China’s Policy Driven Bull Market

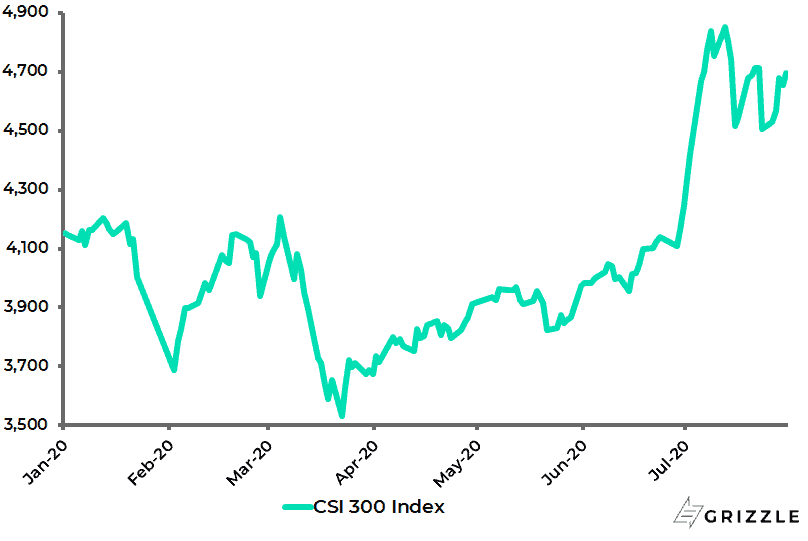

The Chinese stock market has resumed rallying since the start of the current quarter helped by a positive comment as regards equities from the central government.

The front page of the state-owned China Securities Journal on 6 July printed: “Fostering a ‘healthy’ bull market after the pandemic is important”. This is an important signal in what has always been a policy-driven stock market.

China CSI 300 Index

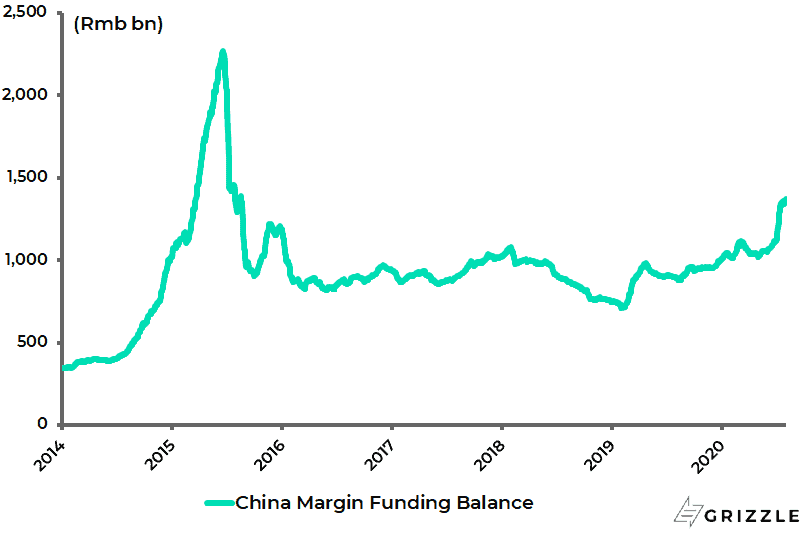

Margin lending has also begun to rise, though it is not yet anything like on the boom-bust scale seen in 2015. China margin financing balance has increased by 21% so far this quarter to Rmb1.37tn at the end of July, the highest level since August 2015, and is up 36% year-to-date.

This compares with the peak of Rmb2.27tn reached in June 2015.

China Margin Financing Balance

On this point, while it is the case that the deleveraging policies of recent years have peaked out as suggested by the gradual pickup in credit data seen so far this year in China, Beijing is not engaged in an aggressive reflation.

Thus, Guo Shuqing, China’s top banking regulator and the architect of the squeeze on shadow banking in recent years, was quoted in June saying that China “won’t flood” the economy with cash nor do negative rates.

This comment is worth highlighting since Guo, besides being chairman of the China Banking and Insurance Regulatory Commission (CBIRC), is also the senior party official in the People’s Bank of China which means the PBOC Governor is subordinate to him.

