Sometimes it is important to monitor alternative narratives and, like any good trader, not to be rigidly stuck to any specific view.

The focus of this writer as regards the state of the American economy in recent quarters has been on the considerable lags in the impact of monetary tightening in this cycle.

This means the full impact of the tightening has not yet been felt.

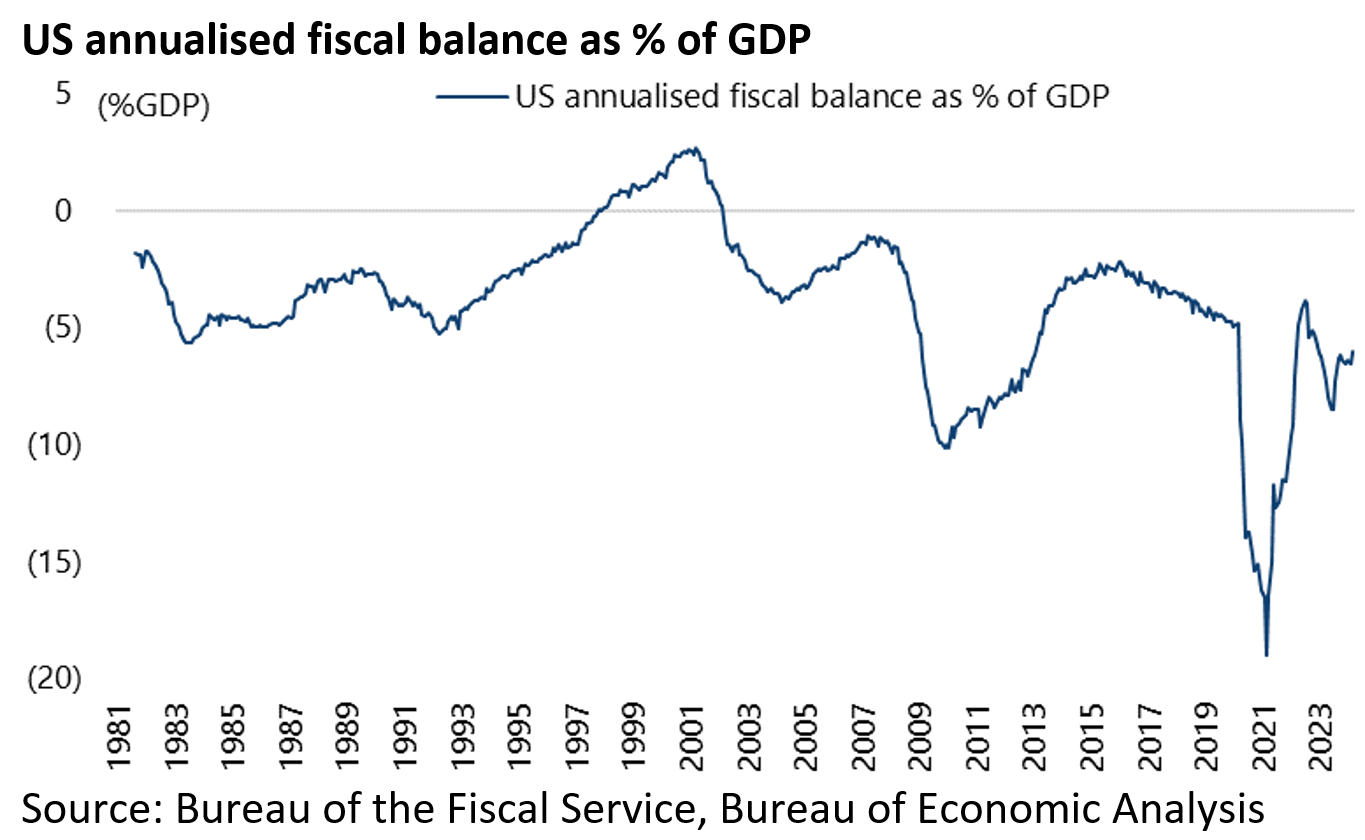

The other issue, of course, has been the undoubtedly near-term stimulatory impact of America’s unexpected large fiscal deficits.

The deficit is still running at an annualized 6% of GDP.

The above points still apply.

But recent data also means that the current reality is that financial markets have begun to question the prevailing soft-landing consensus on the view that there may be no landing at all.

Such an outcome would be equity bullish but Treasury bond bearish since it implies higher nominal GDP growth.

