Fed to Remain Dovish: Yield Curve Control

There was an interesting speech made last month by Federal Reserve governor Lael Brainard, one of the candidates to be Treasury Secretary in the Biden administration (see Financial Times article: “Fed official fears disparities will slow recovery”, 22 October 2020).

The most interesting comment attributed to Brainard in the article was that she said that it would be important for the Fed to remain dovish even after any “lift off” in interest rates.

This would again suggest at least implicit support for yield curve control since, otherwise, rising bond yields could threaten economic recovery. The speech given to the annual online conference of the Society of Professional Economists was also important in its stress on the “uneven” nature of the recovery.

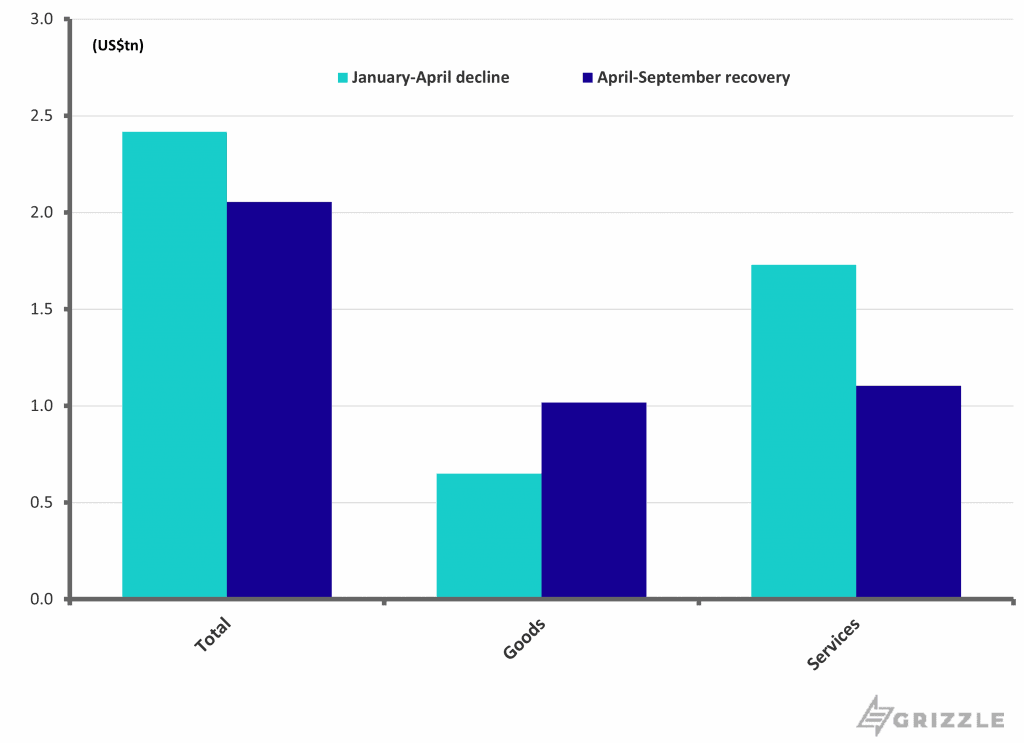

The Fed governor noted that while overall consumer spending has recovered 75% of its lockdown-triggered decline, consumer spending on services had recovered by only 60% as of August (September data shows that overall consumption recovered 85% while consumer spending on services had recovered by only 64%, see following chart).

US Real Personal Consumption: January-April decline and April-September Recovery

The speech also highlighted the uneven impact on Main Street. This is important because ever since the bailout of the Wall Street fat cats in 2008 and the resulting unleashing of asset price inflation via quanto easing in late 2008, the Fed has been vulnerable to accusations that it has undermined the moral authority of America’s capitalist system, accusations this writer agrees with.

Brainard’s speech shows a healthy understanding, not always shared by those on her side of the political argument, that lockdowns have inflicted much more damage on blue-collar workers and those working in the real economy than those who are fortunate enough to be able to work remotely. In a bid to address these disparities, she stated that the Fed had held three meetings over the past month with community groups, “mission-oriented lenders” and representatives of frontline workers. This certainly makes sense from a public relations perspective.

Still to a large extent, unfortunately, the damage has already been done. Brainard contrasts the starkly different conditions facing large businesses with access to the capital markets and those now facing small businesses.

