Bottom Line

We firmly believe the decision by CEO Vic Neufeld to step aside is a big move in the right direction, as it presents Aphria a clean management slate that it obviously needs.

With the management cloud now out of the way, it allows the market to refocus on a company with the lowest growing costs in the industry and legitimate assets trading at a deep discount to peers — facts that Grizzle highlighted immediately after the publication of the short report.

Just as importantly, the short seller Gabriel Grego announced he is moving on to other short opportunities, implying that there is no ‘smoking gun’ remaining in his report.

Aphria should have their full rebuttal out by the end of January or early February.

We think Aphria is now ripe for an investment from a consumer company, not to mention the ongoing C$11/sh offer from Green Growth Brands.

Aphria trades for only $9/gram while recent equity stakes taken by consumer companies were done at more than $30/gram, valuing Aphria at $30/sh.

Aphria trades at an 85% discount to peers even though it will be the first licensed grower in Canada to reach full capacity in 2019 and has a similarly diversified global footprint to industry leader Canopy Growth.

Operationally, investors should be prepared for another 3-6 months of messy financials from all licensed producers.

Cost structures are ramping up to full scale faster than production and revenue, leading to higher cashflow deficits in the near term.

Aphria is ahead of peers in reaching profitability so could possibly show a shrinking EBITDA deficit as soon as the May reporting quarter.

Operational Overview

Like all of the other large producers, Aphria’s profitability adjusted to recreational pricing and growing costs increased as the company builds a larger workforce to handle its rapidly increasing capacity.

Aphria is also dealing with delays in Health Canada permitting and is pushing off construction for the next expansion phase of Broken Coast as they reconsider the design and the location of the facility.

Starting in the quarter that ends May 2019 Aphria should start to show much-improved financials and management mentioned on the conference call they should generate positive EBITDA 3 months after the receipt of all their production licenses in Canada.

The selling price per gram in the quarter was $6.36, down 15% from $7.47 last quarter. This was a much smaller decrease than the 45% decline HEXO reported. HEXO is the only other producer to report partial results from recreational sales so far.

Recreational pricing was $4.85/gram excluding excise taxes while medical pricing was $8.36/gram in the quarter.

The most important financial detail we noticed in the quarter was the very small cashflow deficit of only $1.8 million.

This means the company is very close to breaking even, an important milestone that will lead to less dilution for stockholders as the company moves closer to funding growth internally.

Aphria has enough cash to reach full capacity of 255,000 kg and will not need to issue any more shares unless they choose to embark on another large expansion project.

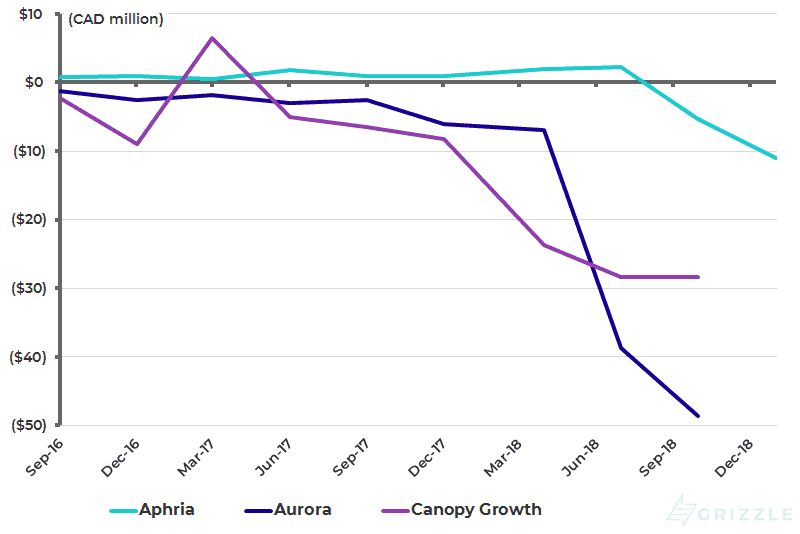

The chart below shows that Aphria’s EBITDA deficit is only a fraction of similar-sized peers Aurora Cannabis and Canopy Growth.

EBITDA by Quarter

Production and Inventory

In the quarter Aphria sold 13,600 kg on an annualized basis, up 91% over last quarter.

Sales only include a month and a half of recreational sales and will likely be closer to 21,000 kg annualized next quarter.

Production capacity is running at 35,000 kg annually and will ramp up to 255,000 kg by the middle of 2019.