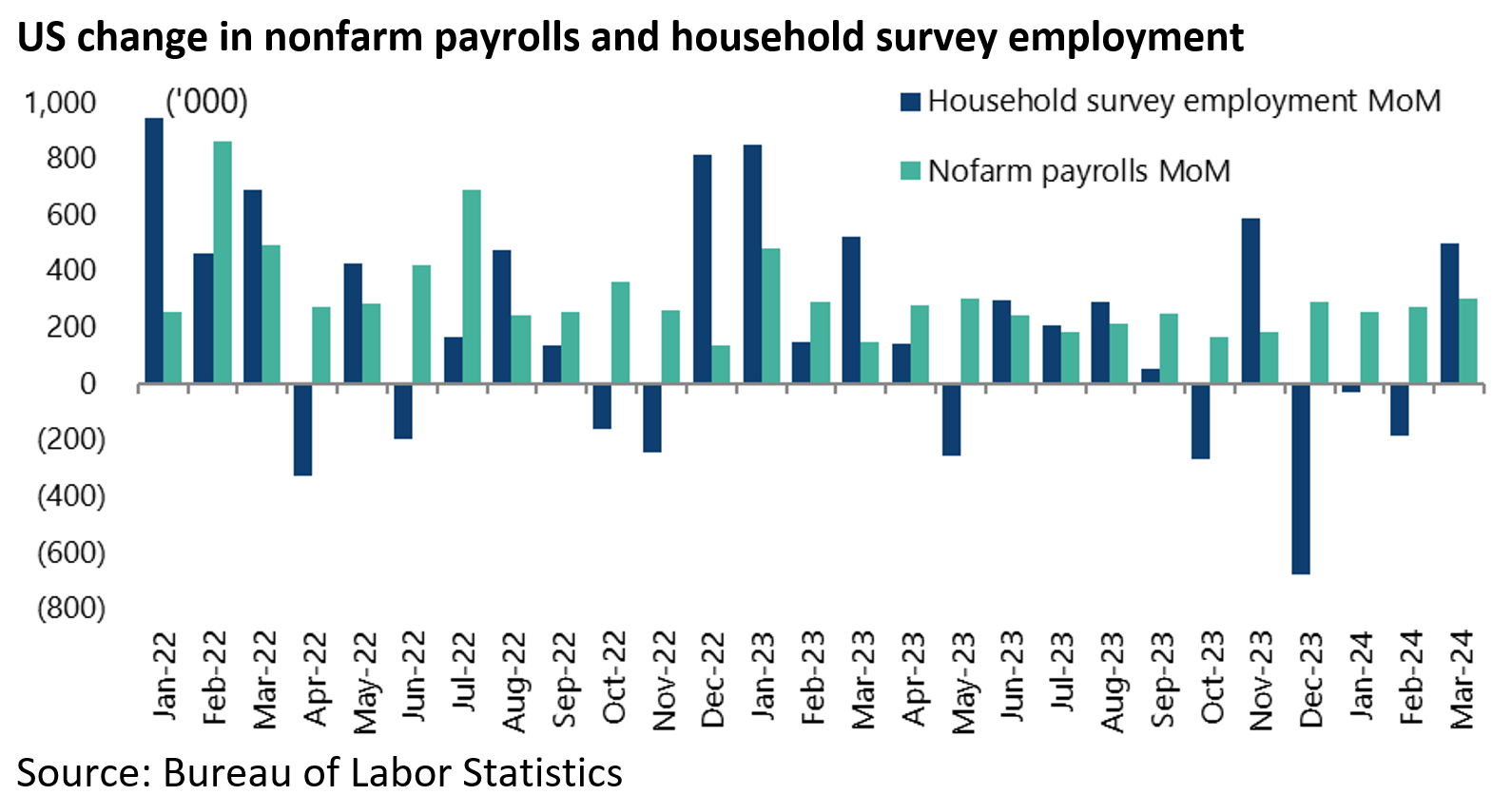

US nonfarm payrolls increased by 303,000 in March, well above consensus expectations of 214,000 and the 270,000 increase in February, while the increase in the previous two months was revised up by 22,000.

Household survey employment also increased by 498,000 in March following a 898,000 decline in the previous three months.

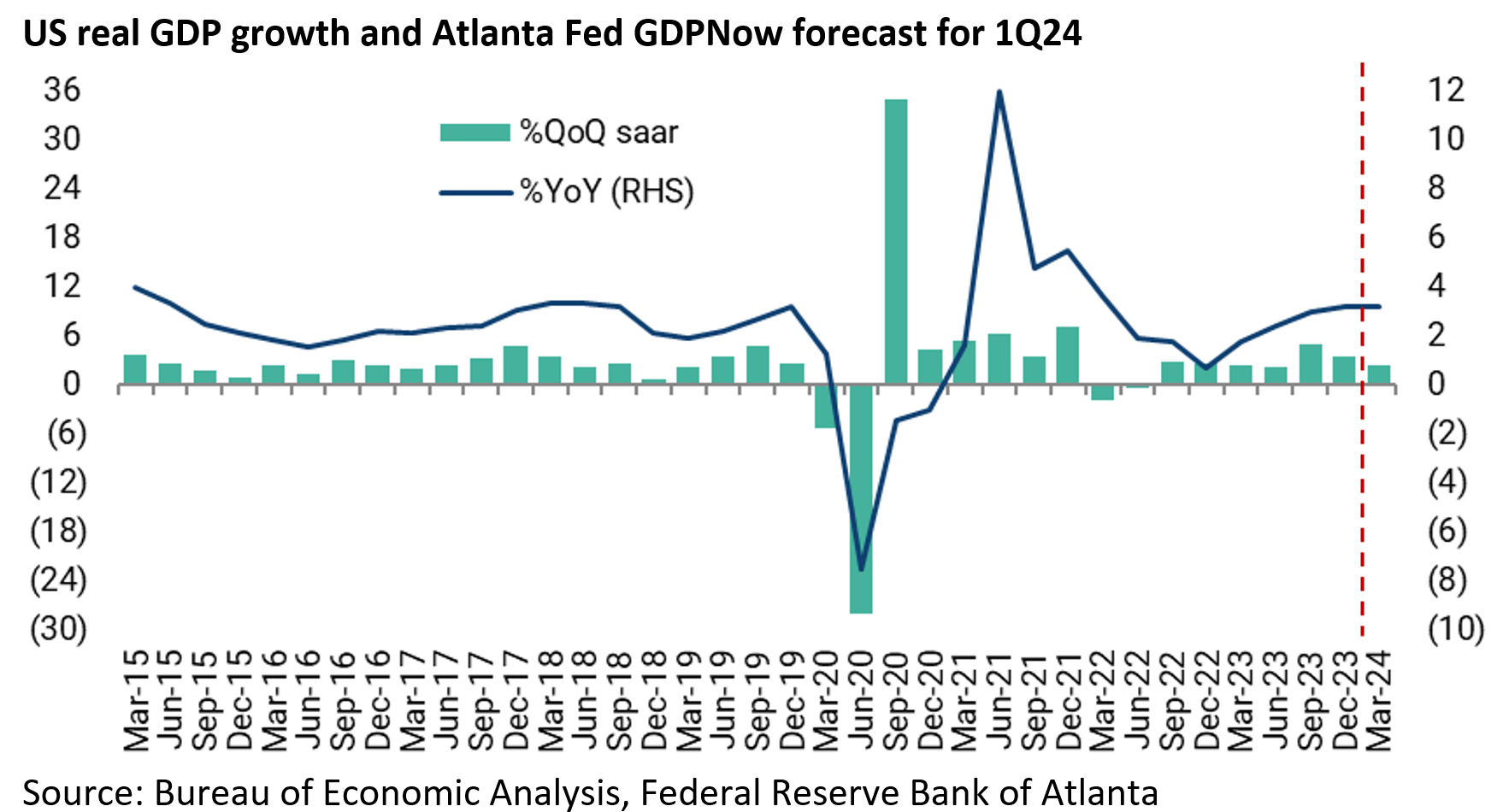

Meanwhile the Atlanta Fed GDPNow model is now projecting a US economy growing at 3.2% YoY in the current quarter, up from 3.1% YoY in 4Q23.

