Gold’s Resilience Despite Weak Physical Markets in India & China

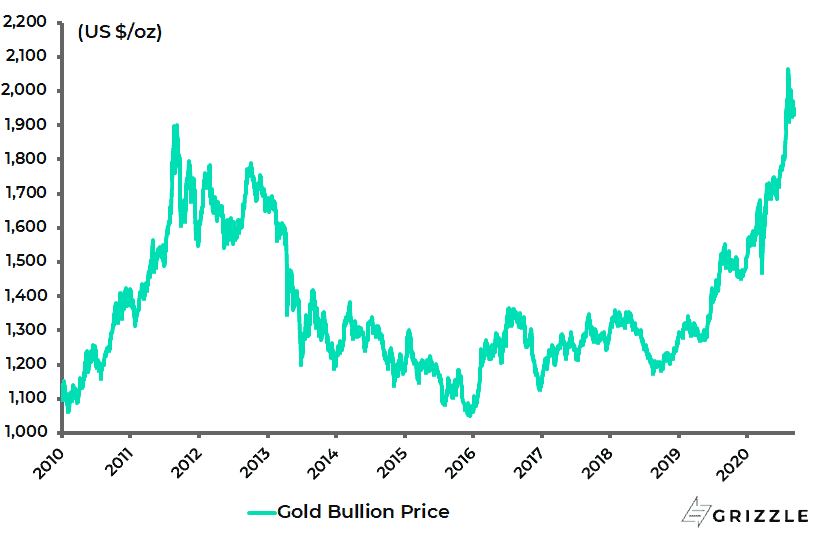

Gold continues to behave in a resilient fashion having been in consolidation mode since it made a new all-time high in US dollar terms of US$2,075/oz on 7 August.

Gold Bullion Price

This resilience is despite the weakness in demand this year for physical gold in India and China, two traditional buyers of the yellow metal.

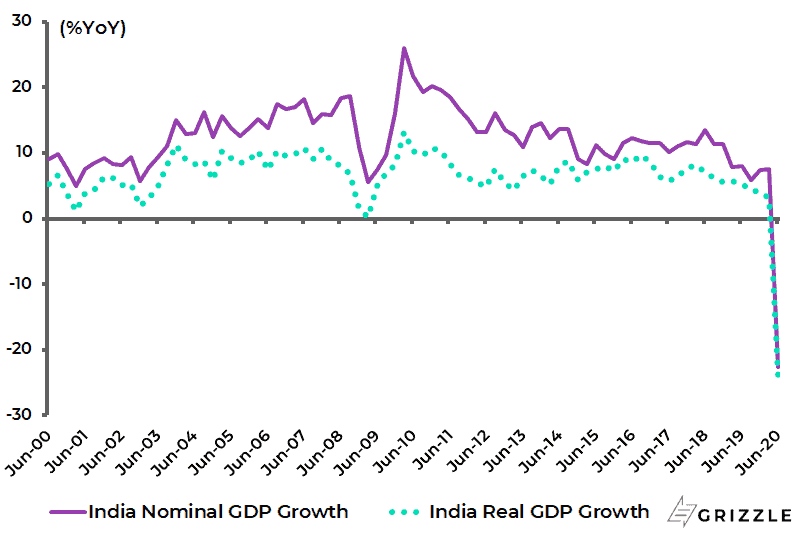

Indian demand has collapsed because of the collapse in the economy triggered by an aggressive lockdown and a surge in COVID cases.

