This writer was recently in Brazil for the first time in a year. There has been an incredible change of sentiment since then.

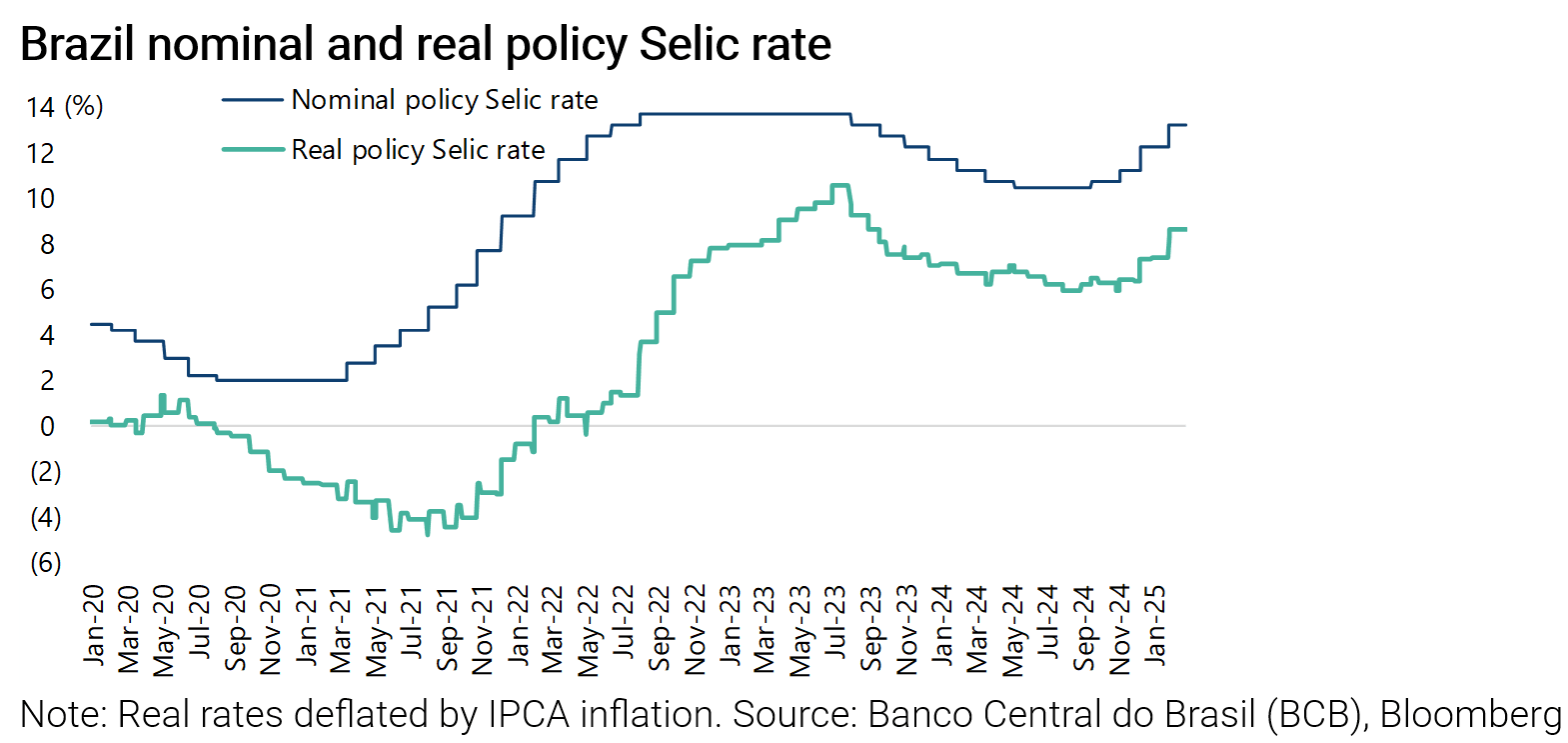

At the start of 2024 there was huge focus on the potential for rate cuts in an anticipated Fed easing cycle given the then high level of real interest rates, running at 7.1%.

One year on and there is now extreme negative sentiment among locals, based on fiscal deterioration under a Lula government which has run a populist policy expanding social spending in an economy where tax revenues as a percentage of GDP are running at an already very high level for an emerging market of 33% of GDP, according to OECD data.

