Cannabis Stocks Have Been a Golden Goose, But Will the Good Times Continue?

If you were fortunate enough to discover the Canadian cannabis industry in 2017 and bought shares in the index, you would be up 82%, outperforming the S&P 500 by 70% over the last two years.

Some individual stocks have done even better with Canopy Growth, Cronos, and Aurora Cannabis up between 230%-680%.

Cannabis investors have been rewarded handsomely for their belief that cannabis is a major new consumer category.

But with two years of stellar stock market gains, dozens of new cannabis IPOs and billions raised from investors, has the market reached a saturation point?

In this report, we answer the question: Is the stock market value of the cannabis industry already higher than the future earnings that these companies can realistically justify?

The answer may surprise you.

First We Need to Define the Size of the Cannabis Market in the U.S. and Canada

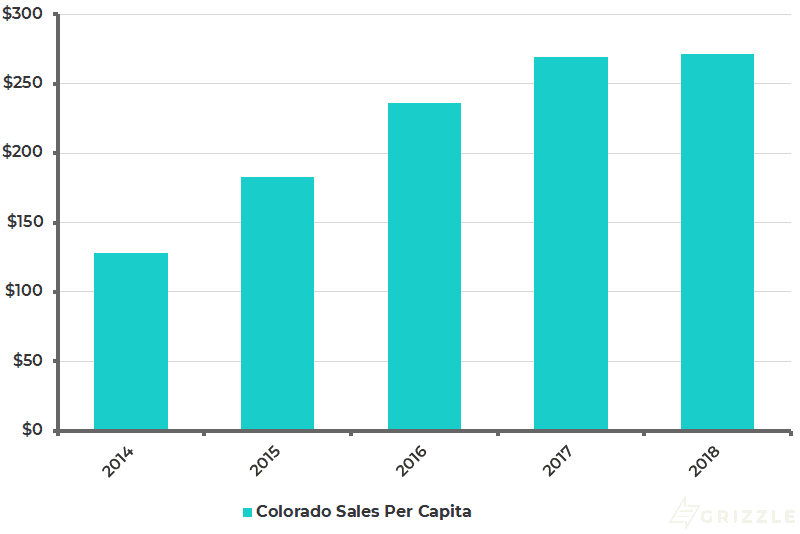

Looking at per capita, also called “per person”, spending in Colorado, the most mature cannabis market, consumers spent $273 on cannabis in 2018, basically flat from 2017.

Cannabis Spending Per Capita (Using Total Population)

Other states spend less, but are showing faster growth, so for an alternate estimate we use $220 of annual spending per person which accounts for further potential declines in retail prices.

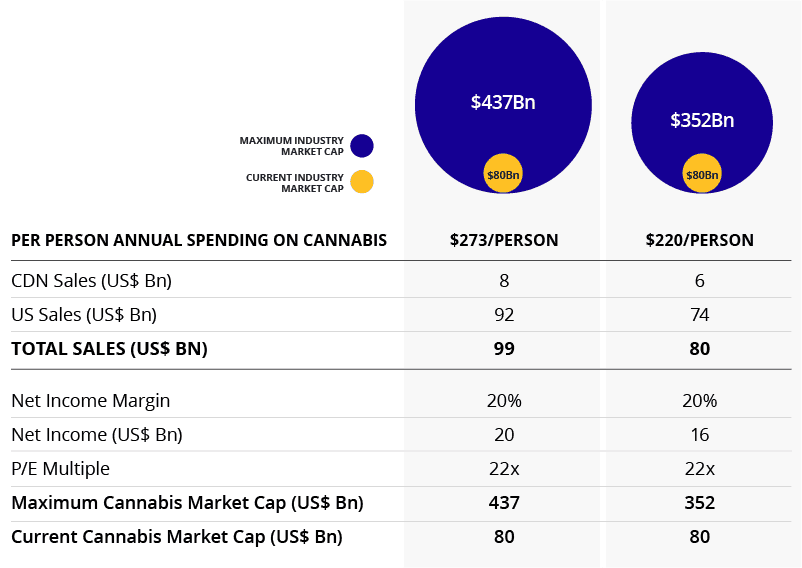

[su_panel background=”#150093″ color=”#ffffff” border=”0px solid #cccccc”]Applying these two scenarios to the entire population of the U.S. and Canada (372 million people by 2021), total cannabis sales will be $80-$100 billion under a full legalization scenario.[/su_panel]$100 billion of sales from the U.S. and Canada is in the ballpark of other estimates we have seen calling for $150 billion of global sales later next decade.

Why Colorado?

The reason we think Colorado has the best data for this exercise is threefold:

- Colorado is a full five years into legalization and is the most mature recreational cannabis market.

- Most product categories and formulations are unrestricted.

- The black market has largely been marginalized and is only hanging on by exporting illicit supply to other states where pot is still illegal.

Colorado helps us understand the two major factors driving the change in per capita spending, number of customers, and the price of cannabis.