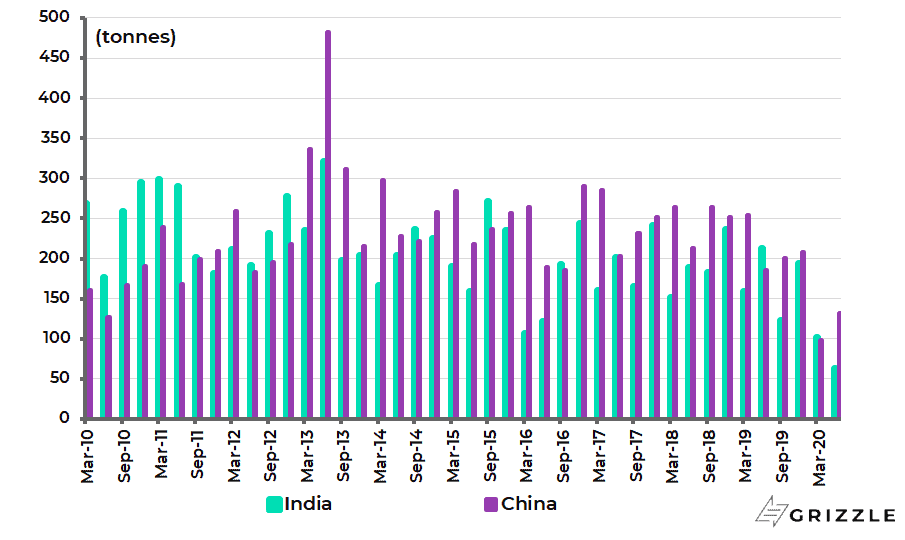

Consumer gold demand in India declined by 70% YoY to 64 tonnes in 2Q20 and was down 55% YoY to 166 tonnes in 1H20.

India and China Consumer Gold Demand

India’s real GDP imploded by 23.9% YoY in 2Q20.

India Real and Nominal GDP Growth

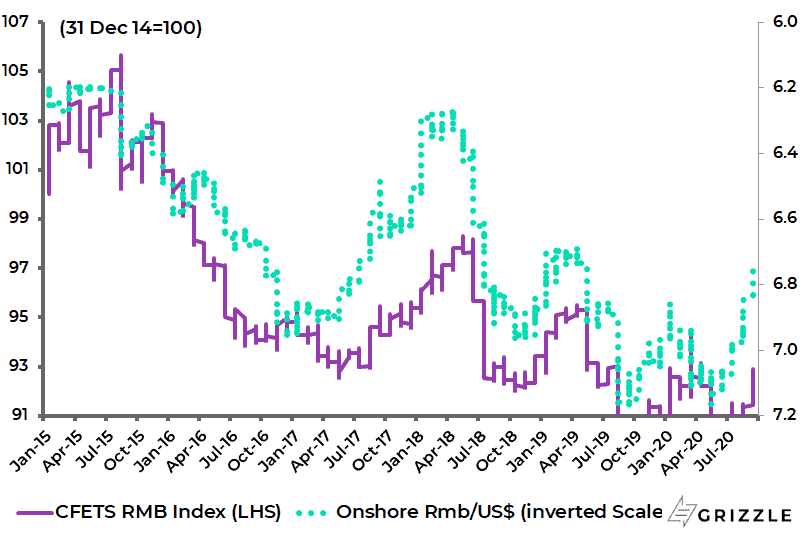

As for China, the demand for gold is less for the simple reason that the renminbi has not been under depreciation pressure.

China consumer gold demand declined by 29% YoY to 132 tonnes in 2Q20 and was down 48% YoY to 230 tonnes in 1H20.

The renminbi has appreciated by 2.9% against the US dollar so far in 2020 while the trade-weighted renminbi index is up 3% over the same period.

China Trade-weight Renminbi Index and Rmb/US$ (inverted scale)

Gold Target Price: $5,500

Meanwhile, with gold having made of late a new all-time high in US dollar terms, it is an appropriate time to review this writer’s long-term price target, which had been US$4,200/oz.