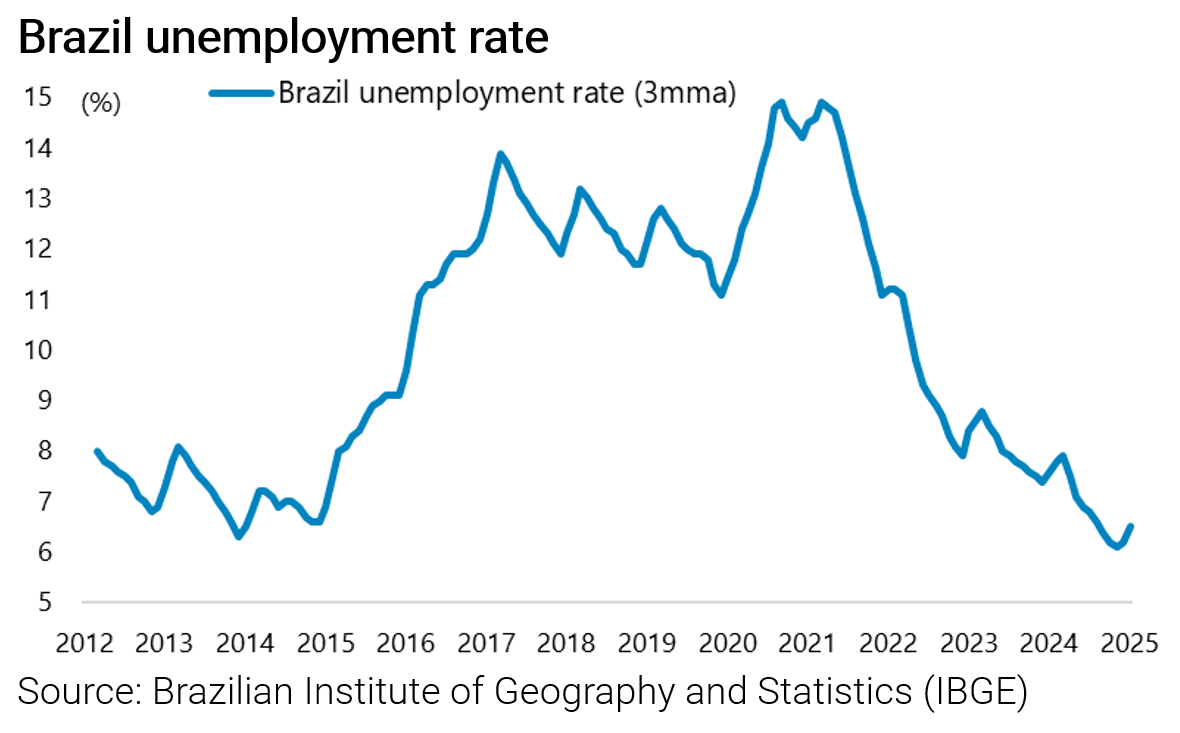

For now the economic data remains strong reflecting the stimulatory fiscal policy with unemployment rate at 6.5% in the quarter ended January 2025, though up from a record low level of 6.1% in the quarter to November 2024.

But with monetary tightening intensifying as investors demand a risk premium for owning local currency-denominated debt, the economy seems likely to hit the wall at some point in coming quarters.

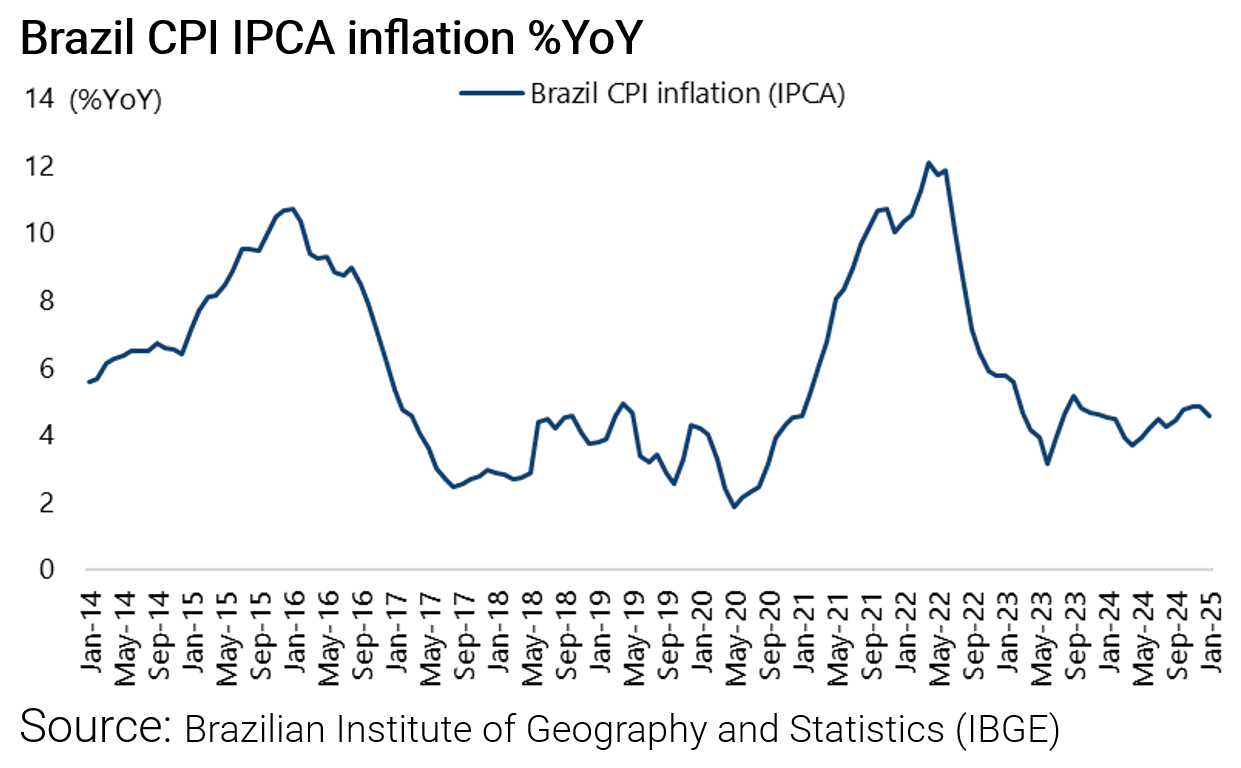

With inflation at 4.56% YoY in January though down from 4.83% YoY in December, the central bank has already indicated another 100bp of tightening in the next meeting on 19 March following a 100bp hike on 29 January, while money markets are pricing short rates reaching around 16% by the second quarter.