We explore the data below to see how both of these factors will likely behave as Canada and the rest of the U.S. cannabis market matures.

Number of Legal Customers Grows Rapidly After Legalization

The legal cannabis market is benefitting from a rapidly growing customer base as consumers drop their illegal dealer and start buying from the local retailer.

As consumers convert from the black market to legal, the percentage of the population who consume legal cannabis will naturally go up and with it per person legal cannabis sales.

We can see this in Colorado state data.

Legal sales more than doubled from 2015 to 2017, while at the same time inventories shrunk.

We know consumers aren’t doubling their marijuana use so this data tells us the number of legal customers is growing, pushing out the black market.

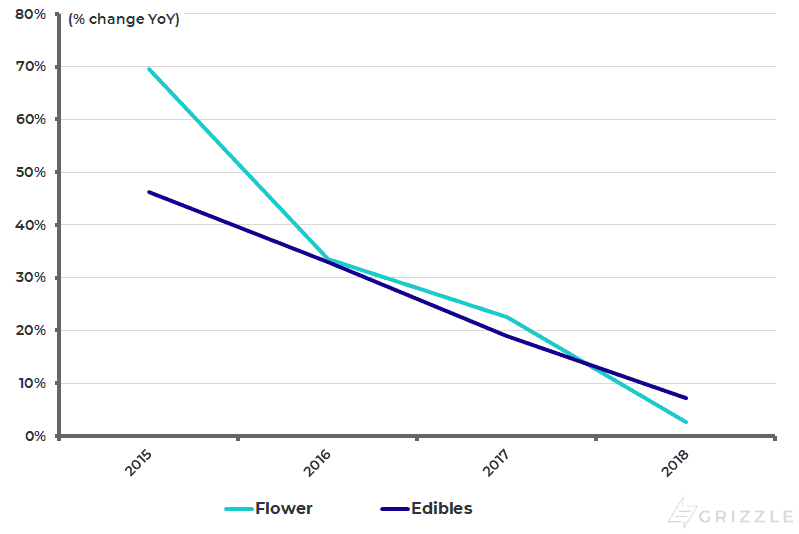

Colorado Cannabis Market Data 2015-2017

We can also see that demand growth for flower and edibles was only 2% and 8%, respectively, in 2018, telling us the Colorado legal market has largely matured or at least reached equilibrium with the black market.

Year-Over-Year Growth in Volumes

On the Flip Side, Retail Prices are Falling

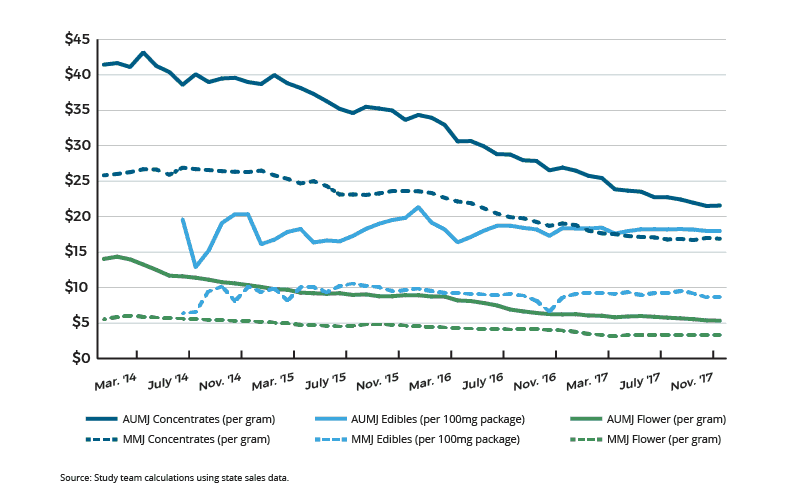

While a growing number of legal customers is great news for cannabis spending, the consistent fall in retail prices is offsetting some of the positive impacts a growing customer base has on per capita spending.

What is very interesting from our Colorado data is even as consumers buy more higher-margin edibles and concentrates, likely in the form of vape pens, the blended price of all of these products continues to fall.

Price per Serving of THC (10 mg)

Market prices for edibles look to be holding up better than any other product category, but interestingly consumer demand for edibles has basically flatlined in Colorado.

This is definitely a trend to watch to see if it repeats in Canada and other states that allow edibles.

Consumer Product Preference is Changing Over Time

This data goes against current investor thinking that as consumers transition from smoking dried flower to more expensive but convenient concentrates and edibles, the industry will see increasing revenue per gram and margins.

This just isn’t happening in Colorado.

Instead, the market is becoming more competitive as it matures.

As producers become more efficient and bring down their production costs, retail prices are falling to account for these lower costs.

Consumers are already accustomed to paying less, yet companies continue cutting prices in a bid to maintain and grow market share in a very competitive industry.

So How Much Stock Market Value can $100 Billion in Sales Support

At the end of the day, the cannabis industry needs to justify its lofty valuations with honest to goodness cashflow.

