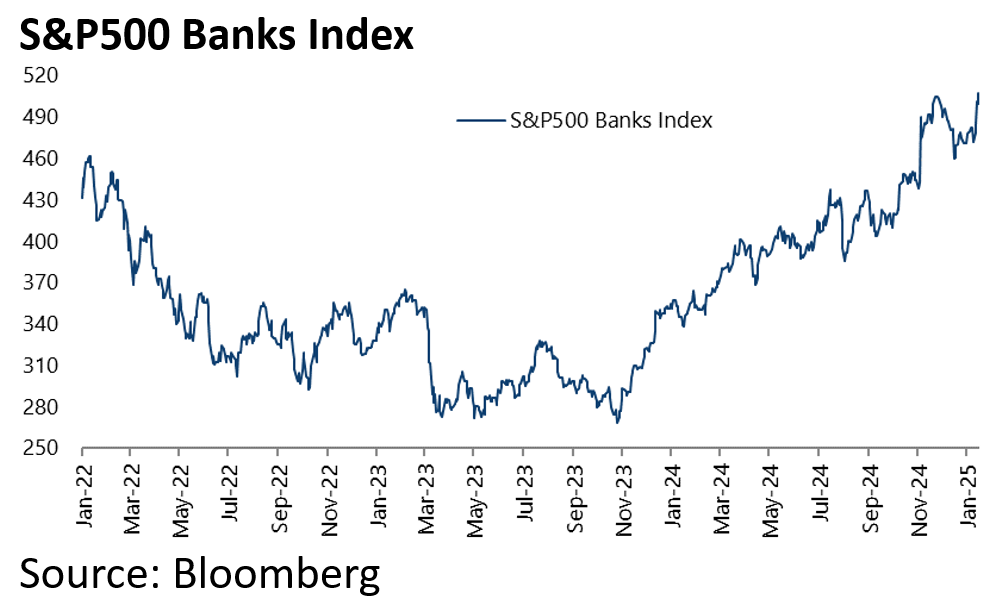

Bank stocks, for example, are up by 16% since the election on 5 November.

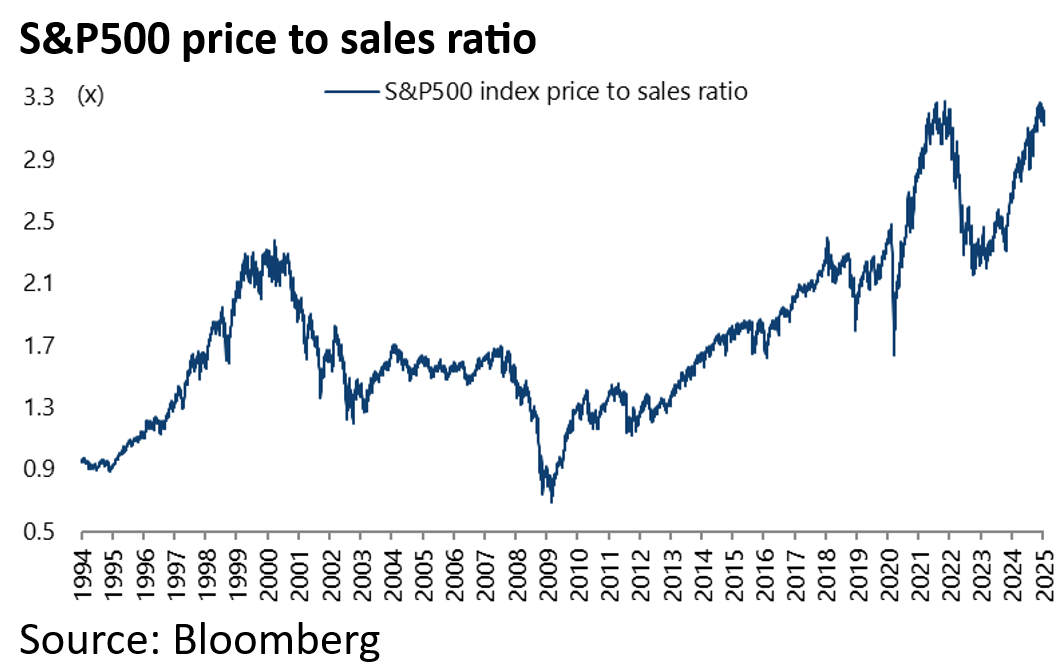

At a time when there is much talk about “American exceptionalism”, it is worth noting that the S&P 500 price to sales ratio is almost back at a record high.