The Banco Central do Brasil (BCB) has already raised the Selic rate by 275bp since September to 13.25%.

So, for now at least, the recently Lula appointed central bank governor Gabriel Galipolo has followed the tightening path of his orthodox predecessor Roberto Campos Neto.

Still on the fiscal side there is no real evidence as yet of a desire to cut spending while there is growing resort to use Brazil’s public sector banks to finance spending off the official budget.

In this respect, many of the reforms of the social security system under the previous Jair Bolsonaro administration have been diluted, if not undone.

It is the case, for example, that 60% of pensions are again linked to the minimum wage.

One key positive achievement of the Bolsonaro government was reform of the pension system, with the retirement age raised to 62 for women and 65 for men.

Previously retirement was set on the basis of length of contribution at 35 years for men and 30 for women.

The reform also limited social security benefits by averaging salaries throughout the working life of the contributor.

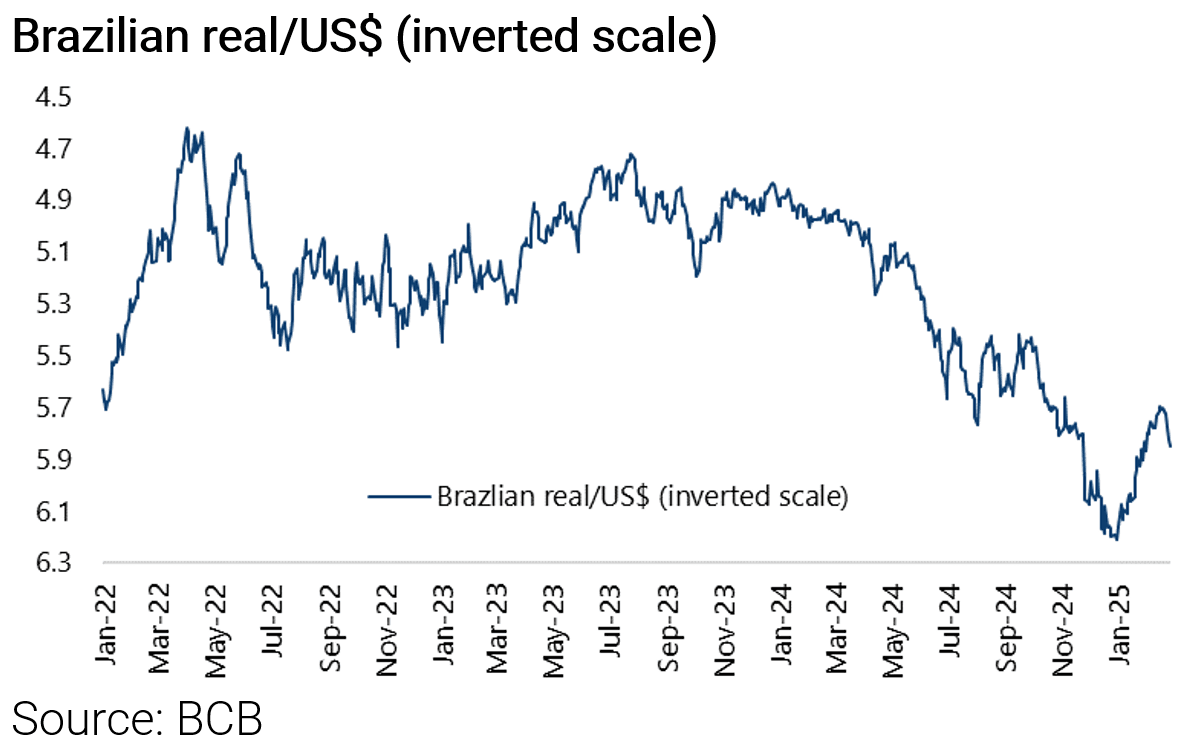

Meanwhile, the latest inflation data does not fully reflect the 22% depreciation of the real against the US dollar last year, though it has appreciated by 5.9% year-to-date.

It is true that Brazil has stood out in the quanto easing era by maintaining high real interest rates.

But this has been a feature of the country for decades.

The result has been a system where Brazilians have been prepared, unlike Argentinians, to keep their money at home since they were paid a decent return on their capital though, admittedly, the availability of high real rates meant that bonds have usually been favoured over stocks as continues to be the case today.

