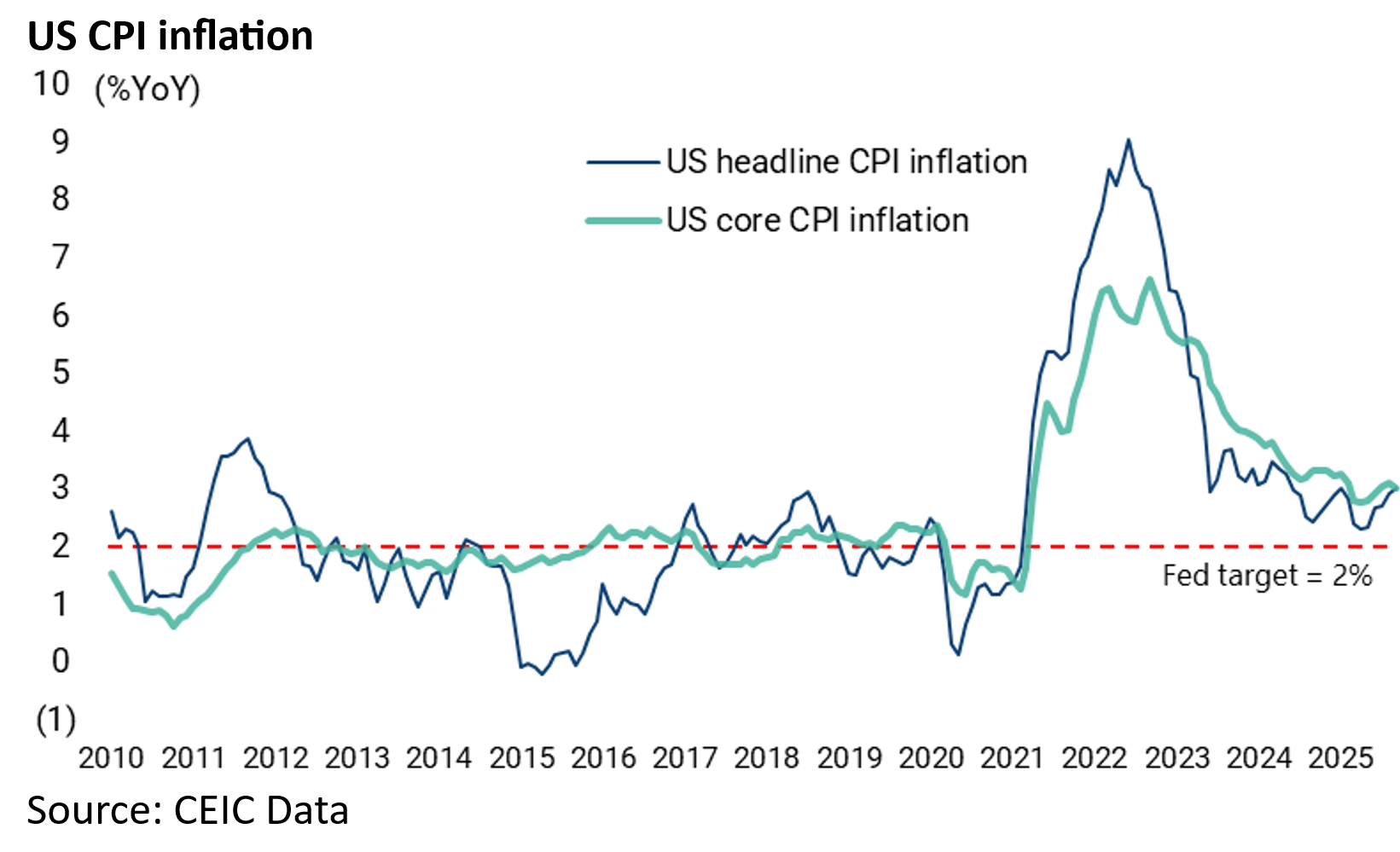

The path is set for another Fed rate cut at this week’s meeting on Wednesday following the latest inflation data even though reported inflation is still well above the 2% YoY target.