The ratio rose to 3.26x on 6 December and is now 3.21x, compared with the previous peak of 3.27x in November 2021.

Meanwhile, America is now 66.9% of the MSCI All Country World Index which is near the all-time high of 67.2% reached in late December.

Valuations are Getting Extreme but that Doesn’t mean US Stocks Can’t Go Higher

Financial markets can get very extreme at inflection points and it has to be wondered whether such a point is approaching.

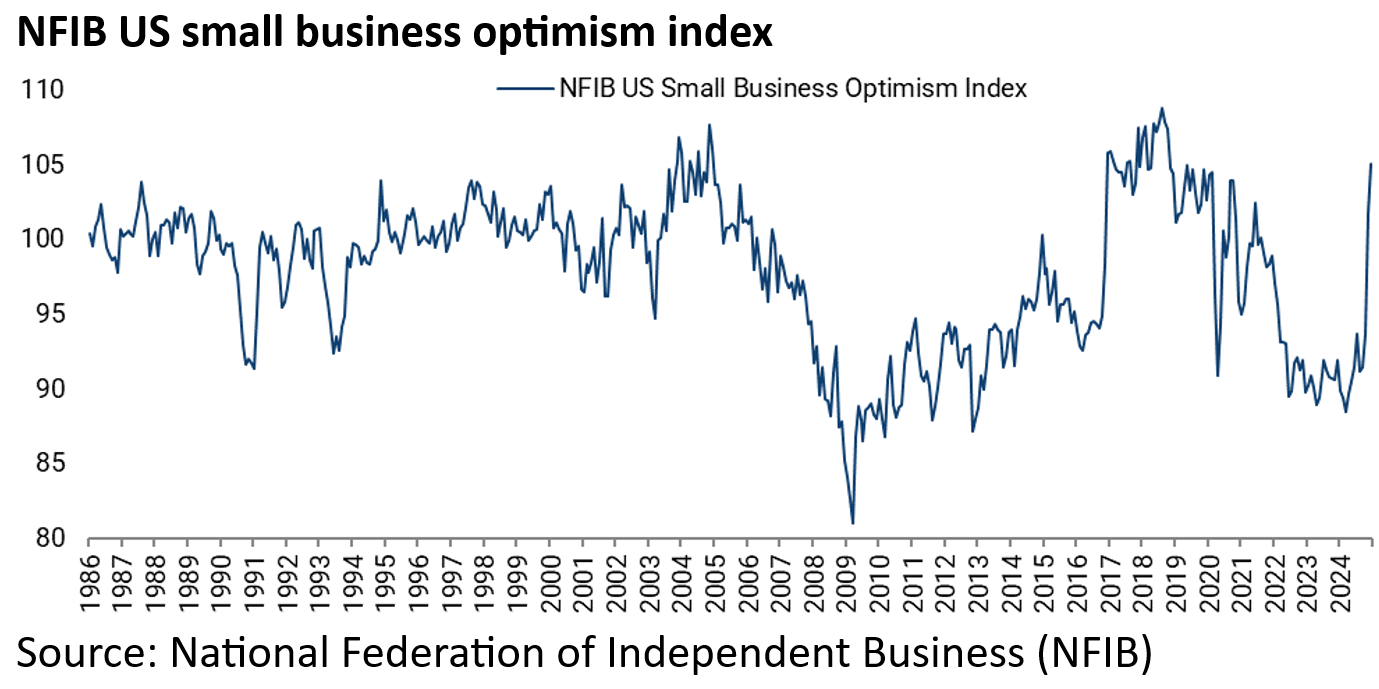

But for now it is crystal clear that there is almost zero interest in America in investing in equities outside America, be it the investor institutional or retail, while the Donald’s re-election has for now undoubtedly stimulated the animal spirits, as reflected in the spike in the small business confidence index.

The National Federation of Independent Business (NFIB) small business optimism index increased by eight points from 93.7 in October to 101.7 in November, the biggest monthly rise since the monthly NFIB survey began in 1986, and was up a further 3.4 points to 105.1 in December, the highest level since October 2018.

It also should be noted that the same happened in late 2016 when Trump was first elected.