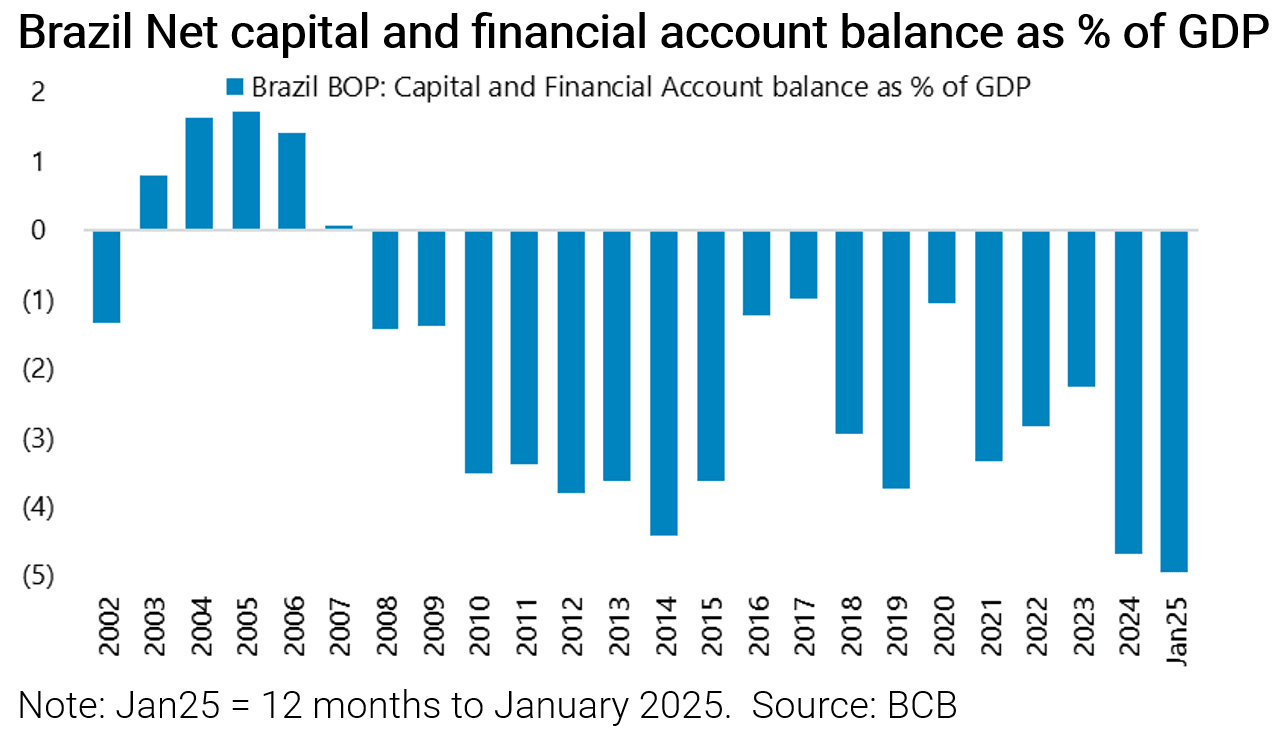

Rich Locals Moving More Money out of Brazil

Still there is of late emerging evidence of capital flight as Brazilians grow weary of a Lula who, in his third term in power, seems finally to be behaving like the left-wing bogeyman wealthy Brazilians feared when he first came to power back in 2003.

Thus, net capital and financial account outflows were 4.9% of GDP in the 12 months to January, up from 2.3% in 2023.

