If Donald Trump is not a national security zealot, there are plenty in Washington who are. This raises the threat of China being kicked out of benchmark investment indices as threatened of late by some of Washington’s more extreme China hawks. But assuming this does not happen, the growing weighting of China raises “concentration” risks for investors in the global emerging market context.

Concentration Risk of Chinese Equities

The overall index allocation to so-called China A shares will grow from 2.5% now to 3.8% at the end of November based on the MSCI Emerging Markets Index, meaning that China in total will then account for 32.6% of the index after including Hong Kong quoted and U.S. quoted China stocks. It is quite possible that by 2022, Chinese equities with A-share full inclusion will be close to a 40% weighting in the FTSE Emerging Index and the MSCI Emerging Markets Index.

If this is one aspect of concentration risk, another is that the top five countries in the FTSE Emerging Index could also account for more than 80% of the index by 2022. All of this is likely to lead to a growing debate in coming years about whether it makes sense to have a separate allocation for China, and another for global emerging market allocation excluding China. This is, of course, for those entities that do not have a problem investing in China on political grounds. Meanwhile, the growing concentration of China will also raise issues for passive investors tracking indices.

Passive Investing

This is one of the consequences of the by now extremely extended fashion for “passive” investing, or indexing, otherwise known as “investor socialism”. While on the subject of passive investing, also noteworthy is the commercially smart efforts by the passive indexing investing community to portray themselves recently as part of the politically correct trend to monitor corporate activity from a so-called “Environmental, Social and Governance (ESG)” standpoint.

This makes sense from a business point of view, given the current stampede by the world’s fund management community to issue statements including the word “sustainable”. But the problem, of course, with the indexers’ efforts to jump on this particular bandwagon is that they do not have the ultimate sanction over any corporate’s behaviour. That is because they cannot sell the stock unless it is removed from an index.

Orthodox vs Unconventional Monetary Policy

Meanwhile, returning to emerging markets, there is one area that the emerging world continues not to get the credit it deserves; though this is more important from a fixed income and currency aspect than from an equity standpoint. That is that most emerging markets have adhered to far more orthodox monetary and fiscal policies than their developed world counterparts in the past ten years and more since the global financial crisis.

If this is clear, given the pursuit of unconventional monetary policy in the G7 world in the past decade, that reality is much less reflected in sovereign credit ratings; though it must be admitted that intangibles such as strength of legal systems and institutions are also relevant here. Still, there is a much better secular case to be overweight emerging market sovereign debt than there is to be overweight emerging market equities; most particularly given the negative bond yield phenomenon in the developed world.

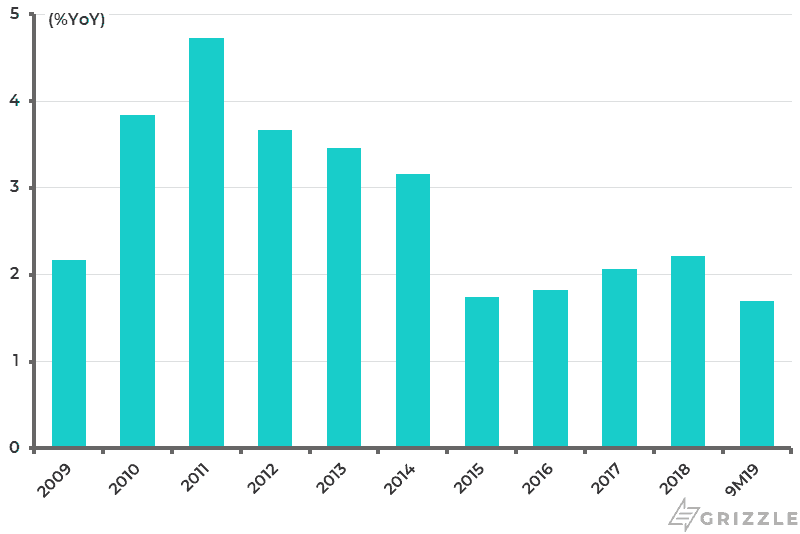

Still, for that to be reflected in dramatic emerging market outperformance the G7 central banks would have to lose credibility and the risk is, by then, the emerging market central banks will have been driven into similar unconventional policies because of slowing growth and falling inflation. On this point, the average CPI inflation for ten major Asian ex-Japan countries has declined from 4.7% in 2011 to 1.7% in the first nine months of 2019 (see following chart).

