The Trumpian driven news cycle continues to dominate, as reflected in the recent headlines concerning Greenland.

Still the all-important issue is US-China relations.

The ultimate deal between Washington and Beijing would be complete abolition of American export controls on semiconductors in return for China’s complete relaxation of restrictions on exports of rare earths.

This makes sense logically since Beijing has explicitly linked these two issues since last year, after showing remarkable restraint previously, as it has become ever clearer that the US does not have the leverage over China it once thought it had on the trade and tariff issue.

Indeed on the rare earth issue the leverage is seemingly all on the China side.

China, for example, has a 92% market share of the global production of rare earth magnets which remain key components in many US weapons systems.

This lack of leverage is something the Washington national security establishment is having a hard time adjusting to.

And in the case of rare earths it increasingly looks like the US needs the rare earths far more than China needs the semiconductors.

In that respect, while the Chinese government has said it no longer wants its tech companies buying Nvidia’s AI chips, this writer has been skeptical about whether this was really the case in practice.

Yet it has been reported of late that Chinese customs officers are now on the lookout for smuggled banned Nvidia chips whereas previously there were estimates that 10% of the banned Nvidia chips ended up in the mainland presumably with the central government’s tacit blessing (see, for example, Financial Times article: “China launches customs crackdown on Nvidia AI chips”, 10 October 2025).

In the same article it was also reported that at least US$1bn worth of Nvidia’s top AI chips were smuggled and sold in China in the three months from May.

Will China Every Agree to Set up US Based Production Capacity?

Beyond the above issue of the two countries’ regimes of export controls, both of which are designed to prevent the leakage of technology, another issue is whether China could offer Donald Trump a “win” by agreeing to set up production in America.

The two leaders are due to meet again in April in Beijing.

Two obvious candidates for such production are CATL and BYD.

In this respect it should be recalled that Trump’s stated reason for advocating tariffs, aside from boosting fiscal revenues, is to create an incentive for foreign companies to move production to America for those wanting to access the American consumer market.

Naturally, such policies will be anathema to Washington’s national security establishment which is for now belatedly and manically focused on securing rare earths from the likes of Pakistan, ironically a long-term China ally.

See, for example, the Financial Times article: “Pakistan courts US with pitch for new Arabian Sea port”, 4 October 2025. Still as the saga over TikTok has demonstrated yet again, Trump is not a national security zealot nor indeed a hawk on China.

It is also the case that he is increasingly sympathetic to this writer’s longstanding view, doubtless also argued by Nivida boss Jensen Huang in private conversations with the American president, namely that the export controls on semiconductors introduced by the Biden administration in October 2022 have proved to be a massive “own goal” for the US to employ a soccer analogy.

This is because they have triggered an overwhelming incentive for China to set up its own semiconductor value chain while depriving US tech companies of a major customer.

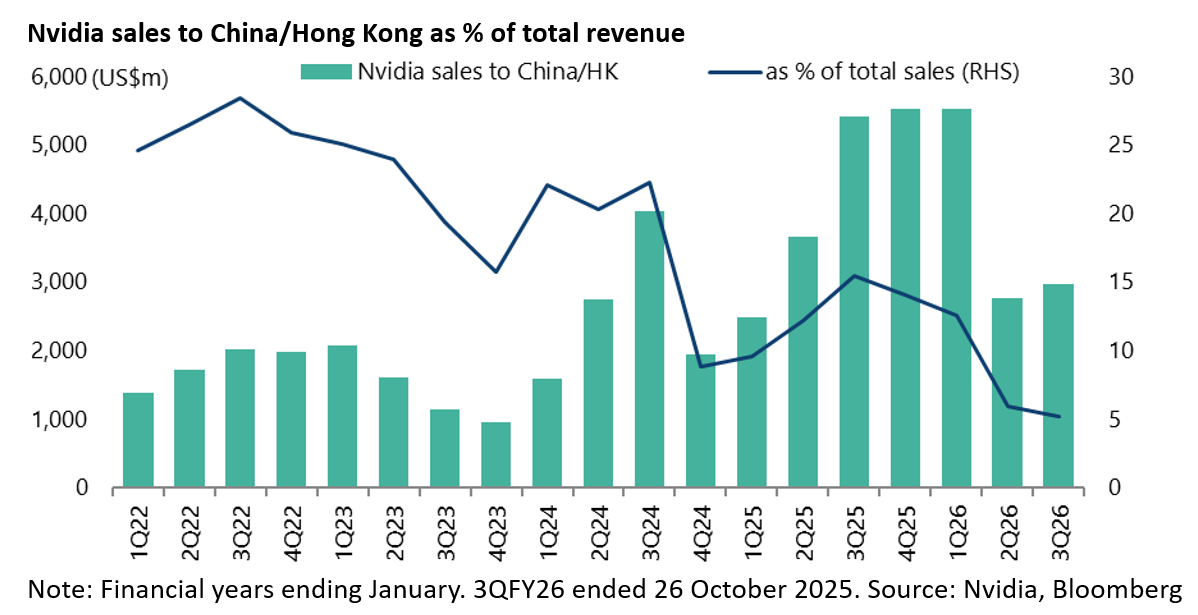

Nvidia’s sales to China (including Hong Kong) declined by 24% YoY to US$2.77bn in 2QFY26 ended 27 July and were down 63% YoY to US$2.97bn in 3QFY26 ended 26 October 2025.