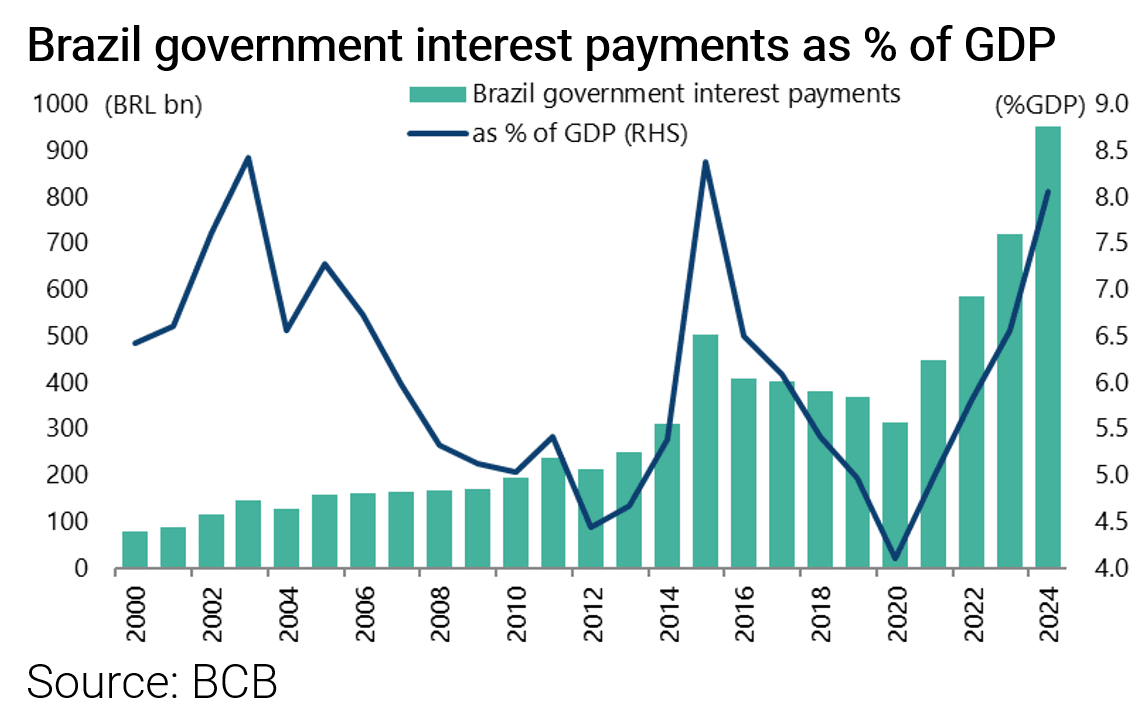

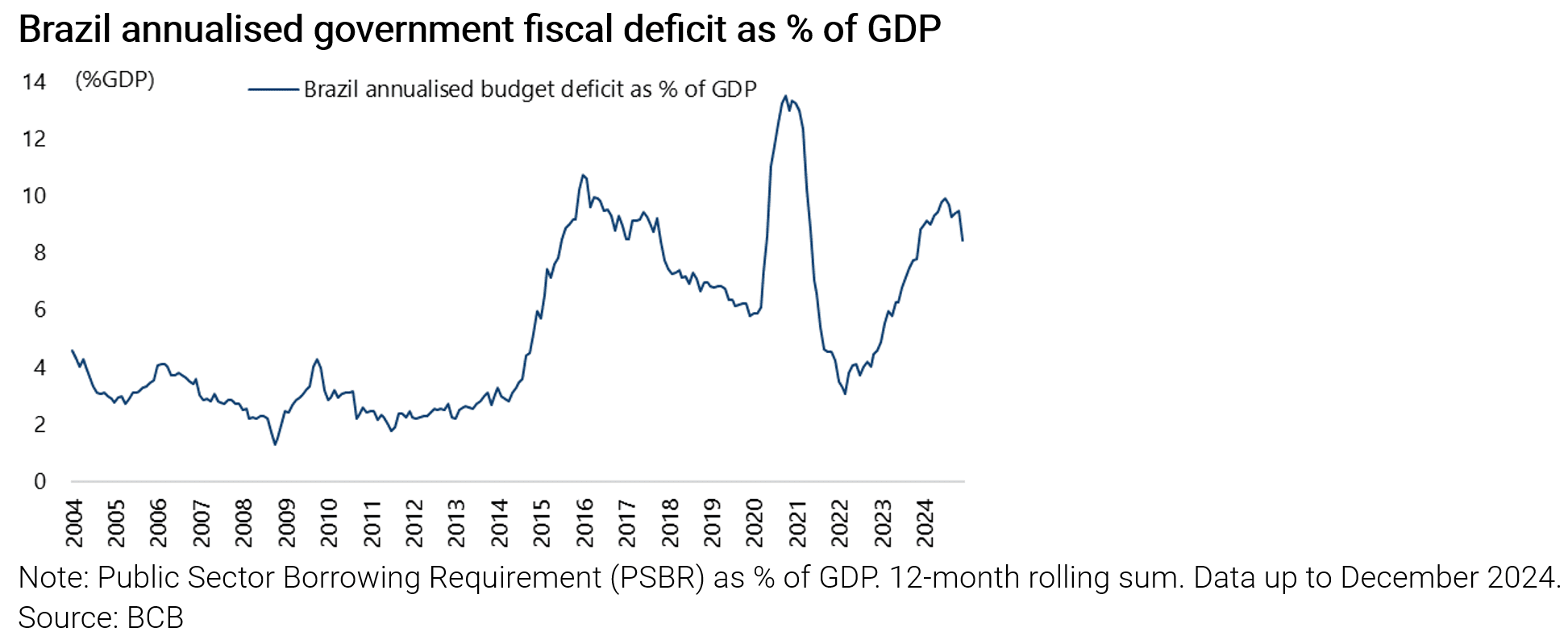

While the urgency of the fiscal issue is best reflected in the statistic that the government’s interest payments are running at an enormous 8.1% of GDP.

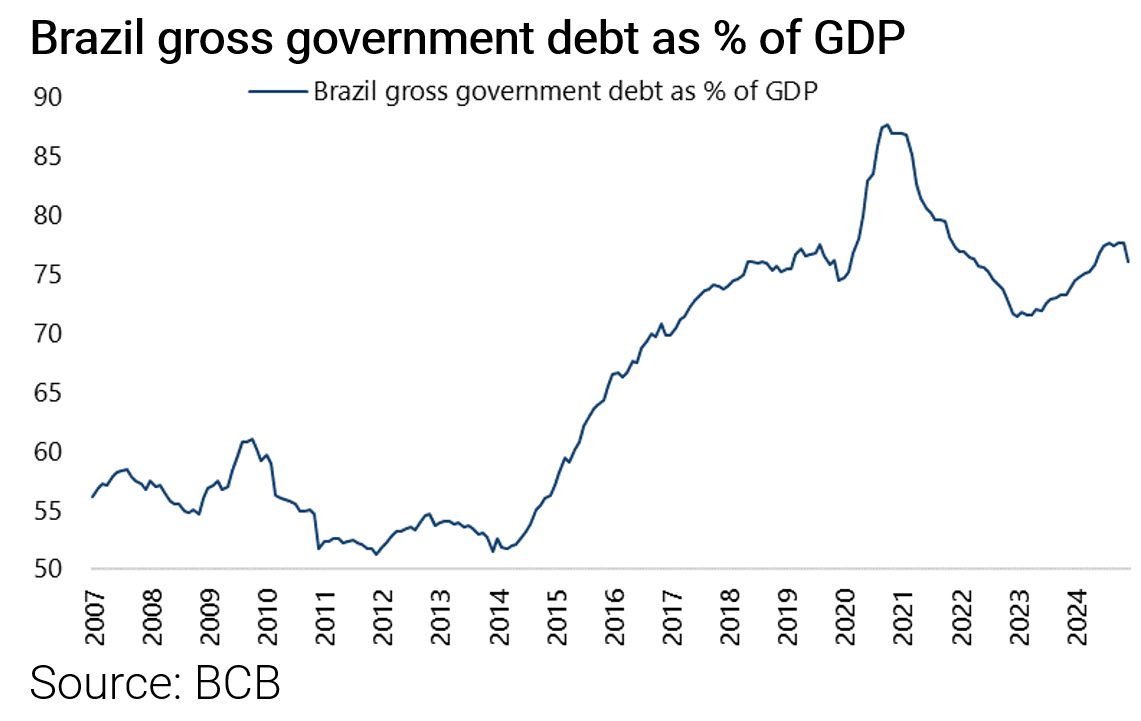

Meanwhile, with such high real rates and government debt to GDP of 76%, the current negative dynamic is that aggregate government debt is rising at a rate of two to three percentage points of GDP a year.