Headline CPI rose by 3.0% YoY in September compared with consensus expectations of 3.1% YoY, while core CPI inflation slowed from 3.1% YoY in August to 3.0% YoY in September.

Meanwhile, money markets are now discounting 50bp of rate cuts by the end of this year, up from 39bp in late September.

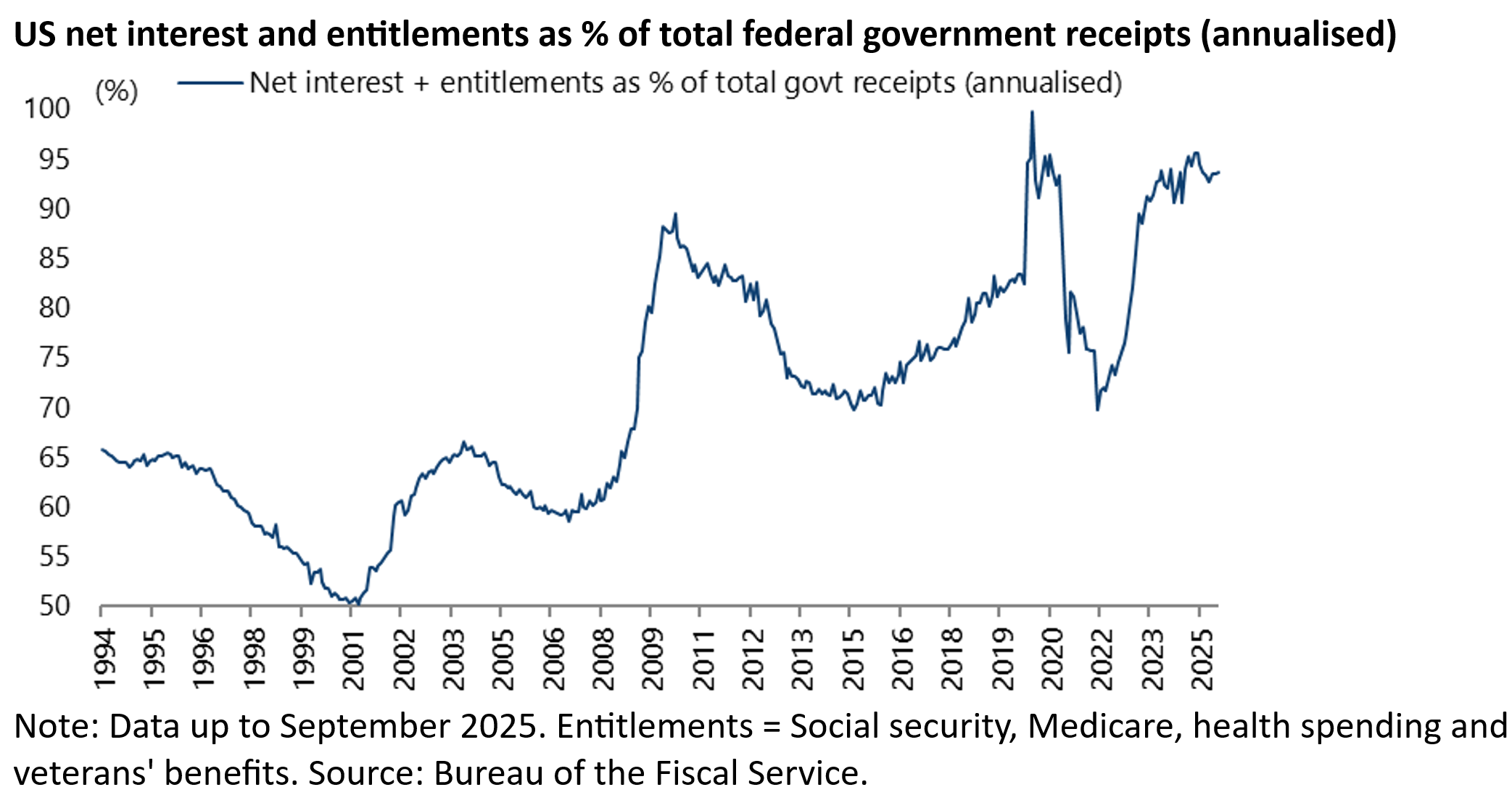

Meanwhile the prime driver of the Trump administration’s criticism of Jerome Powell is not concerns about the state of the economy but rather to get the cost of debt servicing down.