As a result, China/HK’s share of Nvidia sales has fallen from 26.4% in FY22 ended 30 January 2022 to 13.1% in FY25 ended 26 January 2025 and only 5.2% in 3QFY26.

All this suggests that the potential for such a deal is not impossible even though it will involve Trump acting specifically against the agenda of the national security lobby, something he has conspicuously failed to do in the case of Ukraine where he has ended up following the exact opposite of the policy he campaigned on.

As a result, what he used to call “Biden’s war” has now become his war in political terms.

Indeed the Wall Street Journal reported at the time that Trump was on the point of telling President Xi Jinping he would allow China to buy the most advanced Nvidia chips when he met with Xi in Korea in late October only to be talked out of it at the last minute by Secretary of State Marco Rubio (see WSJ article: “Trump Aides Sank Nvidia Push To Export AI Chips to China”, 4 November 2025).

Americans are Increasingly Tired of Tariffs

Meanwhile, it is surely the case that the more tariffs impact prices in America, the more they risk becoming unpopular.

There is growing evidence of this.

An Economist/YouGov poll conducted on 20-22 December shows that 56% of respondents disapprove of the way Trump is handling the tariff issue, with only 36% approving.

An earlier Economist/YouGov poll conducted on 15-17 November also shows that 73% of Americans say that Trump’s tariffs have increased the prices they have paid by either a lot (40%) or slightly (33%).

If there is a deal it will likely mean, in investment terms, that Chinese stocks will no longer be viewed as uninvestable by managers of America-based global equity funds.

It would also mark a reprieve, if likely only a temporary one from a longer term historical standpoint, in the growing rivalry between the world’s two major economic powers.

On this point, Beijing must surely be aware that other American presidents could be much more ideologically hostile, and also perhaps less easy to manipulate than the Donald.

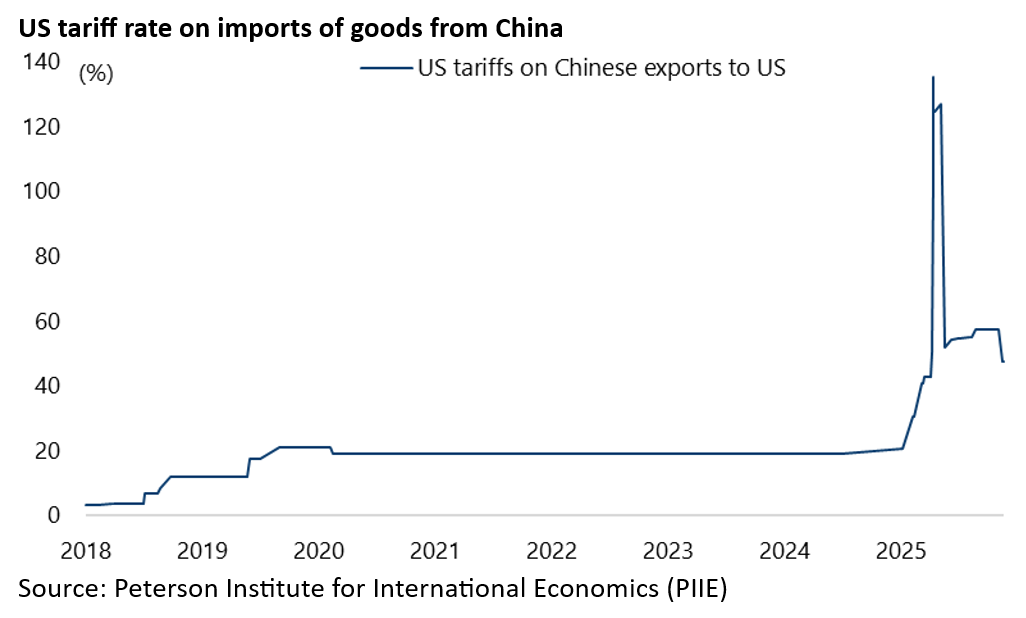

Still it is also the case that President Xi Jinping is surely not going to sign any deal endorsing the current tariff rate on US goods imported from China which is 47.5%, according to the Peterson Institute for International Economics.

The 15% level agreed by Europe would surely be much more acceptable, though Trump has threatened last weekend to impose an additional 10% tariffs on imports from several European countries over the Greenland issue.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.