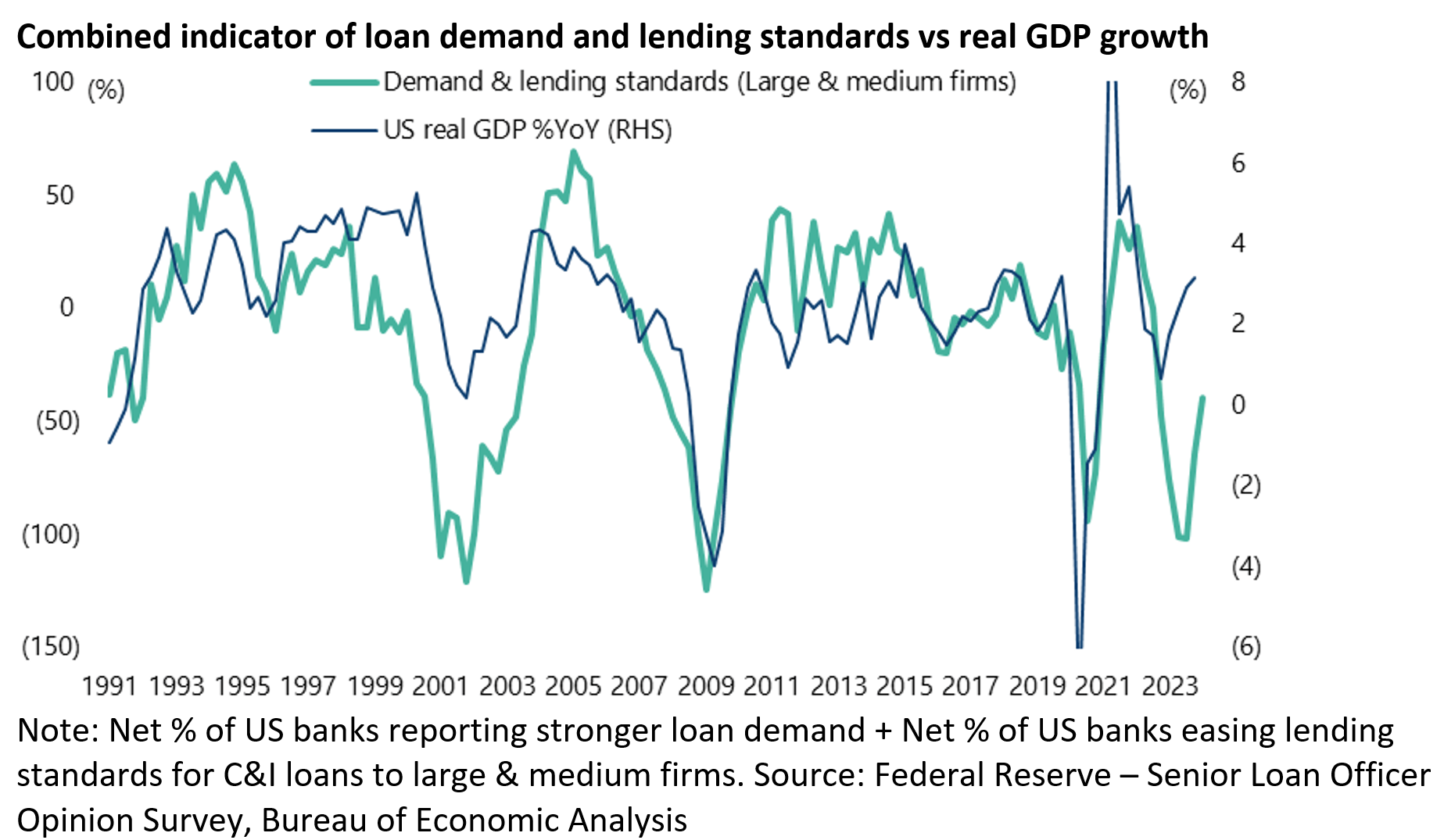

It is also the case that the last Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) released in early February showed a decline in the net percentage of banks tightening lending standards.

Thus, a net 20.6% of US banks tightened lending standards for all loans over the past three months, down from 30.6% in the October survey and 42% in April 2023.

The next survey is due in early May.

As discussed here before (see With bank lending on the decline, why aren’t we in a recession already?, 24 December 2023), the correlation between the combined indicator of lending standards and loan demand in the so-called SLOOS (Senior Loan Officer Opinion Survey) and the state of the US economy has so far broken down in this cycle as shown in the chart below.

Inflation Remains an Issue

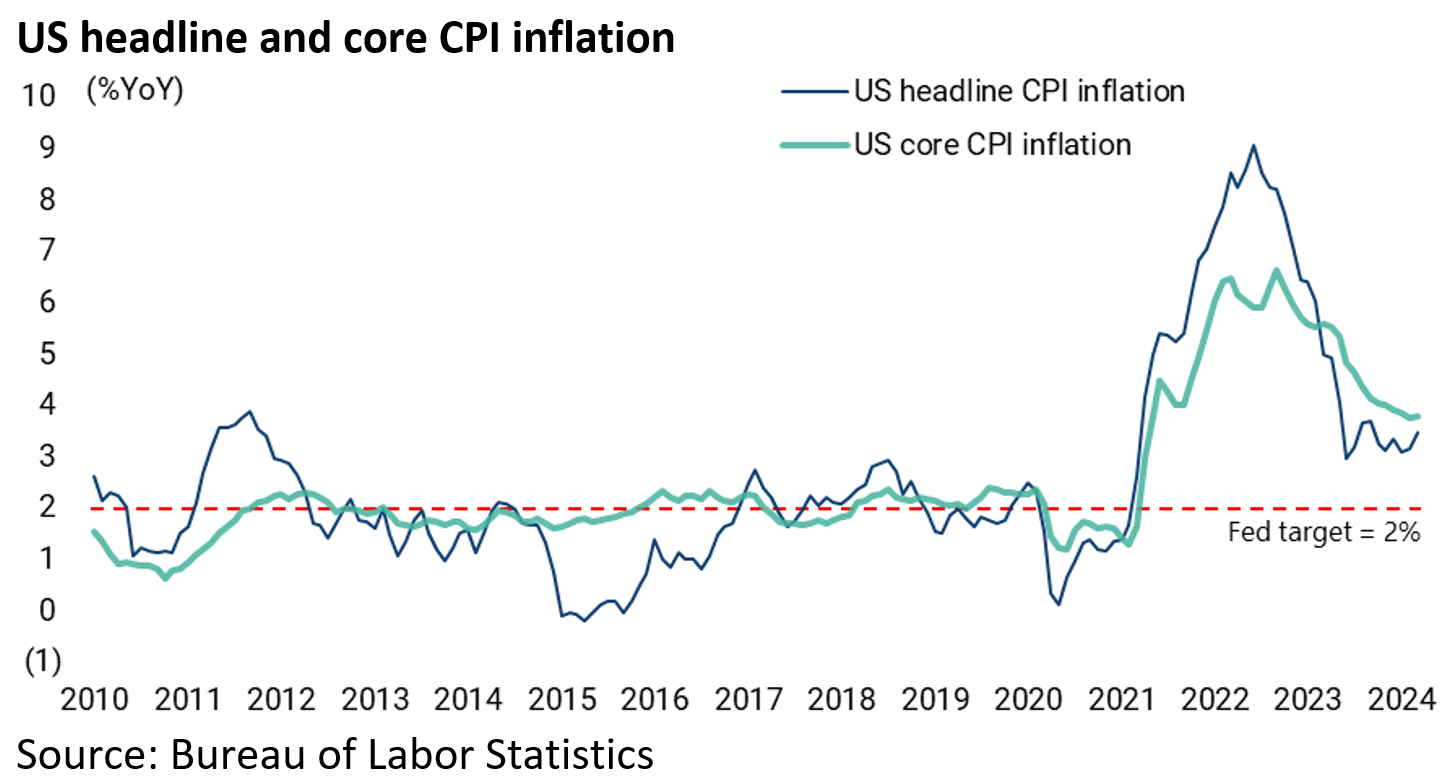

Then there is the inflation issue which markets have been reminded of again last week with US CPI in March coming in above expectations for the third month in a row.