Net interest payments and entitlements were still running at 93.7% of total federal government receipts in the 12 months to September.

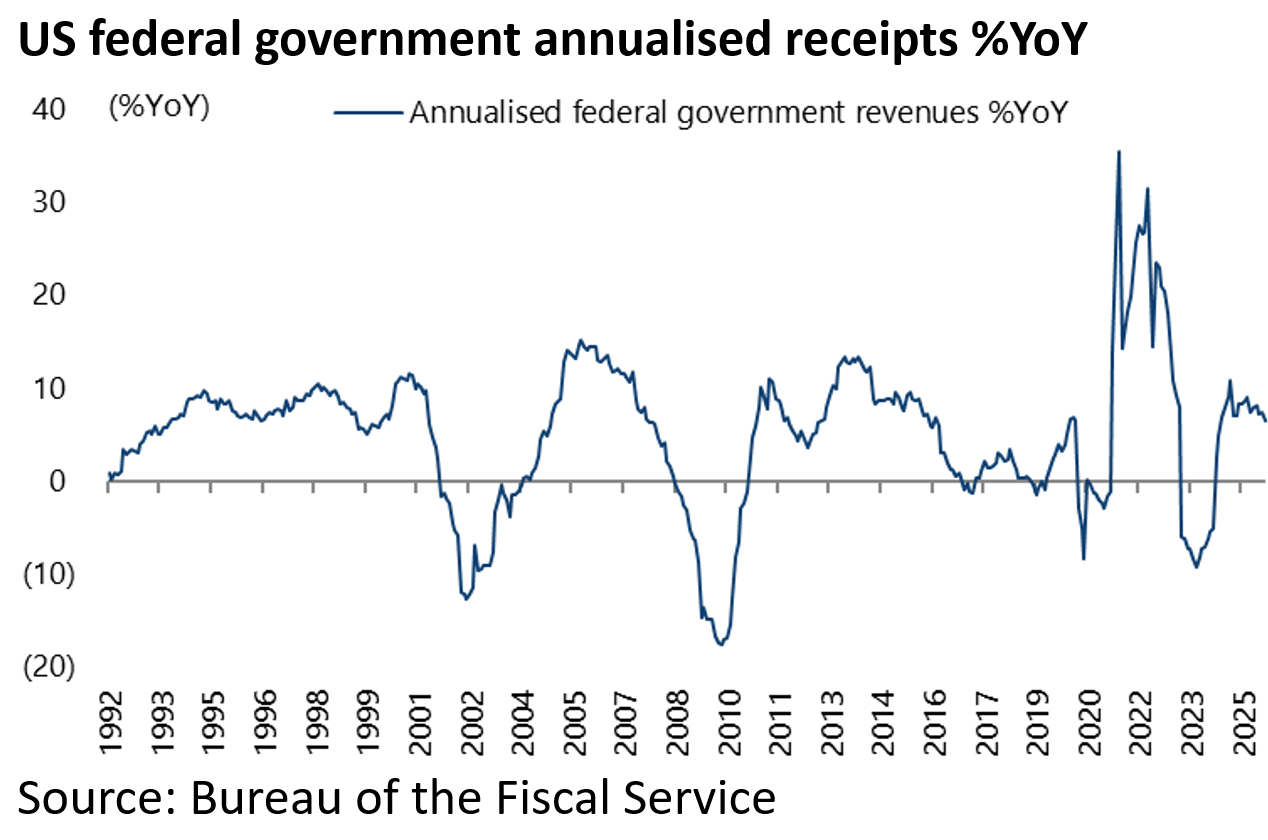

Total receipts are, for now at least, still not showing a big impact from increased tariffs.

Total federal government receipts rose by 3.2% YoY to US$543.7bn in September and are up 9% YoY to US$2.97tn in the period between April-September.