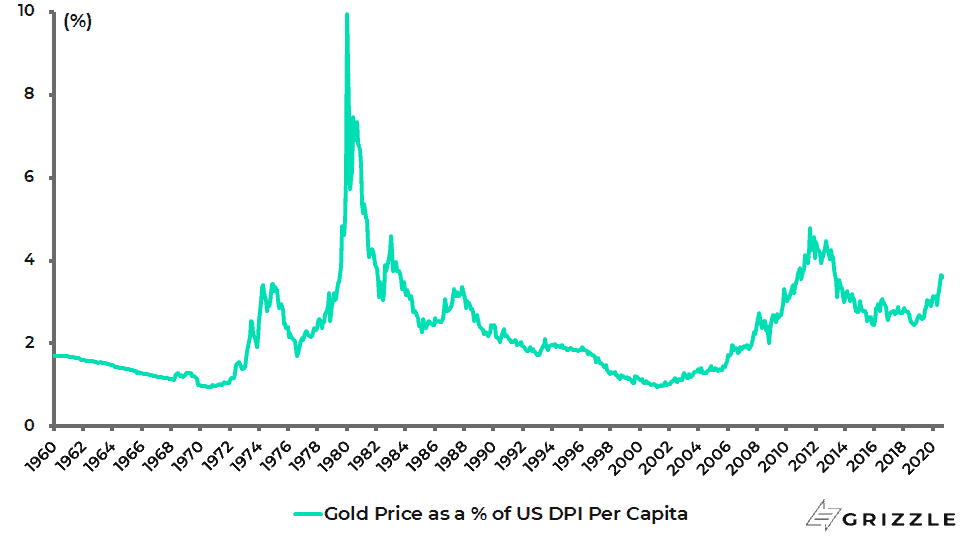

This was based on adjusting the gold price for US disposable income per capita, based on the gold price of US$850 at the peak of the last secular bull market in gold in January 1980.

The gold price was then equivalent to 9.9% of US disposable income per capita, which was US$8,547.

The gold price is now US$1,951 or 3.6% of US disposable income per capita of US$54,154.

To reach 9.9% of US disposable income per capita means gold should rise to US$5,386.

Gold Price as % of US Nominal Personal Disposable Income Per Capita

This means that a price of US$5,500 is now a conservative price target for gold at the peak of the current secular bull market.

On this point, it should be made clear that the bull market in bullion is viewed as having commenced in 2001 when gold was US$254/oz.

The correction of gold from the 2011 peak of US$1,921 to the late 2015 bottom of US$1,046 continues to be viewed here as a cyclical bear market in the context of an ongoing secular bull market.

The first stage of this bull market, which peaked in 2011, was driven primarily by Chinese and Indian buying. But the latest bull run has been primarily driven by Western financial investors buying gold as a hedge against US dollar debasement.

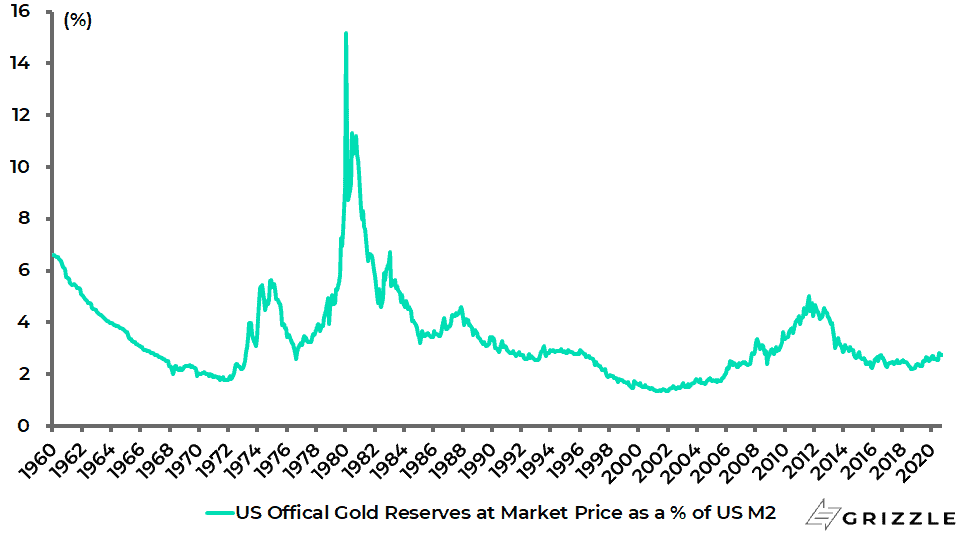

If the above is one longstanding methodology employed here for setting a price target for gold, it is worth looking at another way of valuing gold for comparative purposes. That is to compare America’s official gold reserves with US M2.