The index increased by 3.5 points from 94.9 in October 2016 to 98.4 in November and by a further 7.4 points to 105.8 in December.

The interest of American investors in investing outside the US is now primarily confined to those professional fund managers with the specific job of managing dedicated international mandates.

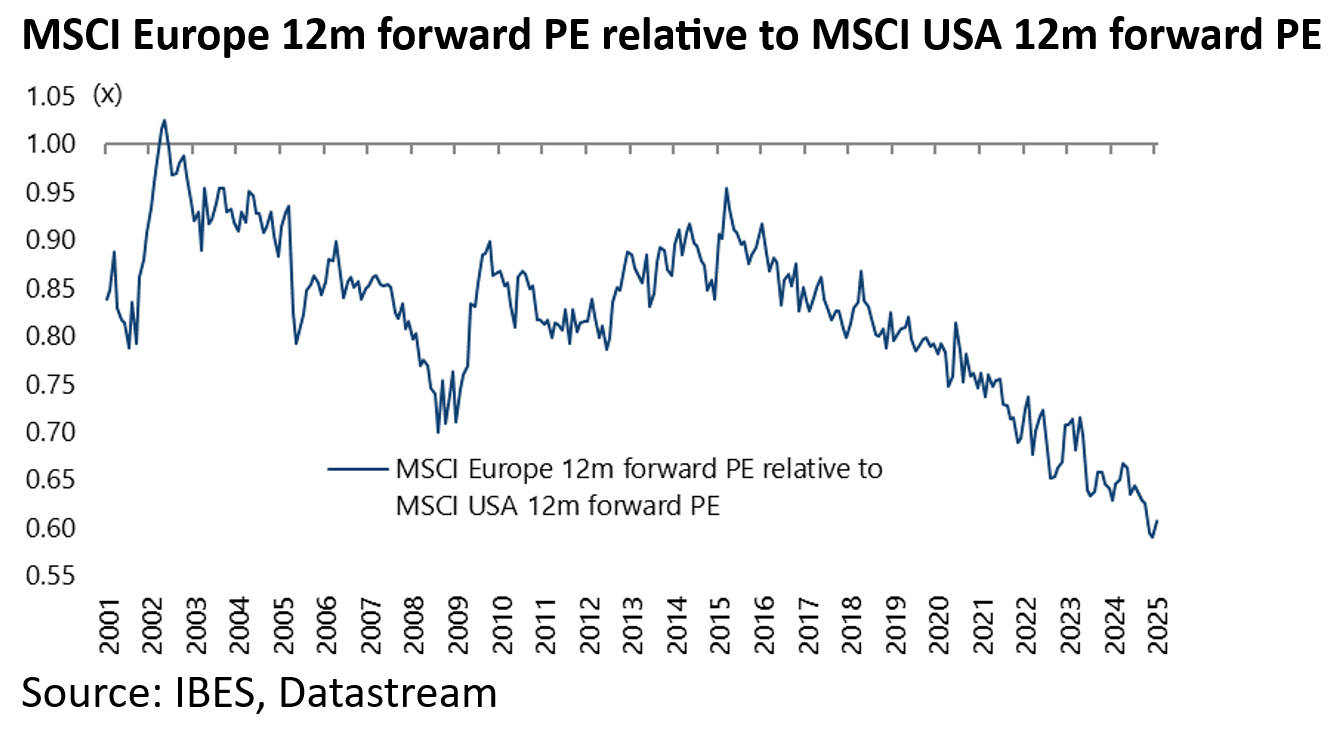

This is not just reflected in the lack of interest in emerging markets but also in Europe, which is increasingly regarded in terms of its “value added” as the place to take a holiday and party, a trend also encouraged by a strong US dollar.

Indeed Europe is now trading at a near record low valuation relative to the US market.

The MSCI Europe now trades on 13.5x 12-month forward earnings, or a 39% discount to the MSCI USA 12-month forward PE of 22.2x, compared with a record 41% discount in December.

Europe Outperformance is Still Possible This Year, Though it May be Short Lived

That said, this writer still believes there is the potential at least for a cyclical trade in Europe this year based on a new presumed CDU-led German government abandoning, or at least revising, the so-called “debt brake”, as discussed here previously (see Will February 23rd Mark the Day Europe Becomes Investable?, 8 January 2025).