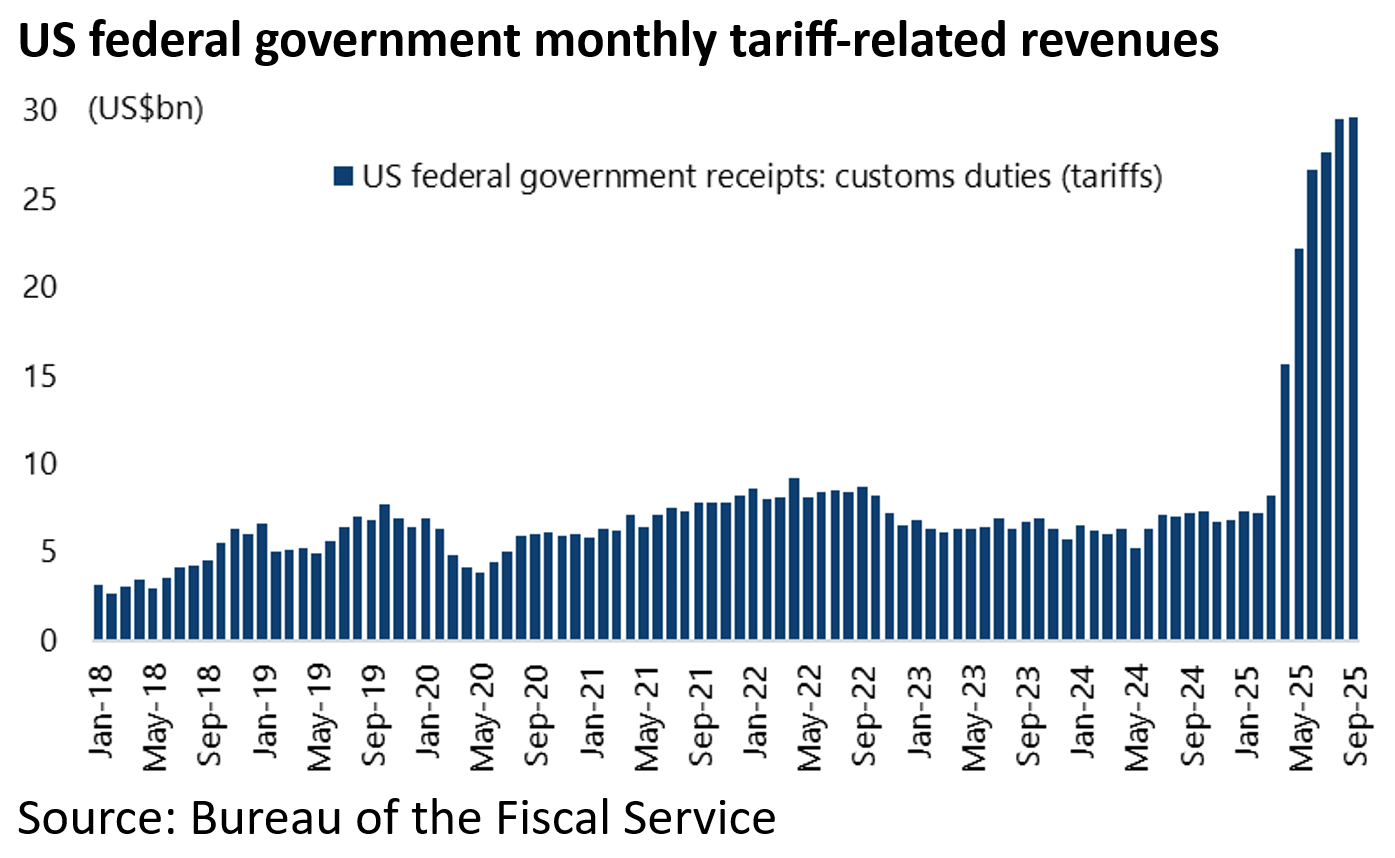

Still tariff-related revenues are up from US$7.25bn in February to a record US$29.7bn in September 2025 and were US$151.3bn in April-September 2025.

A Disjointed US Foreign Policy Approach Looks to be by Design

Moving on to more topical matters, running foreign policy on an ad hoc deal-making basis can generate newsflow, and divert attention from awkward domestic issues such as the Epstein case which continues to simmer as discussed here previously (see An Exploration of Trump’s View on Crypto, Short Term Treasuries and Yield Curve Control, 11 September 2025).