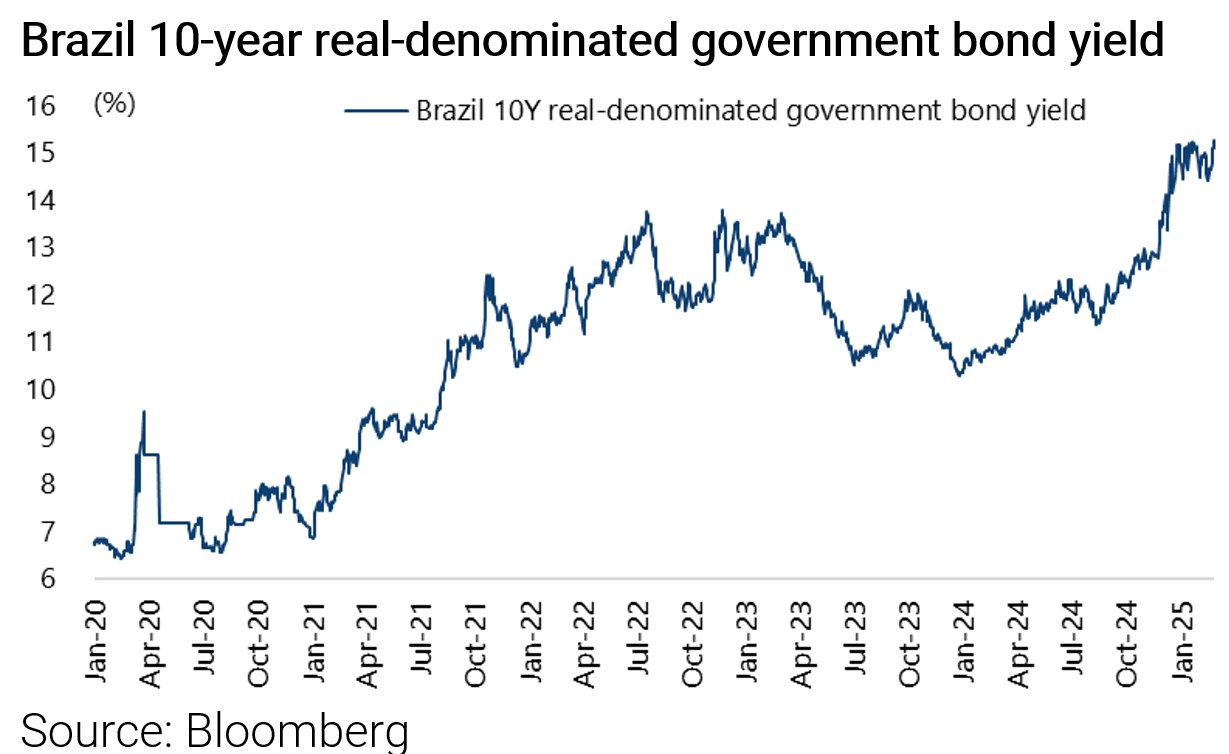

Local Savers Fleeing Asset Managers in Favor of Local Bonds

The situation has led to some convulsions in the previously booming asset management industry as savers have opted to withdraw money from both hedge funds and equity funds in favour of local fixed income where it is possible to lock in a 15% return on long-term real government paper.

For example, R$364bn (US$67bn) was withdrawn from local hedge funds last year.

Lula Stepping Down Would Benefit Bonds, Stocks and the Currency

If this is the negative, the reality is that debt, currency and equites will rally hard on any evidence that Lula is exiting power.

Still with the next general election not due to be held until October 2026, a potential positive catalyst for the market, in terms of a change in government, remains some way off.

Indeed the view of locals is that markets will not start to trade the election until the end of this year.

It is also the case that Lula has stated that he does not rule out the possibility of running for a fourth presidential term.

Impact of a Bolsonaro Arrest?

There is also the issue of the extreme polarisation of the Brazilian electorate with Lula defeating Bolsonaro in the October 2022 presidential runoff election by the narrowest of margins (50.9% vs 49.1%).

On that point, there is growing talk that there is a risk Bolsonaro will be arrested for his alleged role in the Brazilian equivalent of America’s 6 January 2021 incident when his supporters questioned the result of the last election.

On this point, Bolsonaro was charged on 18 February by chief prosecutor Paulo Gonet Branco with overseeing a vast scheme to hold on to power after losing the 2022 election, including one plot to annul the vote and another to assassinate then president-elect Lula (see New York Times article: “Brazil Charges Bolsonaro With Plotting a Coup After 2022 Election Loss”, 18 February 2025).