Asia ex-Japan Average CPI inflation

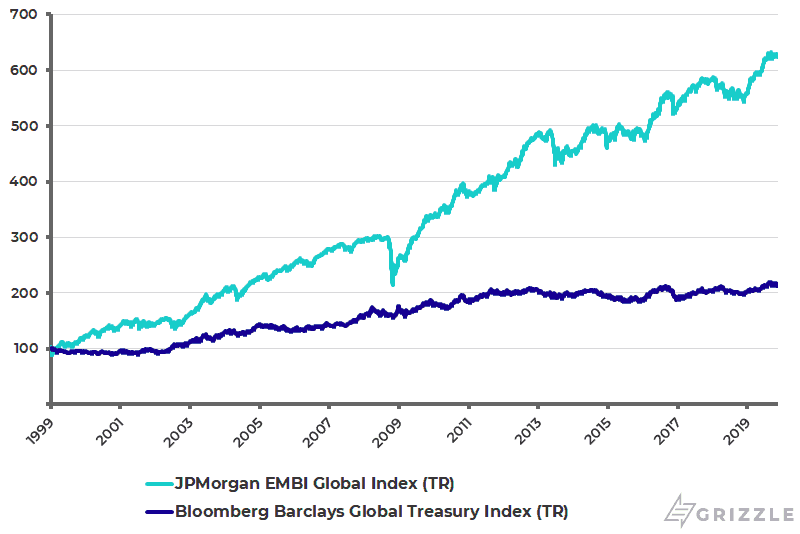

Meanwhile, it is already the case that emerging market sovereign debt has dramatically outperformed global sovereign debt over the past two decades. This reflects the orthodox approach of many major emerging markets compared with the increasingly unorthodox macro policies in the G7 world. The JPMorgan EMBI Global Total Return Index has risen by 525% in U.S. dollar terms since the beginning of 1999, compared with a 114% increase in the Bloomberg Barclays Global Treasury Total Return Index (see following chart).

JPMorgan EMBI Global Index and Bloomberg Barclays Global Treasury Index (Total return basis)

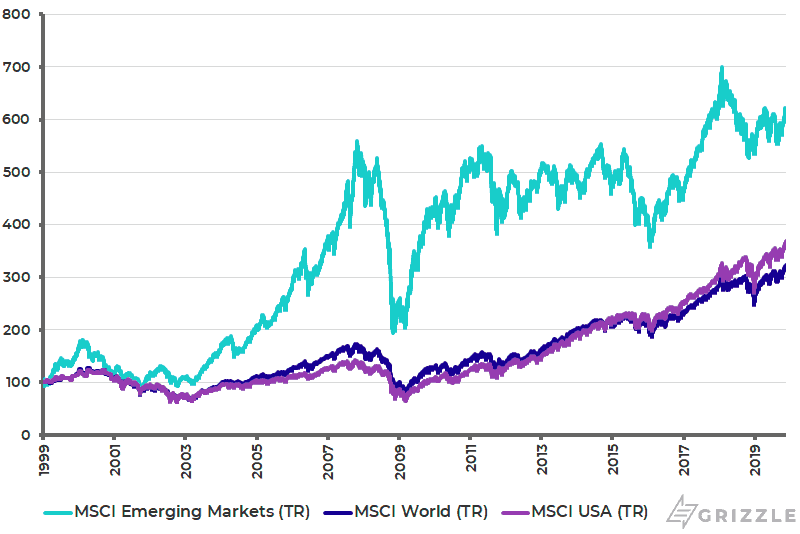

MSCI Emerging Markets, MSCI World and MSCI USA Since 1999 (Total Return Basis in US$ Terms)

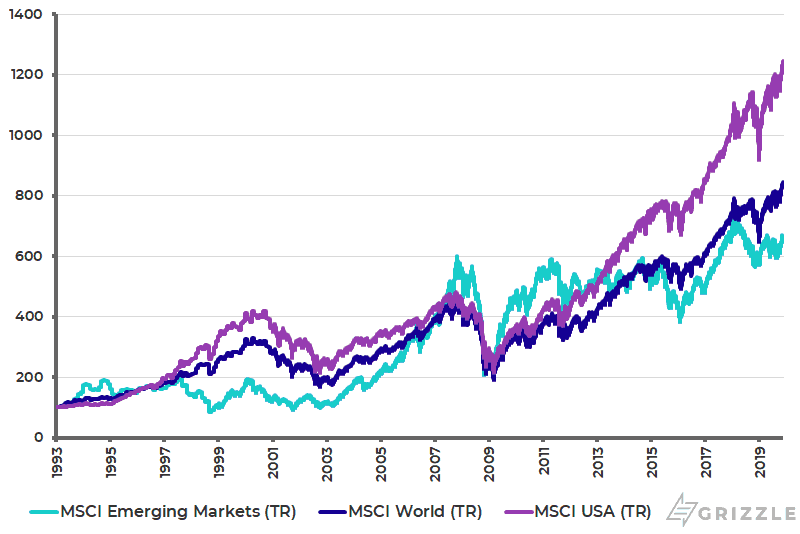

As for equities, the MSCI Emerging Markets Index has also outperformed the MSCI World Index (developed markets) over the past two decades. The MSCI Emerging Markets Index has risen by 508% in U.S. dollar terms on a total-return basis since the beginning of 1999, compared with a 224% gain in the MSCI World Index and a 269% gain in the MSCI USA Index (see previous chart). But it should be noted that in the case of equities the relative performance looks very different depending on where the starting point is. For example, the MSCI Emerging Markets has risen by 553% on a total-return basis since the start of 1993, while the MSCI World and the MSCI USA are up 744% and 1145% respectively over the same period (see following chart).

But perhaps more relevant, the MSCI Emerging Markets Index is up “only” 149% on a total-return basis since the beginning of 2009, compared with a 336% gain in the MSCI USA and a 230% gain in the MSCI World Index. It is the last ten years’ underperformance that has driven the current “end of the emerging market asset class” bear story. This issue will be discussed in the next column.

MSCI Emerging Markets, MSCI World and MSCI USA since 1993 (Total Return Basis in US$ Terms)

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.