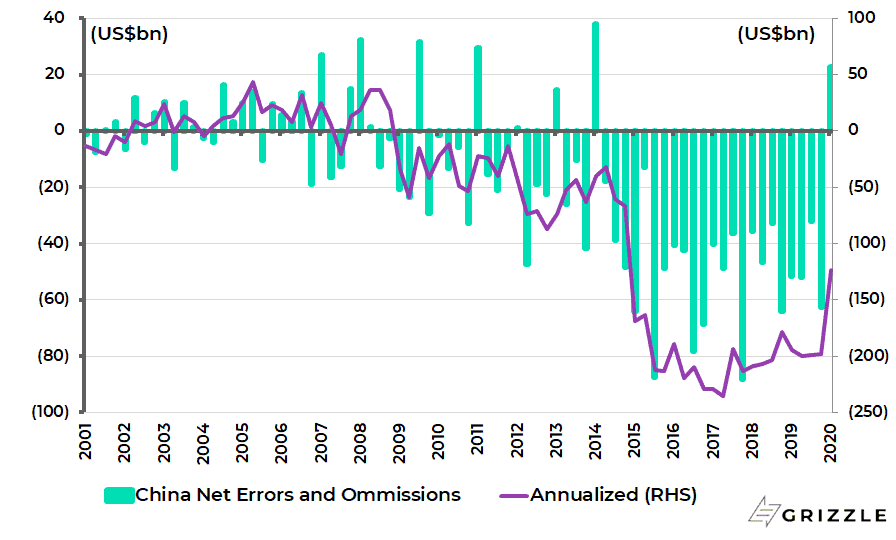

Another positive on China is evidence of renewed capital inflows for the first time in several years.

The net errors and omissions item in China’s balance of payments turned from a US$62.6bn deficit in 4Q19 to a US$22.6bn surplus in 1Q20, the first quarterly surplus since 1Q14.

As a result, on an annualised basis, the net errors and omissions deficit declined from US$198.1bn in 2019 to US$123.8bn in the four quarters to 1Q20, the lowest level since 2014.

China Balance of Payments: Net errors and Omissions

Chinese equities remain a structural overweight as do Chinese bonds.

The central government has navigated the pandemic crisis in a manner that makes it look as if other governments have been engaged in blind panic in terms of the scale of over-the-top fiscal and monetary stimulus announced.

As for Hong Kong, the rally in MSCI Hong Kong and the Hang Seng Index since the controversial national security bill was first announced in May contrasts with the hysterical Western media coverage on the same issue.

The MSCI Hong Kong and the Hang Seng Index have risen by 8.6% and 7.3% respectively since 22 May.

MSCI Hong Kong and Hang Seng Index

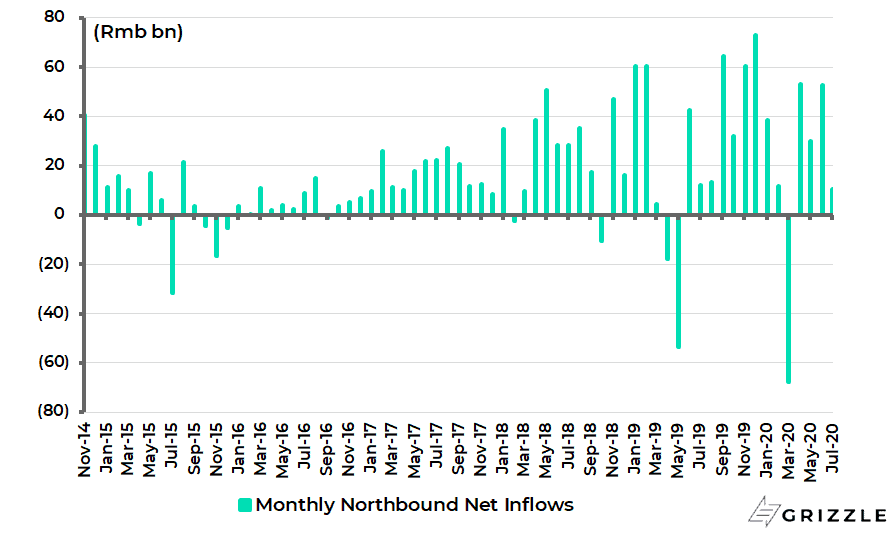

Meanwhile the flows in Hong Kong’s Stock Connect have remained healthy in both directions in the past quarter.

Northbound flows (i.e. from Hong Kong to mainland China) recorded a net inflow of Rmb136bn last quarter and Rmb128bn year-to-date.