Headline CPI rose by 0.4% MoM and 3.5% YoY in March, compared with consensus expectations of 0.3% MoM and 3.4% YoY.

While core CPI increased by 0.4% MoM and 3.8% YoY, above consensus expectations of 0.3% MoM and 3.7% YoY.

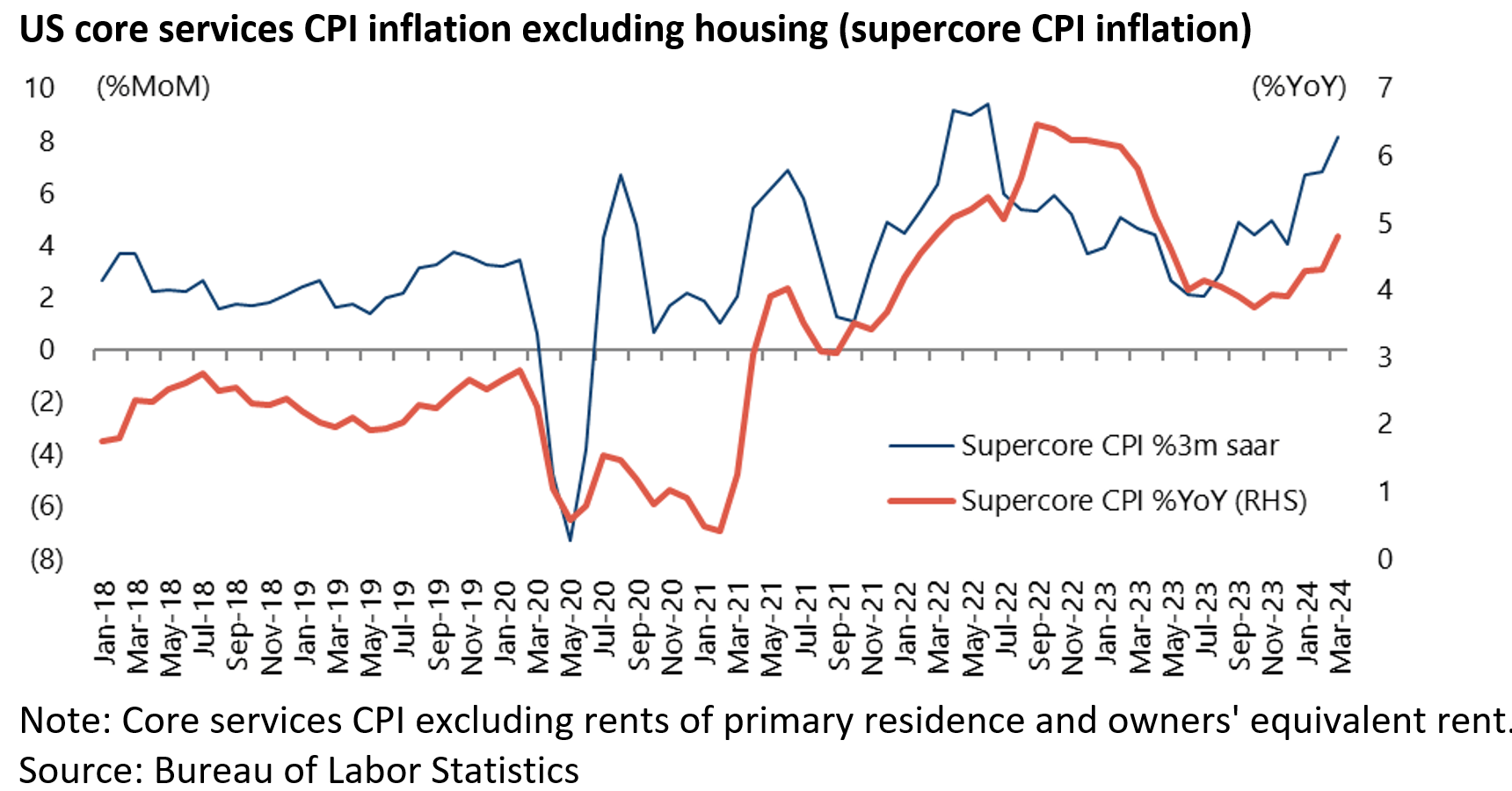

Meanwhile, core services CPI inflation, excluding housing, rose from 4.3% YoY in February to 4.8% YoY in March, the highest level in 11 months, and is up an annualised 8.2% over the past three months.