The past week has seen a classic example of the extreme volatility of the Trumpian approach to foreign policy.

Thus, Donald Trump’s telephone call with Vladimir Putin on 16 October was followed by his statement later on the same day that he would meet with the Russian president in Budapest which then followed by his statement on 22 October that he has now cancelled that meeting.

But the problem is that the effective conduct of foreign policy for the world’s major power requires a conceptual framework and this is what is conspicuously lacking in the current US administration.

The 47th US president certainly has no such framework and is also bereft of an adviser who has one. There is certainly no equivalent to Henry Kissinger who was the ultimate conceptual thinker.

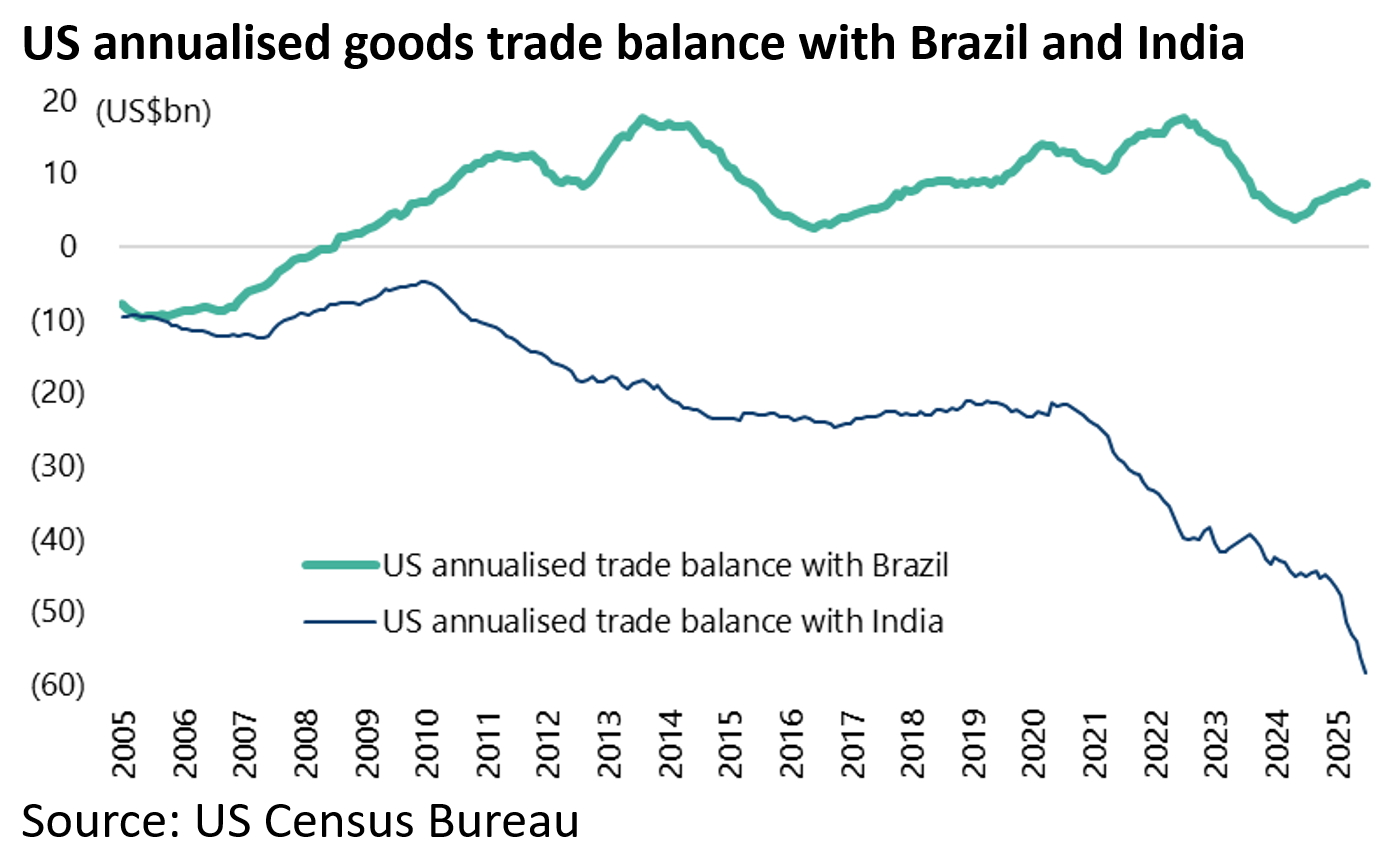

This has become only too starkly evident in recent months as Donald Trump has succeeded in bringing China, Russia, India and Brazil together like never before.

Indeed BRICS as a grouping has been regalvanised. Thus, as a result primarily of tariff provocations, most particularly in the case of India which currently faces 50% tariffs.

Meanwhile Brazilian president Lula is indignant against 50% tariffs imposed arbitrarily by Trump even though Brazil runs a trade deficit with the US.

Tariffs Singling out India Surprised Us

The singling out of India in this fashion is not what most people would have predicted, including this writer.

First, China has been buying more Russian oil than India but has not been similarly punished. (India imported an estimated 1.6m barrels/day of Russian crude oil in September compared with 2.0m barrels/day for China).

Indeed Trump in mid-August extended the tariff deadline as regards China for another 90 days to 10 November in the latest signal of his desire for a one-on-one meeting with Chinese President Xi Jinping who has continued to play hard to get.

Meanwhile New Delhi will not be happy that it now faces 50% tariffs whereas arch-enemy Pakistan is only facing 19%.

As regards the purchase of Russian oil issue, India has taken the position since the start of the Ukraine conflict in February 2022 that its duty is to pursue its own national interest which is clearly to purchase oil as cheaply as possible.