Stock Connect Monthly Northbound Flows

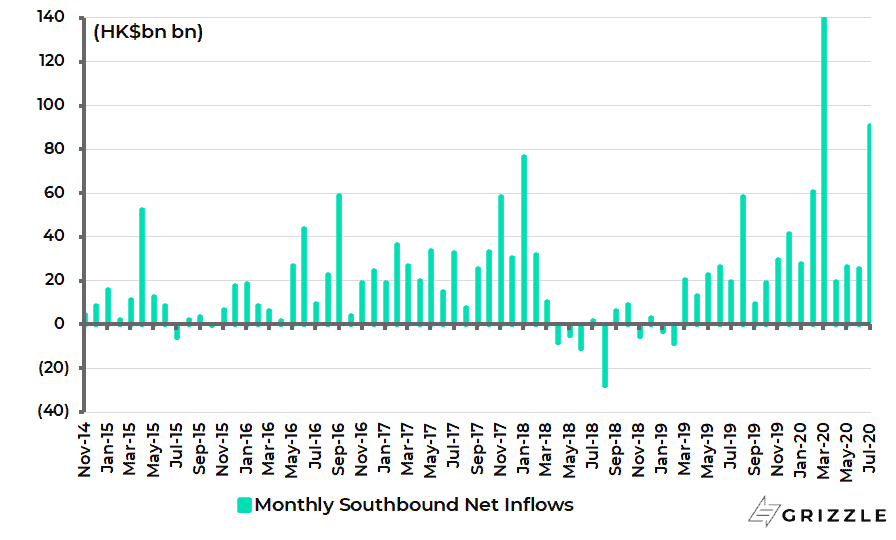

Southbound flows (i.e. from mainland China to Hong Kong) recorded a net inflow of HK$72bn in 2Q20 and HK$391bn year-to-date (see following charts).

But the real boom in Southbound flows will come, in due course, when the likes of Alibaba enter the Stock Connect.

This means mainland investors will then be able to buy the stock for the first time. The same will apply to other Chinese companies quoted in America who are now also seeking listings in Hong Kong.

Stock Connect Monthly Southbound Flows

Base Case for U.S. Market Remains a V-Shaped Recovery

Meanwhile returning to more global themes, cyclical stocks will enjoy renewed outperformance, as they did for a period last quarter, if V-shaped recovery expectations revive amidst yield curve steepening.

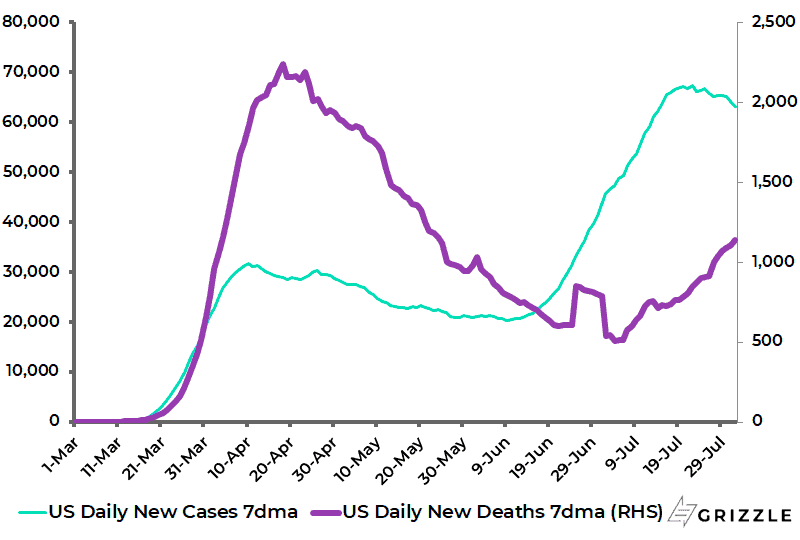

This remains the base case here, though it should be noted that the death rate in the US has picked up over the past week.

The 7-day average daily Covid-19 death rate in America has risen by 26% in the past seven days from 907 to 1,140.

That said, the positive point is initial evidence that new cases have peaked out in America.

The 7-day average number of daily new cases peaked at 67,317 on 22 July and has since declined by 4,249 or 6.3% to 63,068.

US Covid-19 Average Daily New Cases and Deaths

In the event of such a V-shaped outcome, a likely decision by the Federal Reserve to implement yield curve control will then reassure investors that bond yields will remain lower for longer which should again support high PE growth stocks.