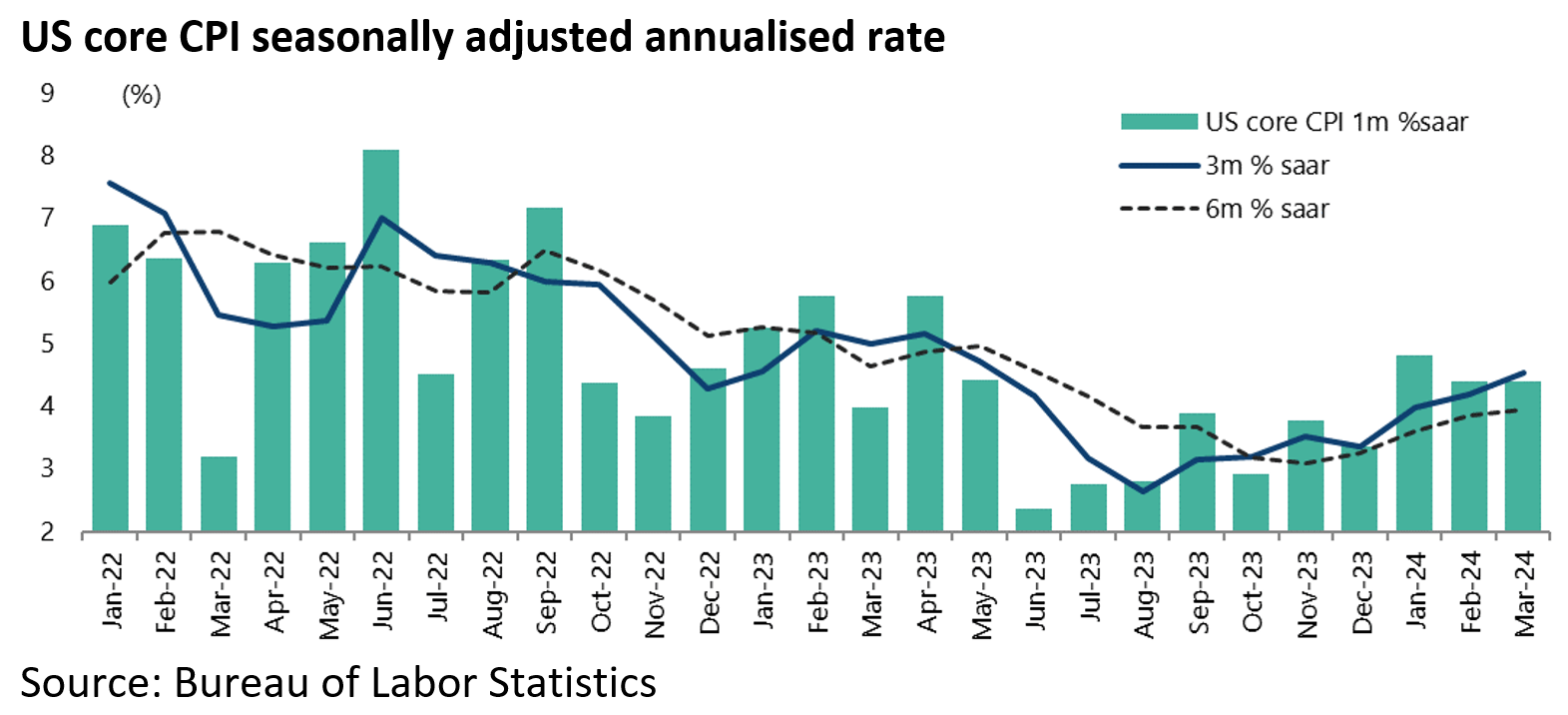

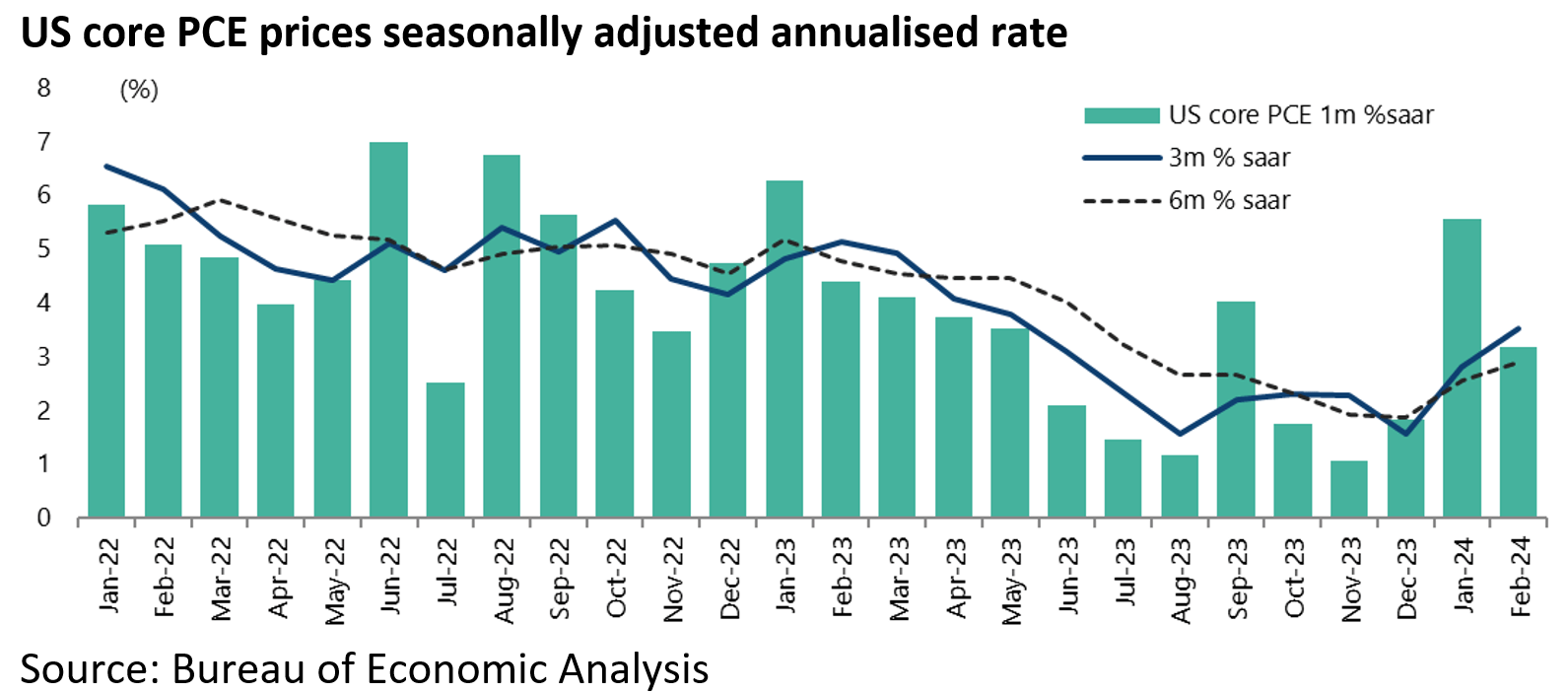

It is interesting to note that core CPI is now running at an annualised 3.9-4.5% over the past one, three and six months.

This compares with the annualised growth of 2.9-3.5% in core PCE inflation over the same periods.

This raises again the issue of which inflation rate the Fed is targeting.

In this respect, the question is whether core PCE is going to rise towards the core CPI level or the other way round.

At the moment the data is suggesting the former, not the latter, outcome.