New Delhi has also had little patience with the pretence that Europe is not buying Russian oil when it is common knowledge that Europe has been buying Russian oil refined in India.

As one senior Indian bureaucrat commented to this writer two years ago it seems politically correct for the Europeans to buy Russian oil “so long as it is washed in the Ganges”.

This is the kind of humbug nonsense Trump as presidential candidate railed against.

Still presidential candidate Trump also said he would end the Ukraine conflict in 24 hours.

Unfortunately for him, Biden’s war has now become his war as he has chosen to listen to the neo-con lobby whose agenda is all about expanding NATO where the people of Ukraine are in reality pawns in a greater power game.

Still Trump is no neo-con and it is certainly possible that more U-turns can happen at any time.

The problem for Trump is that it is hard to project any deal on Ukraine as a “win” for the West since the Russians will only agree a deal where there is a formal renunciation of any Ukraine intentions to join NATO while Moscow will assert sovereignty over the four eastern and southeastern Ukraine regions they already effectively control, namely Donetsk, Luhansk, Zaporizhzhia and Kherson, as well as of course Crimea.

The Best Hope for a Real Deal Between the US and China

Meanwhile, the best hope for a real deal between US and China, if the long-sought meeting between the two leaders actually goes ahead on 30 October in Busan, South Korea on the sidelines of the Asia Pacific Economic Cooperation (APEC) summit as confirmed by White House press secretary Karoline Leavitt on 23 October, is the US dismantling its export controls on semiconductors in return for China allowing unfettered exports of rare earths.

This may seem far-fetched at the moment but anything is possible with the Donald.

The original export controls introduced by the Biden administration in October 2022 amounted to nothing less than the declaration of economic war against China, as discussed here at the time (see The Shadow Semiconductor Wars Explained, 23 November 2025).