It is now up to the Supreme Court to decide whether to accept the charges and order Bolsonaro’s arrest and put him on trial.

For the record, the federal police in late November formally accused Bolsonaro of multiple crimes related to an alleged coup plot against Lula.

While the Superior Electoral Court in June 2023 banned Bolsonaro from running for office for eight years until 2030.

Such developments have further polarised the political atmosphere.

Bolsonaro’s supporters, for example, are of the view that the court system, from the Supreme Court down, is highly politicised.

The hope in financial circles is that, if Bolsonaro is really disqualified from running in the election as seems likely, then he will endorse a centre-right candidate which will have a much better chance of defeating Lula.

On that point, the favoured candidate is Sao Paulo Governor Tarcisio de Freitas.

Still the risk is that Bolsonaro nominates his son Eduardo Bolsonaro, at which point the view is that Lula would win.

If there is a brief account of the state in play, for those already invested in real-denominated assets the real returns are such that an investor is probably paid to wait.

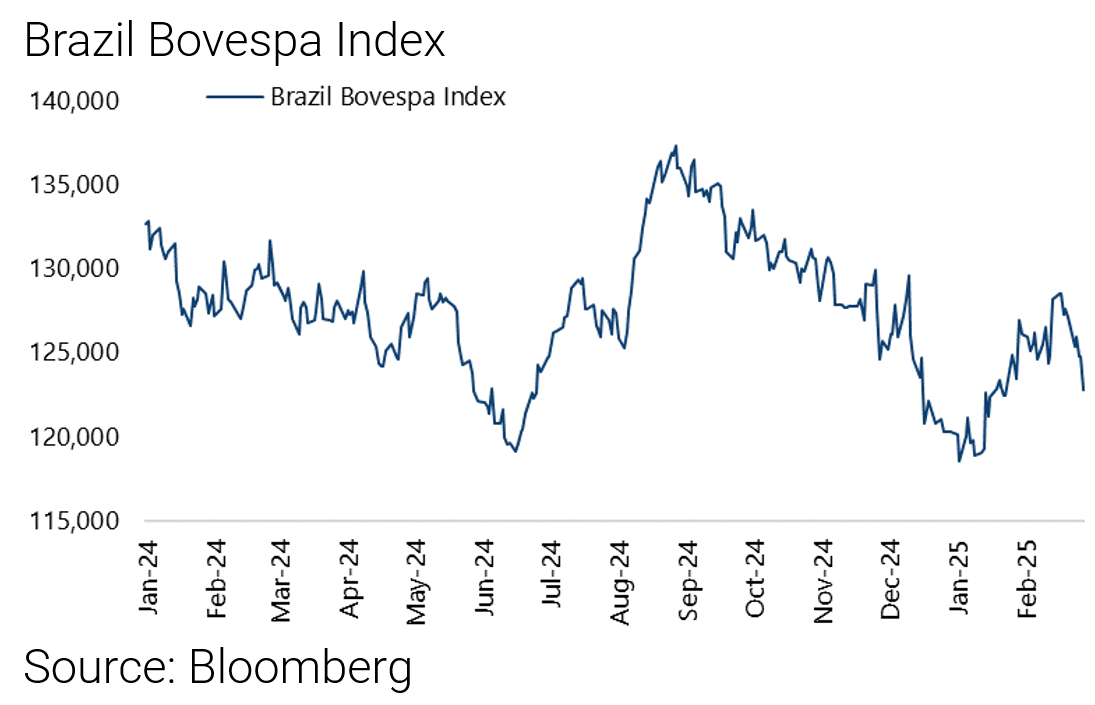

Brazil One of the Cheapest Stock Markets Globally

As regards equity valuations, the Bovespa Index now trades on 7x 12-month forward earnings with a forecast 2025 dividend yield of 7.3%.

This makes Brazil one of the cheapest stock markets globally.

It is also the case that companies are buying back shares reflecting the cheap valuations. 101 companies reportedly approved buyback programmes last year, with the total value of outstanding buyback programmes approaching R$80bn (US$13bn).