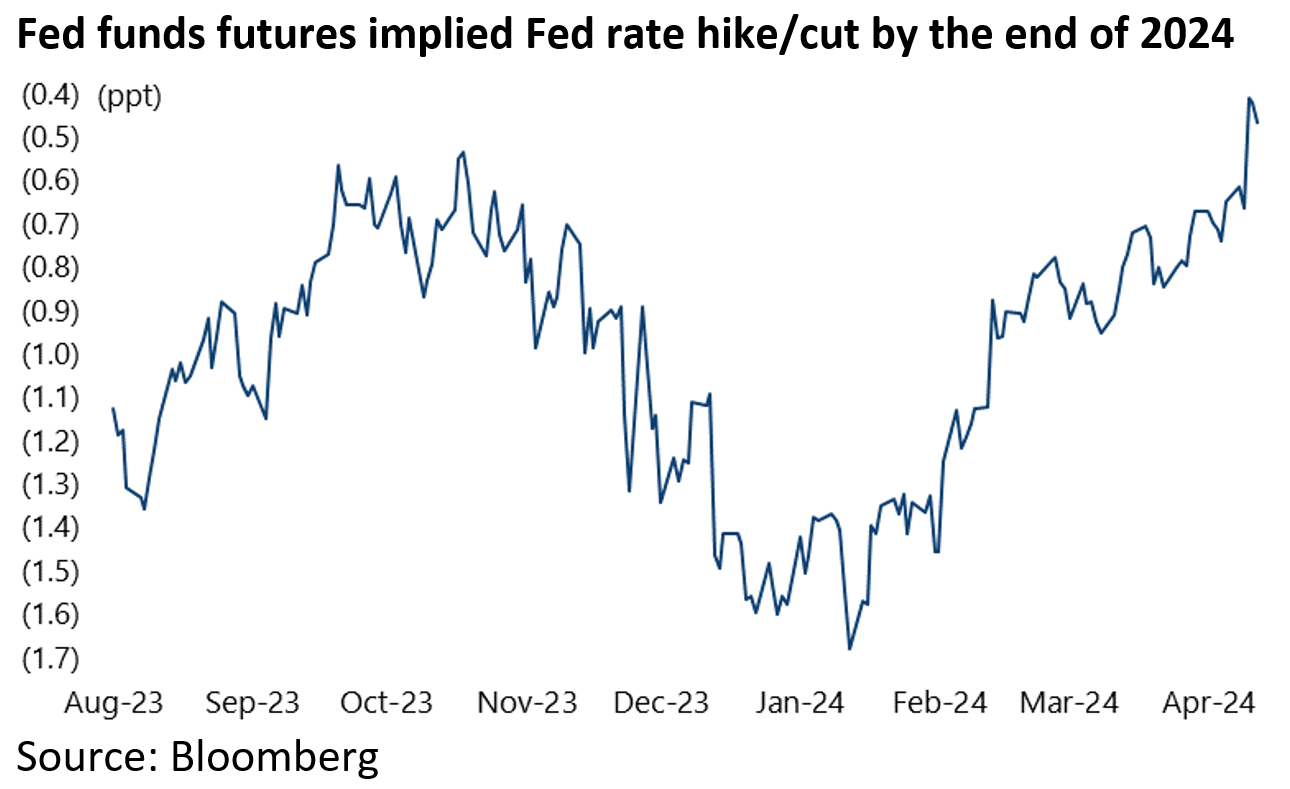

The result of the recent data is that money markets are now expecting only 46bp of Fed rate cuts in 2024 as opposed to 150bp the day after Jerome Powell engaged in his perceived pivot at the December FOMC meeting.

It is also the case that the first cut has now been pushed back to September which is a bit late for the Fed from the standpoint of the presidential election cycle.

For if the Fed starts cutting in the months immediately preceding the November poll it is likely to be accused of being political by the probable Republican presidential candidate Donald Trump.

Still a “no landing at all outcome” would make this a possibility.

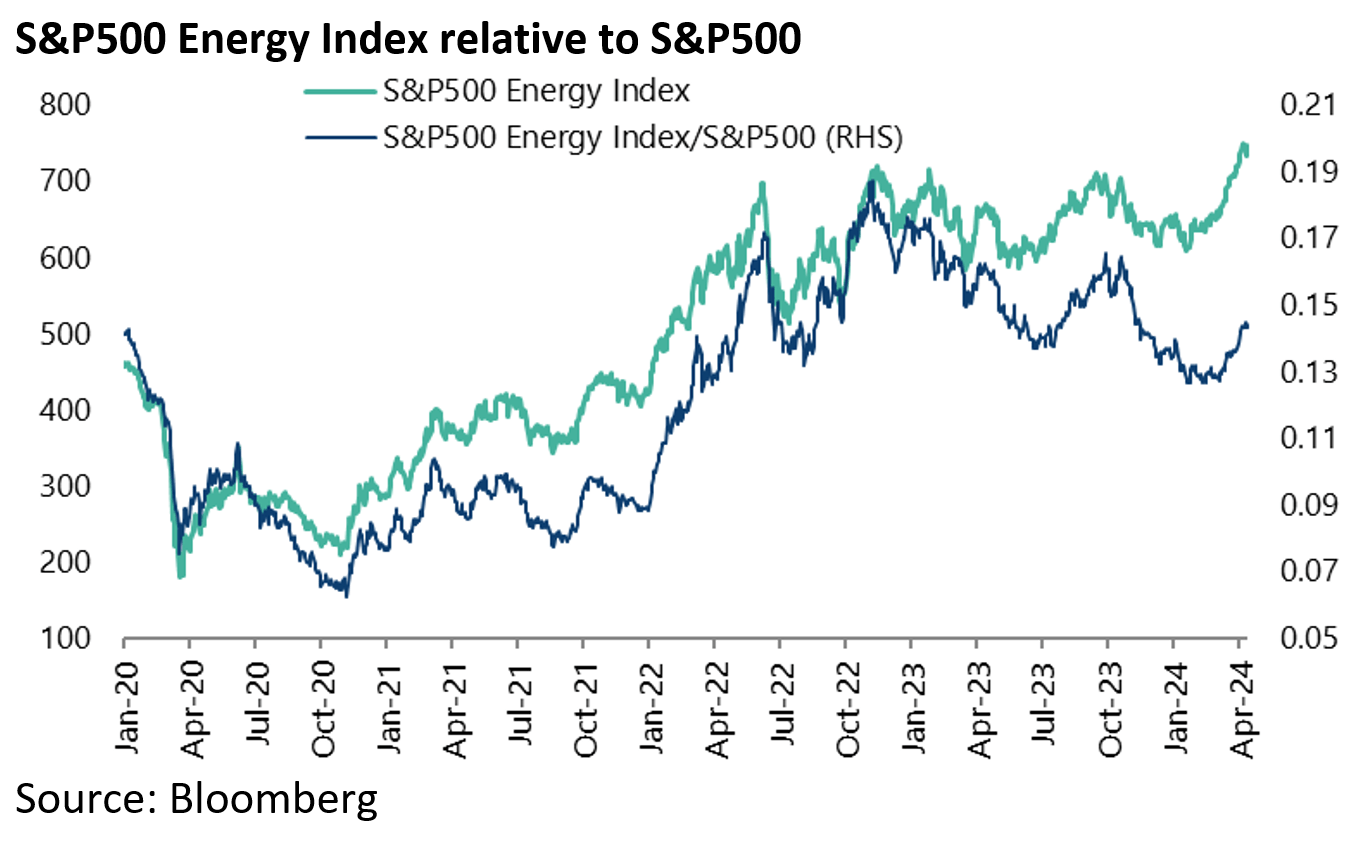

A No Landing Scenario Means Higher Oil Prices

The other risk of such an outcome is a further rise in the price of oil.