In this respect, it is assumed for now that the US Treasury bond market will react in a docile fashion to any announcement of yield curve control where the Fed fixes the yield of the five-year or, even more controversially, the ten-year Treasury.

This is assumed for now because such is the precedent from Japan where a yield curve control regime has been in place since September 2016 when the Bank of Japan announced it would target the yield on 10-year JGBs at “around zero percent”.

Still if the yield curve control regime is likely to stick in the first instance, a bond market revolt at some point in America cannot be ruled out, most particularly if monetary and fiscal monetary policy continue to converge as is likely, and if the Fed continues to flirt with monetisation in terms of financing the central government directly.

Such a revolt becomes more likely the further along the yield curve the Fed tries to control.

Fed is Merely Flirting with Yield Curve Control at this Point

Amidst all the recent talk of helicopter money and the potential adoption of Modern Monetary Theory (MMT), the term “flirt” with direct central bank monetisation of federal government spending is used deliberately.

Consider the example of the Fed’s Covid-19-triggered move to purchase corporate bonds.

Technically, the Fed is not buying the corporate bonds outright.

Rather, so far as this writer understands the process, the Fed has established and extended loans to a special purpose vehicle for the corporate credit facilities, which the Treasury’s Exchange Stabilisation Fund will make a US$75bn equity investment in.

The Treasury’s equity will be leveraged up to ten times by the Fed to purchase high-grade corporate bonds with remaining maturities of up to five years.

If these bonds default, it would seem that the liability of the defaulted bond is not transferred to the Fed itself but rather, in the first instance, to the Treasury’s Stabilisation Fund. On this point, it is worth quoting the exact words from the Fed’s official statement: “The Board (i.e. the Fed) does not expect at this time that the SMCCF (Secondary Market Corporate Credit Facility) will result in losses in excess of the Department of the Treasury’s equity investment.

Accordingly, the SMCCF is not expected to result in losses to the Federal Reserve or the taxpayer.”

So, technically, it could be argued that this does not look yet like direct monetisation.

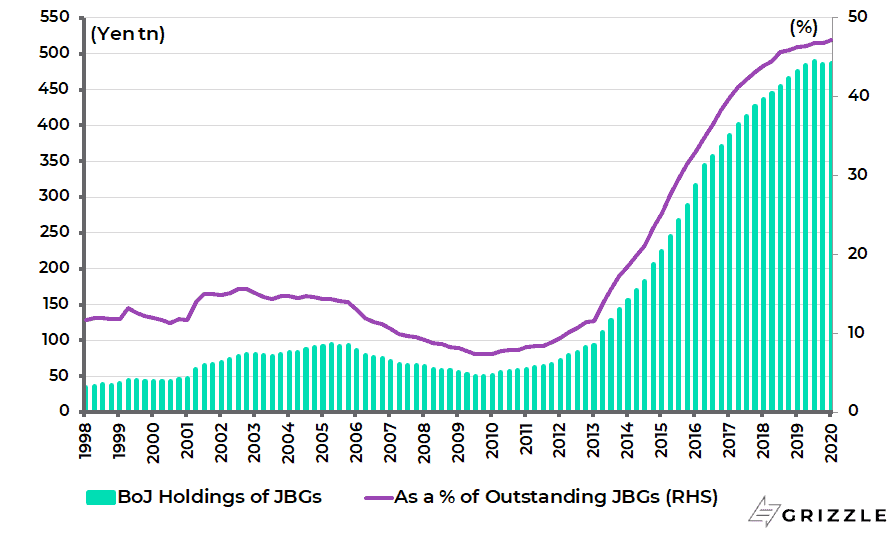

Still this is a slippery slope where the direction of travel looks to be the Fed monetising the government directly, just as is in Japan.

There the official line that the Bank of Japan is not engaged in direct monetisation of the government, since it is only buying JGBs on the secondary market, has become increasingly hard to maintain as the Bank of Japan has owned an ever greater percentage of JGBs outstanding.

The central bank’s current ownership is now a record 47.2%.

Bank of Japan holdings of JGBs

Meanwhile, what is abundantly clear is that government bonds with fixed or pegged yields no longer make interesting investments.

This is why there is really no alternative to equities with the obvious hedge on the currency debasement implied by G7 central bank policies gold and silver, and gold and silver mining stocks.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.