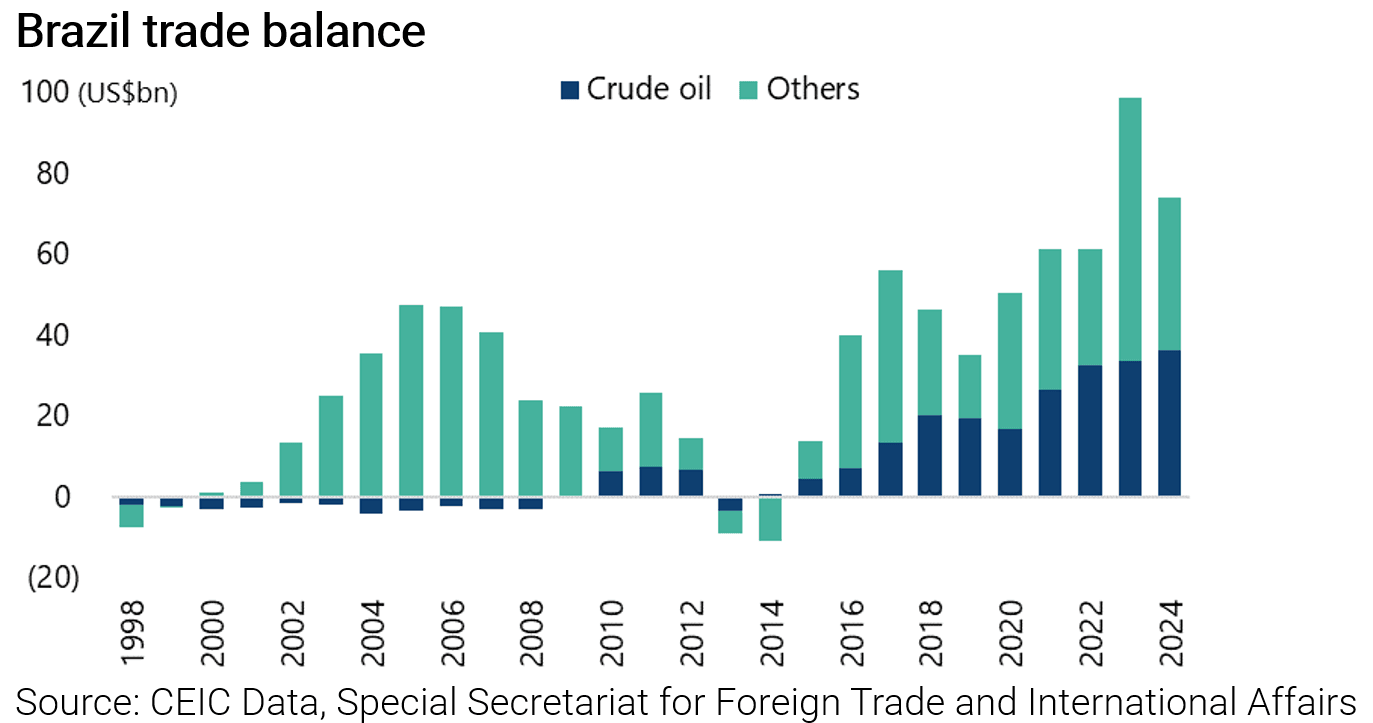

Meanwhile one macro positive continues to be the growth in oil production which has added US$40bn to the trade surplus with that another US$40bn expected in the next five years.

The result is that, while the country has a fiscal deficit of about 9% of GDP,

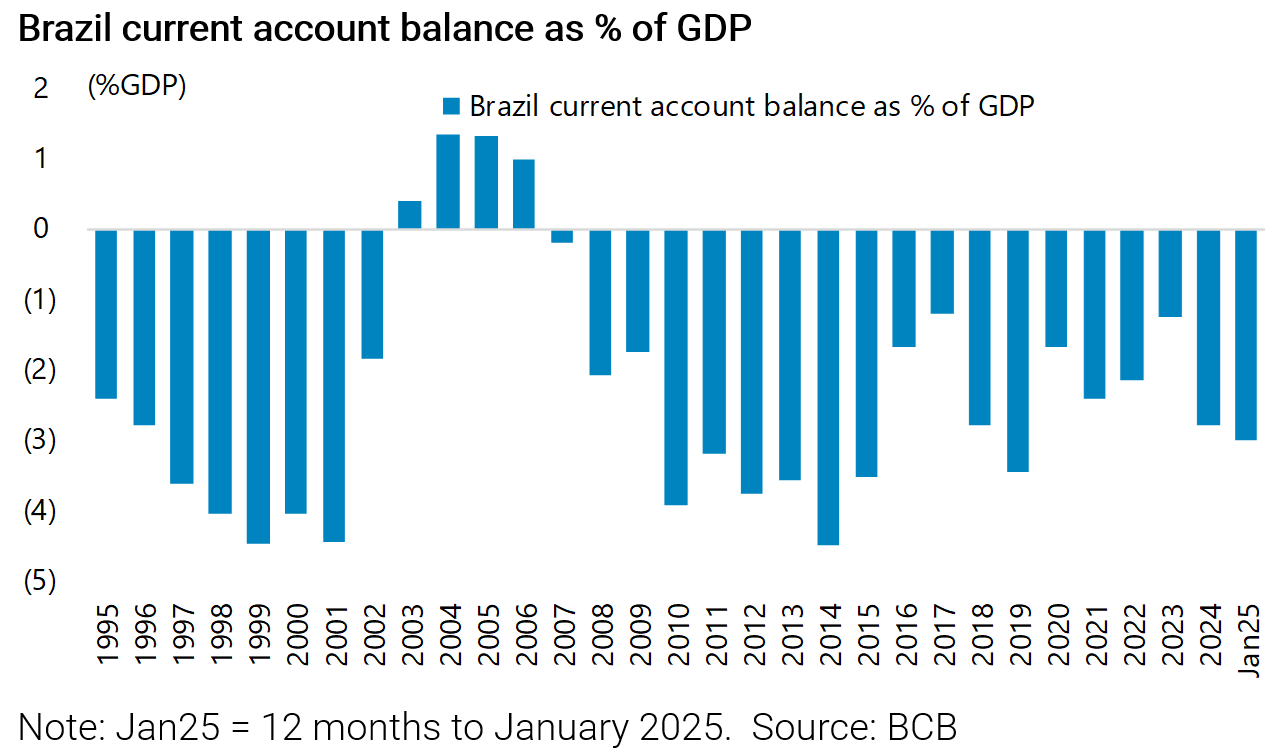

the current account deficit is running at “only” 3% of GDP in the 12 months to January, though up from 1.3% in 2023.

About Author

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.