Corporates Issue Record Amount of Debt

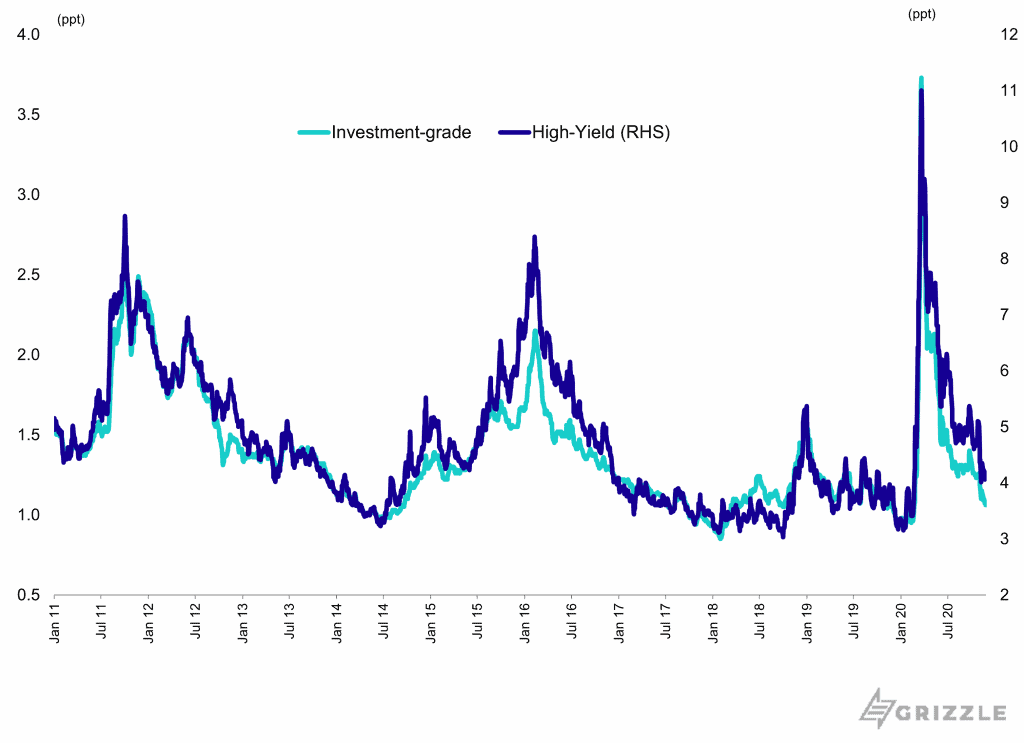

The big corporates have clearly benefitted from the Fed’s historic decision to buy investment-grade bonds which has allowed the whole of the fixed income market effectively to front run the Fed, as can be seen in the dramatic contraction of spreads (see following chart) since Jerome Powell made that announcement in March and the related surge in corporate bond issuance. US corporate bond issuance rose by 66% YoY to a record US$2.07tn in the first ten months of 2020 (see following chart).

US Corporate Bond Yield Spreads

US Corporate Bond Issuance

Tighten Credit for Small Businesses

As for small businesses, the Paycheck Protection Programme (PPP) clearly provided a critical lifeline but that has now ended and credit availability is tightening.

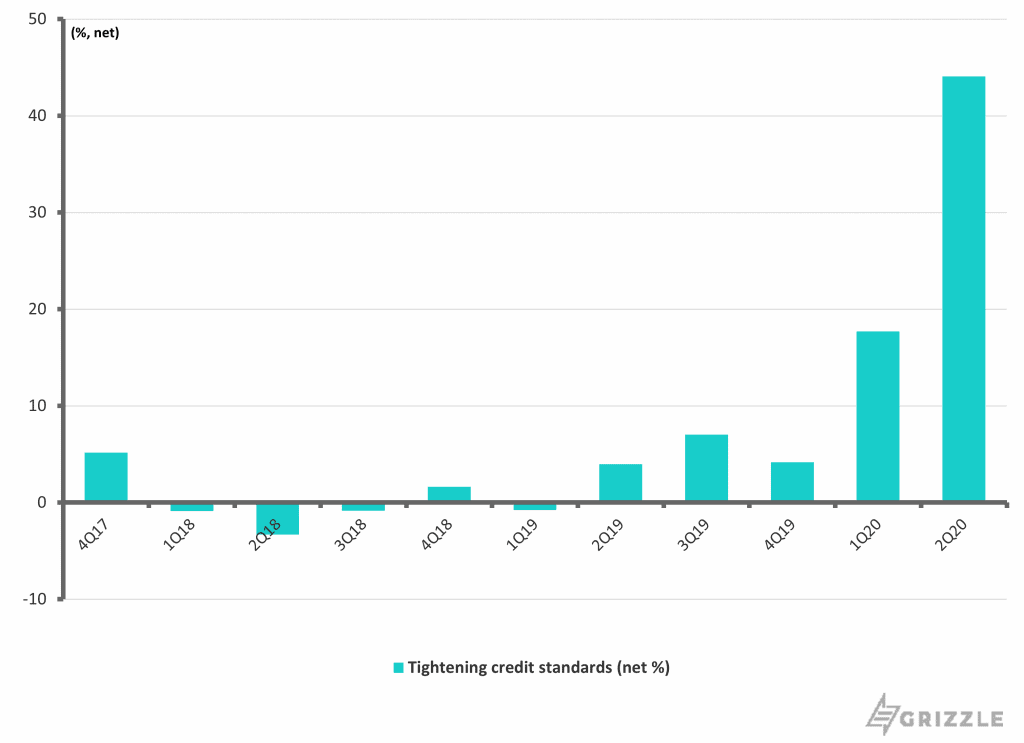

Driven primarily by PPP-related loans, originations of new small business commercial and industrial (C&I) loans in 2Q20 were more than nine times the size of those originated in the second quarter of last year, according to the Kansas City Fed’s Small Business Lending Survey released at the end of September.