Back in January 1980 at the peak of the last secular gold bull market, US M2 was only US$1.48tn while the official US gold reserves were 264.6m oz.

So, at a peak price of US$850/oz, the gold reserves were valued at US$225bn, or equivalent to 15.2% of M2.

What is the state of play now?

The US official gold reserves are now 261.5m oz or US$510bn at the current market price, equivalent to 2.7% of current US M2 of US$18.58tn.

For the US official gold reserves/M2 ratio to rise to 15.2%, the gold price would have to rise to US$10,776/oz.

US Official Gold Reserves at Market Price as % of US M2

The above highlights the potential blue sky for gold unless the Federal Reserve does a dramatic U-turn and suddenly starts targeting higher real rates in the US.

Trumps Hardline on China, Positive for Gold

Remember that the key driver of the value of gold in US dollar terms is the trend in real interest rates. Another one is rising international tensions.

On that point, there have continued to be more developments on the feared US-China “Cold War” as Donald Trump has decided he needs to be ‘’anti-China’’ in the presidential election campaign.

The most dramatic move of late was the latest initiative by the US Commerce Department effectively to kill off China’s Huawei.

The Commerce Department announced in mid-August a move to restrict further Huawei’s access to items produced domestically and abroad from US technology and software, including foreign-made chips, and added another 38 Huawei affiliates to the so-called “Entity List”.

The aim, to quote US Secretary of Commerce Wilbur Ross speaking on Fox TV at the time, is to stop a “bad actor” (i.e. Huawei) buying US software and process equipment through “evasive measures” (i.e. via third parties).

The latest action against Huawei suggests that the China hawks in Washington do not want any major Chinese technology company to be successful globally.

While there may be a national security issue as regards Huawei’s 5G network equipment, it is hard to see what the big deal is about Huawei making smartphones.

Another move has been an executive order from the White House on 6 August stopping Americans using Tencent’s WeChat, an order that was implemented as of Sunday (20 September).

The key issue is whether this executive order is interpreted narrowly or broadly by the Commerce Department. It looks, for now, that it will only be narrowly interpreted which will mean that the main effect will be to stop the China diaspora in America from using WeChat. This is relevant because American companies doing business in China use WeChat, for example, to interact with their customers.

Meanwhile, a warning was sounded at a Beijing think-tank forum last month that China should prepare for possible US sanctions against Chinese banks or even possible seizure of overseas Chinese assets (see South China Morning Post article: “US sanctions: economist Yu Yongding flags risk of Chinese bank assets being seized overseas”, 12 August 2020).

At its most extreme, it was warned, China could even be cut off from the US dollar system by stopping access to Chips and Swift, just as such measures have hit Iran and been threatened in the case of Russia.

This is certainly quite possible in the context of Washington’s proven willingness to weaponize the US dollar.

Still, such dramatic actions seem most unlikely in the short term.

The enforcement measures against China have so far been primarily the responsibility of the Commerce Department, be it ZTE, Huawei and now Tencent, whereas enforcement of financial sanctions would be carried out by the Treasury.

And Treasury Secretary Steven Mnuchin seems to be the best friend China has got right now in the Trump administration.

Still, if there is an issue that could trigger such sanctions, assuming Donald Trump was tempted to make such a dramatic move ahead of the election for maximum political impact, this writer can certainly think of one.

That is, China buying Iranian oil in defiance of US sanctions, and its increasingly close relationship with Iran.

In that respect, there was an interesting article in the New York Times recently reporting that China is close to forming a long-term strategic partnership with Iran whereby China would receive discounted oil from Iran for the next 25 years in return for US$400bn of Chinese investment into the Iran economy with a focus on transport-related infrastructure (see New York Times: “Defying US, China and Iran Near Trade and Military Deal”, 12 July 2020).

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.