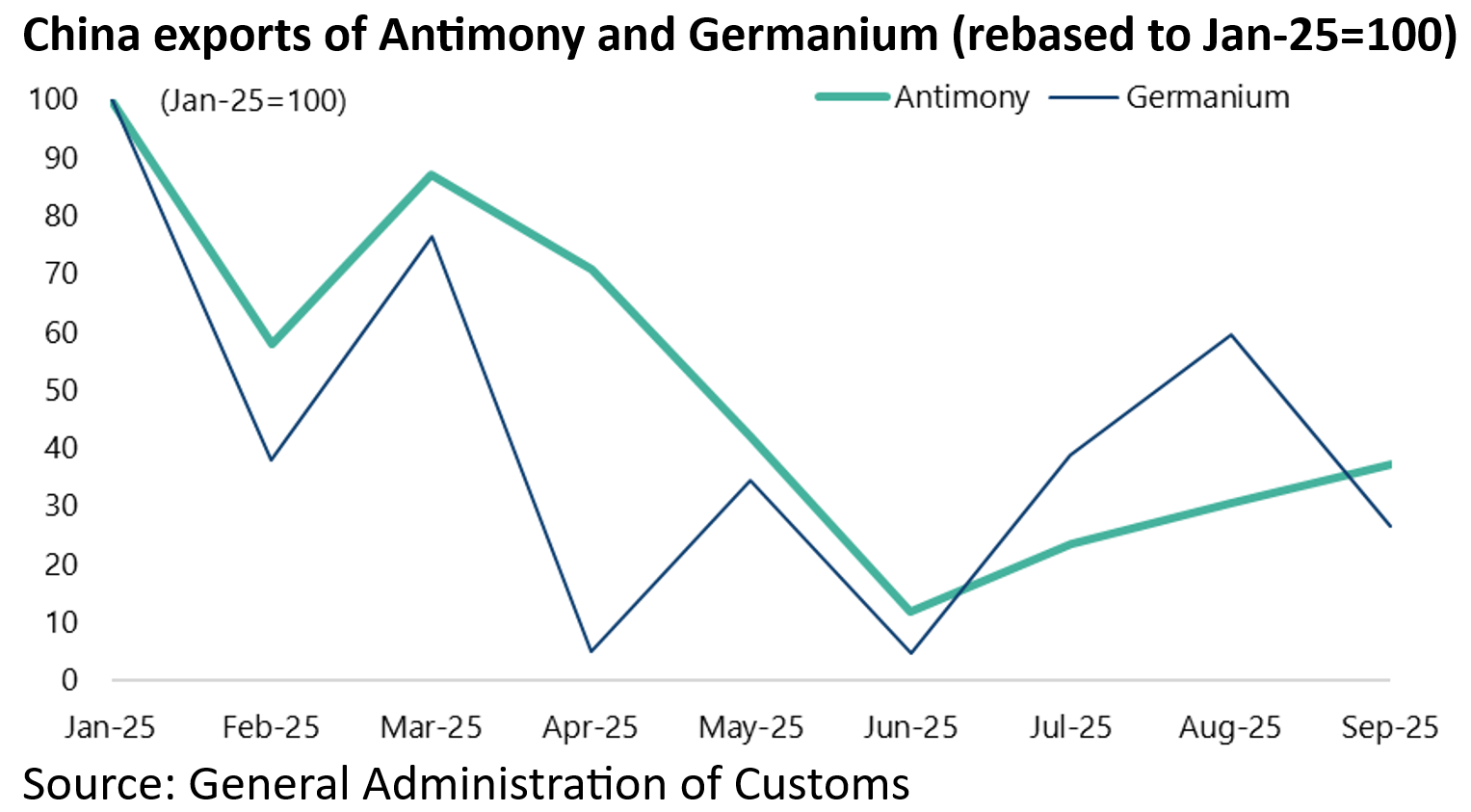

A real lasting improvement between the two countries would require a complete end to such a policy. But this year China has, for the first time, exercised its leveraged on rare earths to stunning effect which directly impacts America’s ability to wage war.

Thus, China continues to curb the export of the two most sought after of its rare earths from a military perspective.

Exports of antimony and germanium have declined by 63% and 73% respectively as of September compared with their January levels.

Meanwhile if such a deal remains theoretically possible, there has to be a growing risk that Beijing has decided that Trump is too unstable, in terms of the constant flip-flops in policy as reflected in the stance on Ukraine, to make it imprudent to invest too much political capital in seeking to secure a deal.

If that is indeed the case the rare earth issue remains a huge source of leverage for China since the Ukraine conflict has exposed that the US simply does not have the means to wage conflicts on all fronts in terms of access to weaponry and the components that go into the weaponry.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.