But the same survey shows that credit standards are now tightening. A net 44% of respondents reported tightening credit standards in 2Q20, up from 18% in 1Q20 and 4% in 2Q19 (see following chart).

Small Business Lending Survey: Net % of banks reporting tightening credit standards

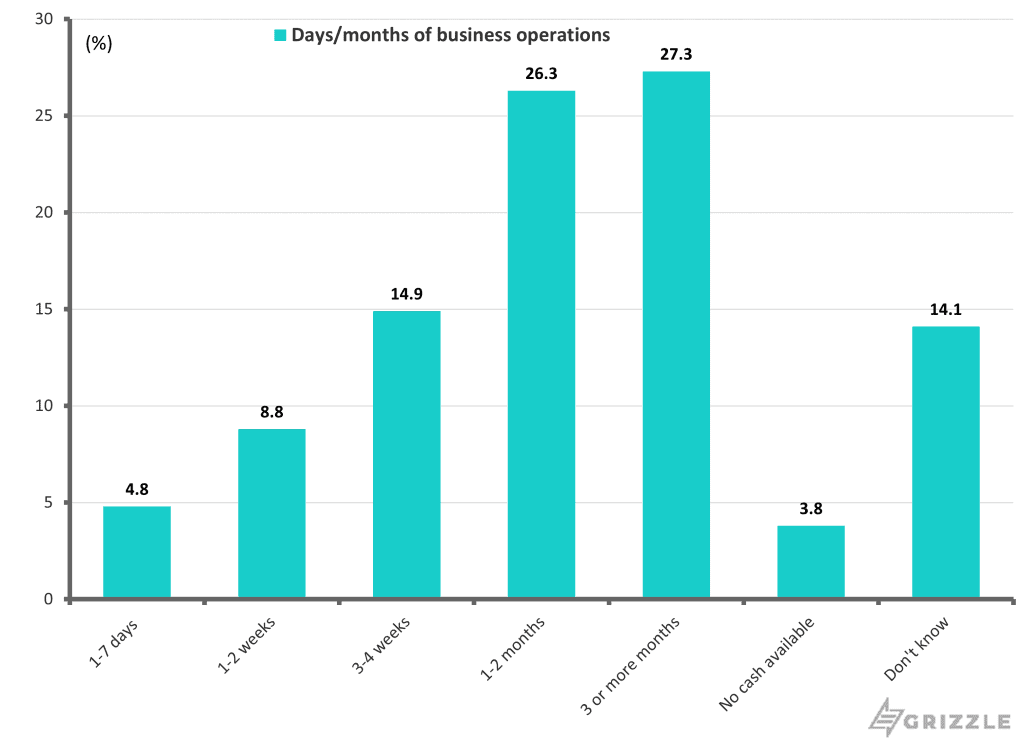

As for the evidence of growing fallout, Brainard cites a Census Bureau Small Business Pulse Survey from early October which reported that more than 30% of small businesses reported having one month or less of cash on hand. The results were the same from the latest survey released last week, see following chart.

She also cited recent research showing that the economy has suffered a 41% decline in Black business owners and a 32% decline in Hispanic business owners compared with a 22% overall decline (See NBER working paper: “The Impact of COVID-19 on Small Business Owners: Evidence of Early-Stage Losses from the April 2020 Current Population Survey” by Robert W. Fairlie, June 2020).

Small Business Pulse Survey: Current availability of cash on hand by days/months of business operations

Brainard is, therefore, right in concluding that the pandemic “is exacerbating existing disparities in labor market outcomes”.

The politically charged question going into the US presidential election was whether voters would blame the outcome on the perceived mismanagement of the pandemic or would they blame it on the unprecedented decision to lock down economies on account of the pandemic. The result of the presidential election suggests, by a narrow margin, that it was the former.

Returning to the more conventional Fed focus on inflation, Brainard notes that “while inflation may temporarily rise to or above 2% on a 12-month basis next year when the March and April price readings fall out of the 12-month calculation”, her baseline forecast is for it to remain “short of 2%” for the next few years.

She also stressed that, under the Fed’s new “flexible inflation averaging targeting” (FAIT) strategy, the Fed should aim to achieve inflation above 2% “for a time” to compensate for previous persistent shortfalls.

In this regard, the Fed governor and potential future Treasury Secretary noted that it was “important” to commit to a path of “lowering borrowing costs along the yield curve”. That again sounds to this writer like a willingness to resort to yield curve control, and the resulting financial repression.

All of the above also suggests that a Biden victory should be long-term bullish for gold and bitcoin and bearish for the US dollar.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.