On that point, CDU leader Friedrich Merz has stated publicly that a revision of the debt brake could now be considered if the extra borrowing was deployed to boost investment as opposed to increase spending on consumption or welfare policies.

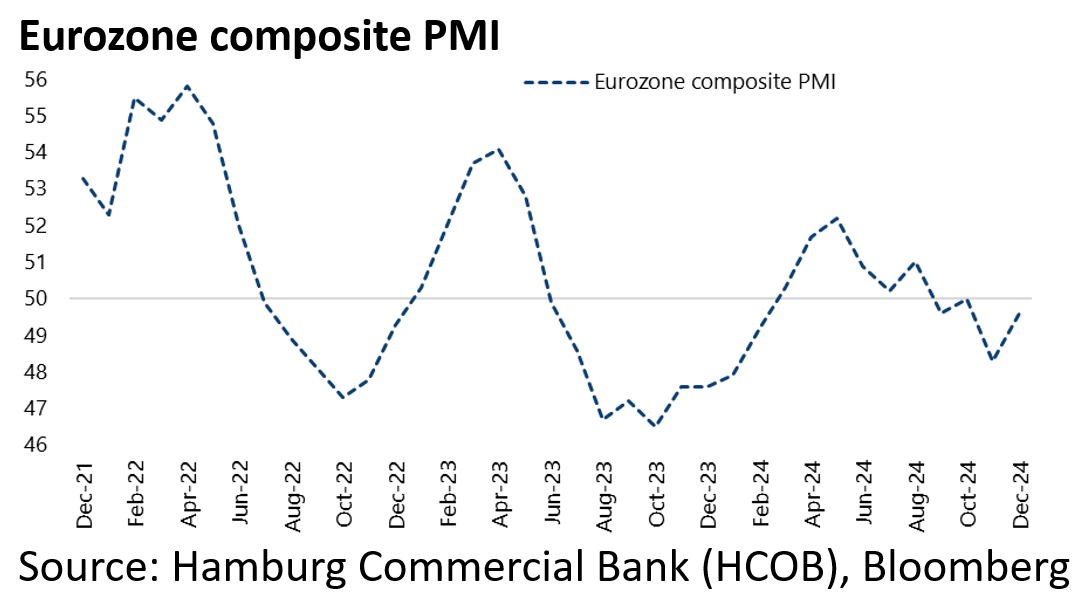

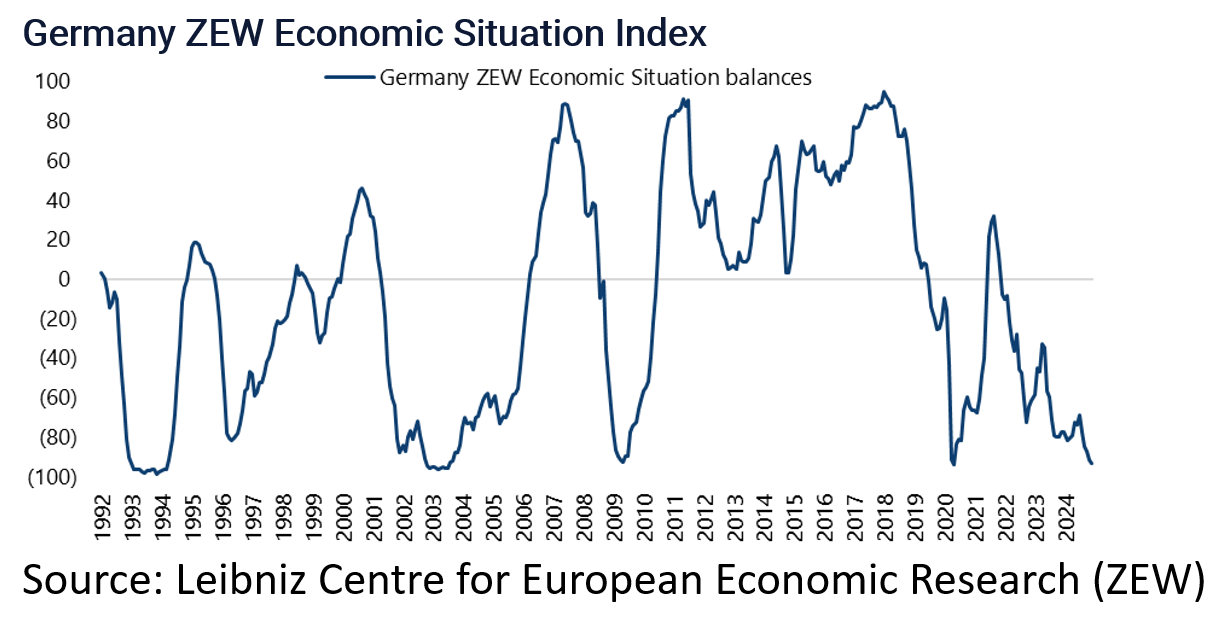

The latest Eurozone data has further confirmed the deteriorating macro trend, most particularly in Germany.