Brent crude is up 25% since mid-December which will have definitely impacted headline inflation data.

On this point, the S&P500 Energy Index has risen by 22% since bottoming on 19 January and has outperformed the S&P500 by 13% since 9 February

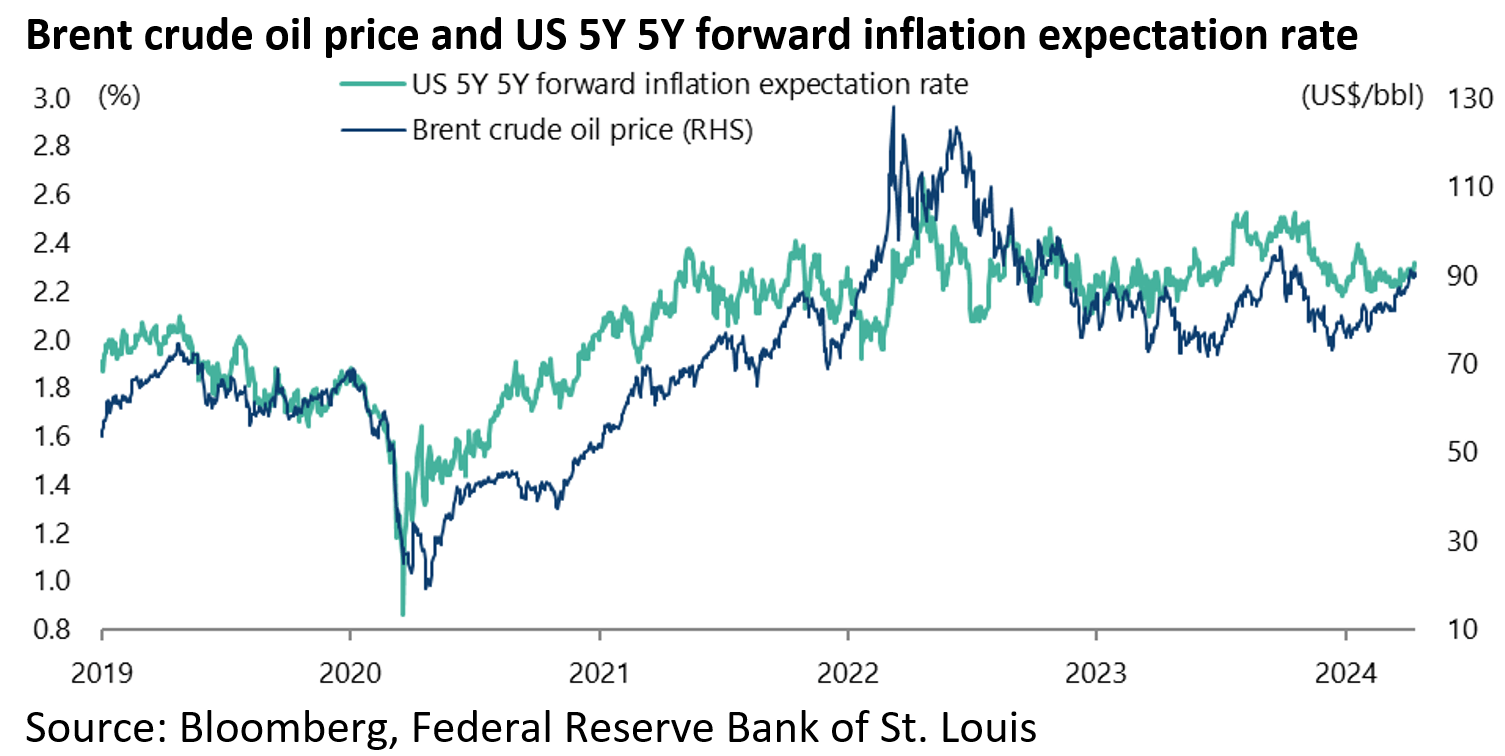

Still the positive point from the Fed’s standpoint is that US five-year five-year forward inflation expectations remain for now well anchored at 2.31%.