Using some educated assumptions about profitability and demand we were able to back into the ultimate market value of the U.S. and Canadian cannabis stocks that can be supported by flesh-and-blood cannabis consumers.

An industry generating $100 billion of sales should be able to support a stock market capitalization of $350-$450 billion.

The current market cap of all cannabis stocks in North America is only $80 billion.

The good news for investors and corporations is that there is much more revenue and stock market value to play for.

The cannabis industry is only in the second inning of growth, to use a baseball reference.

Potential Stock Market Size of the Cannabis Industry

The Cannabis Sector is Just Getting Started

Cannabis investors should feel confident there is more than enough industry growth ahead to support rising market caps and stock prices.

There is still a huge market waiting to be carved up and Grizzle estimates a clear winner is still at least 5 years away from being determined.

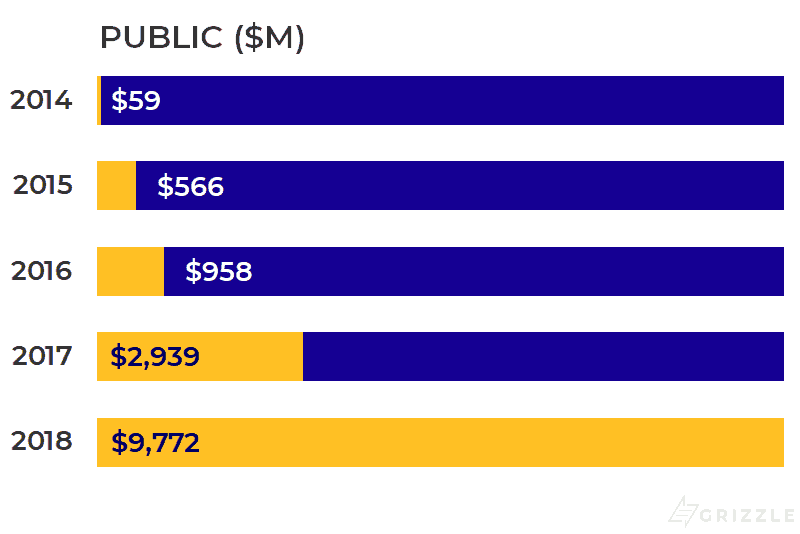

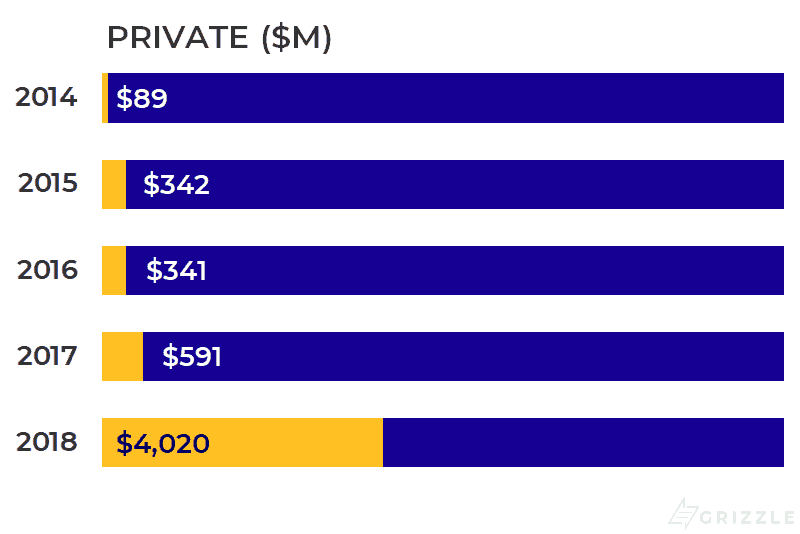

In 2018 the industry raised $13.5 billion from both the public and private markets — four times more than in 2017.

At this rate, 2019 will see $54 billion of value added to stocks from fundraising alone, a 70% increase to the industry’s market cap.

$54 billion of new fundraising may sound like a lot, but it would represent only 13% of equity and high yield debt raised on U.S. and Canadian exchanges in 2018.

At this pace, as long as capital markets stay open, the cannabis industry could reach a market saturation point in only 5-6 years.

This still leaves plenty of time for companies to ride the fastest growing consumer category in the world to big revenue gains over the half-decade.

Cannabis Industry Cash Raised

Totals for 2018 through December 14. Source: Viridian Capital Advisors, Fortune

How to Make Money in Marijuana Stocks

Investors can make money in this market two ways:

- Own the companies with hit products or a demonstrated intellectual property advantage as they will eventually be acquired by larger competitors.

- Own the future leaders who can not only thrive in a fast-growing market but can maintain their market share and growth rate through acquisitions once the cannabis market goes ex-growth.

Separating the winners from the losers is easier said than done, but investors can at least invest with confidence knowing the cannabis capital markets have many years of hyper-growth ahead of them.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.