The Eurozone Composite PMI declined from 50 in October to a 10-month low of 48.3 in November.

As for Germany, the ZEW Economic Situation Index declined from -86.9 in October to -93.1 in December, the lowest level since May 2020, while German real GDP declined by 0.3% YoY on a calendar adjusted basis in 3Q24.

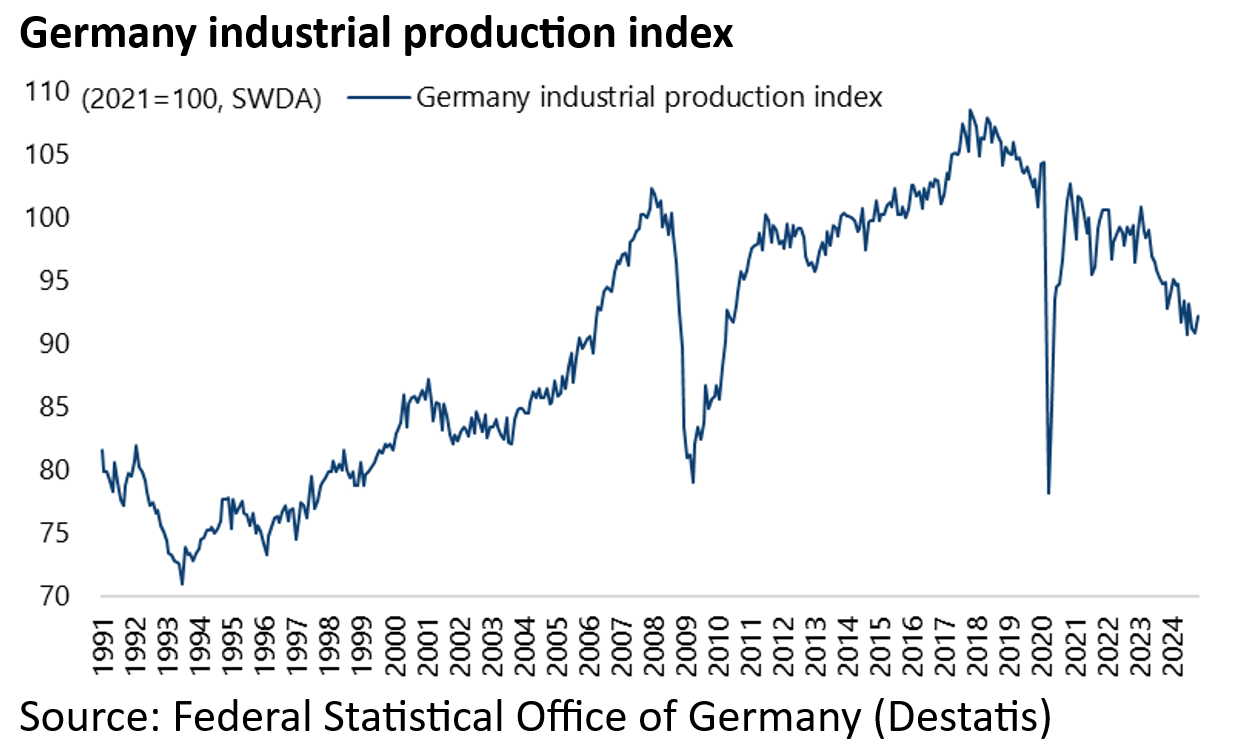

The German industrial production index has about declined by 15% since peaking in November 2017 to 92.2 in November 2024, though up from 90.7 in July, which was the lowest level since May 2020.

The above is why money markets are currently expecting the ECB to be cutting rates more this year than the Fed.

Money markets are now discounting 100bp of rate cuts by the ECB in 2025, compared with only an anticipated 38bp of rate cuts by the Fed.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.