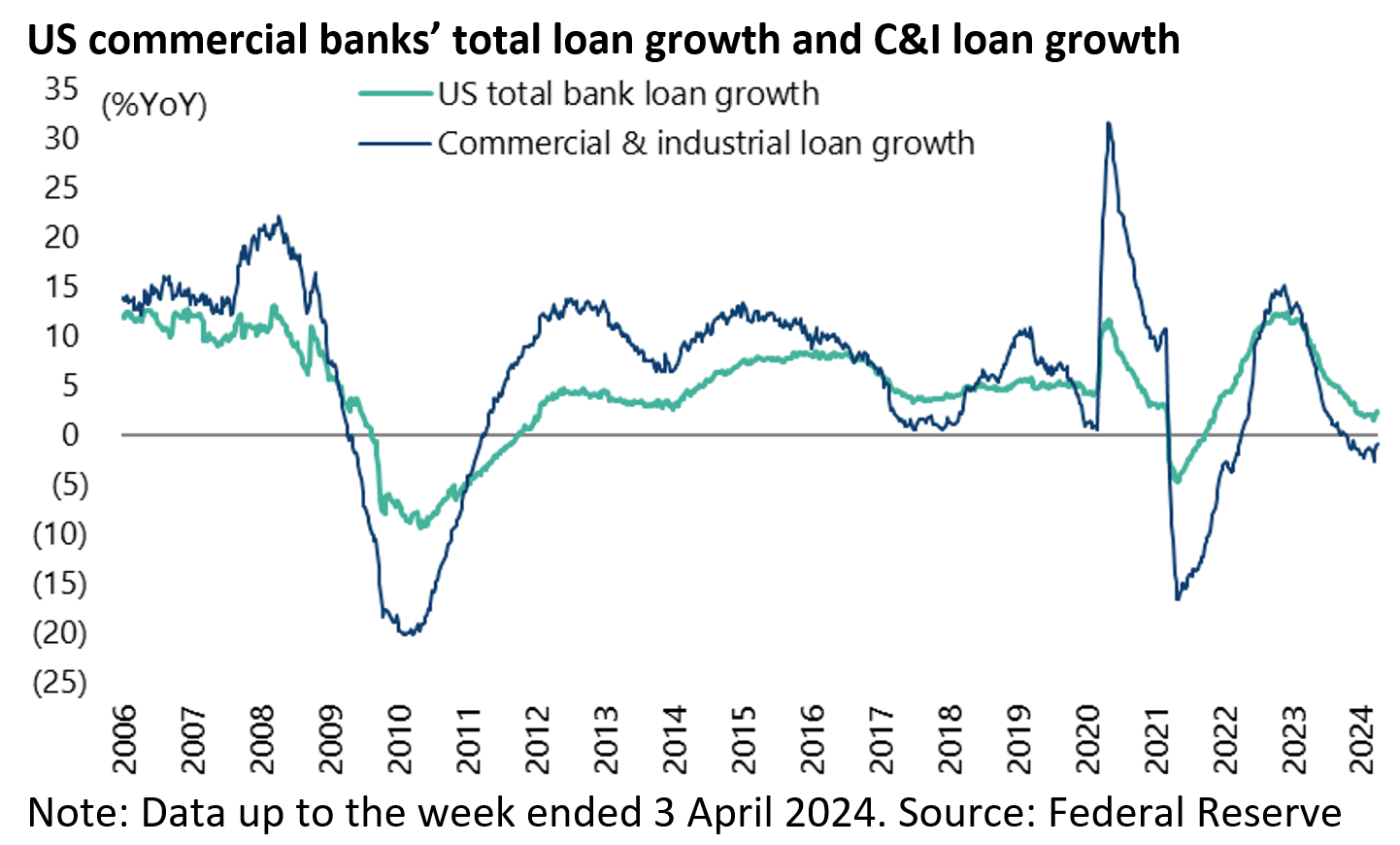

Why is Slow Commercial Bank Lending Having No Impact on the Economy?

Meanwhile it remains strange that the downturn in US commercial bank lending has not yet had the negative impact on the economy that would normally be expected.

For the record, commercial bank loan growth has slowed from 12.4% YoY in December 2022 to 2.2% YoY in the week ended 3 April.

While commercial and industrial loan growth has declined from 15.1% YoY in November 2022 to a 1.0% YoY decline in early April.

One reason, aside from fiscal easing, remains the continuing flow of funds into the private credit asset class.

The interesting point here is that the private credit boom has continued even as investors in private equity funds, such as public pension funds, have turned more risk averse towards private equity as an asset class as they are already, reportedly, over allocated to it.

Yet the average discount on a US private equity fund, for those “locked up” investors or limited partners looking to sell in the secondary market, apparently narrowed from 19% at the end of 2022 to 15% at the end of last year.

The reason for the narrowing in the discount was the emergence of a new buyer in the form of so-called secondary funds, many of them raised by prominent private equity franchises.

Private Equity Loading up on More Credit Since December

Meanwhile it is interesting to note that private equity firms were quick to take advantage of the lower borrowing costs courtesy of Fed chairman Jerome Powell’s perceived pivot in the December FOMC meeting to load more debt on to their portfolio companies to pay dividends to themselves and their investors.

Thus, corporate borrowers sold US$8.1bn of junk-rated US loans in January, more than six times the December level and the highest monthly figure in more than two years.

Most of these loans were issued by companies backed by private equity firms, according to PitchBook (see Financial Times article: “Private equity firms boost payouts by piling on debt as borrowing costs ease”, 6 February 2024).

The above activity, known somewhat bizarrely as “dividend recapitalisations”, is a consequence of the fact that a sluggish market for initial public offerings in the past two years in the US has made it harder for private equity funds to exit investments.

So these dividend payments are a way of returning some cash to investors if not their entire capital.

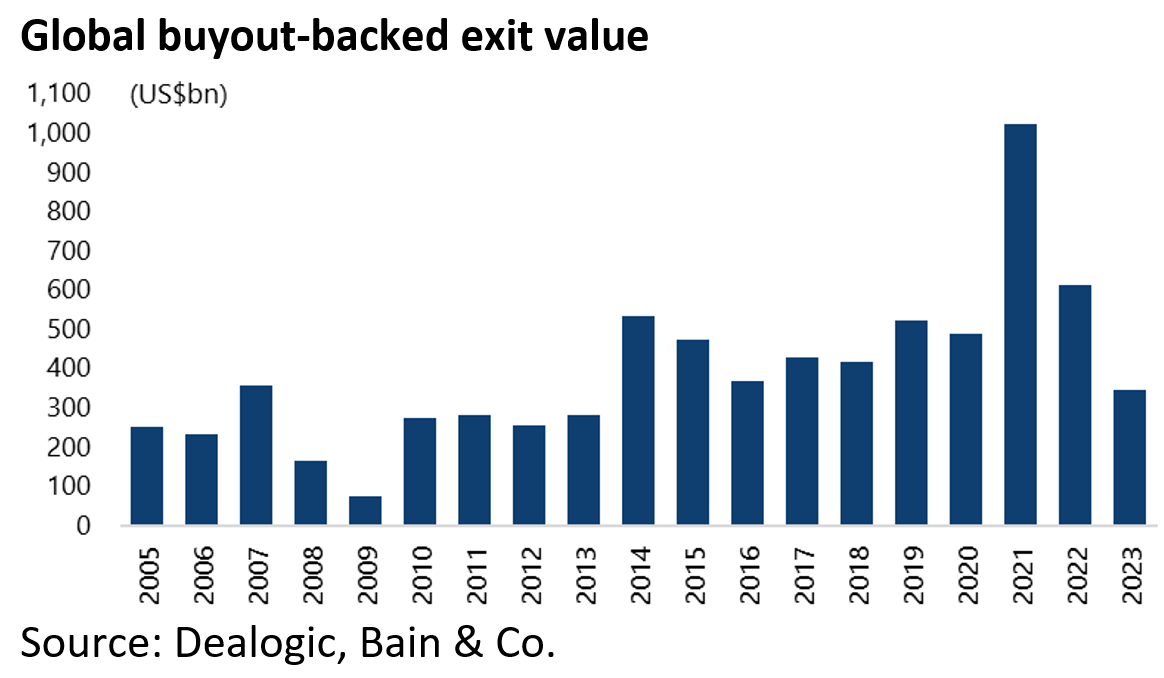

On this subject, a recent recommended Bain report (see Bain & Co. report: “Global Private Equity Report 2024”, 11 March 2024) estimated that private equity companies are sitting on 28,000 unsold companies globally worth a hoped for more than US$3tn.

Last year the combined value of companies sold by the PE industry privately or on public markets fell by 44% to a decade low of US$345bn, down 66% from the peak reached in 2021, according to the same report..

There is no doubting the formidable financial engineering skills of the private equity industry, in terms of navigating the challenge to its business model posed by the 525bp increase in the federal funds rate in this monetary tightening cycle.

After all, this is an industry which boomed in the zero interest rate era.

This is why the longer it takes for monetary easing to commence, the bigger the potential problem for this industry.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.