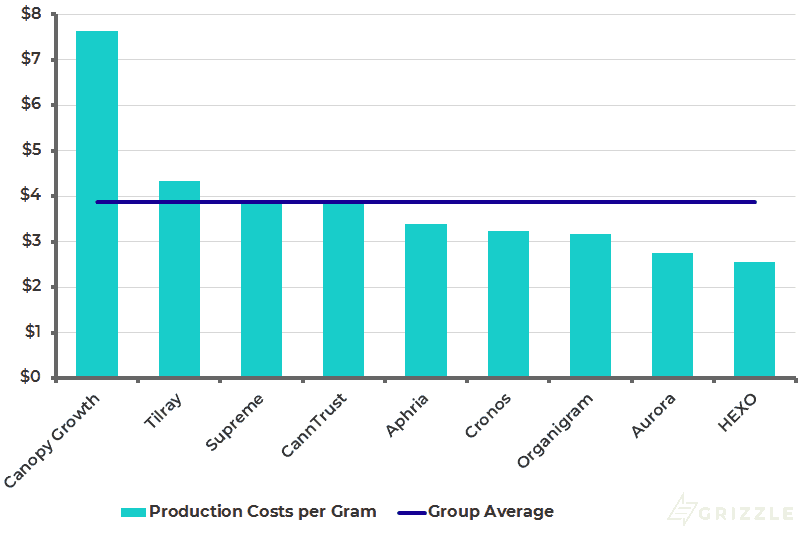

Production Costs Increase, but Will Return to Best in Class

Like all of the other producers, Aphria is seeing higher production costs per gram as it ramps up to full capacity.

Growing space is being repurposed as cloning rooms, decreasing current capacity but making it much quicker to ramp up once Health Canada approval for new grow rooms is received.

Production costs this quarter of $3.38/gram are middle of the pack, but once Aphria 1 and Aphria Diamond ramp up to full capacity of 255,000 kg a year, the company will return to being the lowest cost producer in Canada.

Being the lowest cost producer means that Aphria should be the most profitable licensed producer as the legal market evolves.

Per Gram Production Costs by Company

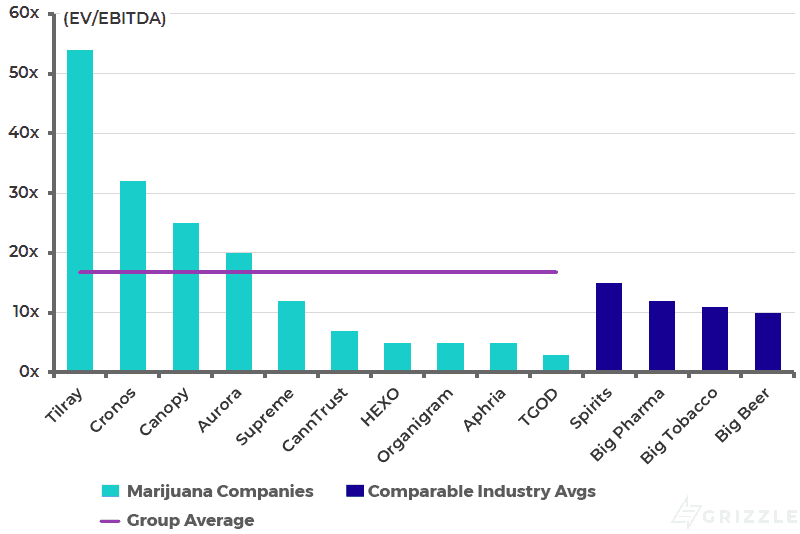

Aphria Continues to Trade at a Huge Discount to Peers Aurora Canopy Growth, Tilray, and Cronos

Even though Aphria will match or exceed the output of the two largest peers in the industry in 2019, the company trades at over an 85% discount to peers.

The market will eventually evolve to a point where revenue is not coming solely from growing and selling cannabis flower and oils, but for the next 1-2 years, capacity and cost structure determine profitability.

Aphria is likely to out-earn peers through 2019 and we expect the stock multiple will move much closer to the group average over the coming 12 months as earnings results set the gold standard for the industry.

If Aphria continues to trade at such a huge discount, a consumer company or large peer will likely swoop in to try and buy up the company’s assets on the cheap.

2020 EV/EBITDA Multiple for the Cannabis Group

In the interest of full disclosure, employees of Grizzle personally purchased and currently own stock in Aphria, Inc. See the Content Disclosure section here on our Terms and Conditions page for more details.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.