27 August was the Ganesh Chaturthi holiday in India.

But it was not a happy day in the country in the specific sense that the Trump administration went ahead with the threatened 50% tariff levied on Indian goods exports, with the main exemption pharmaceuticals.

This amounts to an estimated US$55-60bn direct hit to the economy with the most negatively impacted sectors the likes of textiles, shoes, jewellery and gems, all of which are employment intensive.

This writer would never have predicted such an outcome.

But conversations in New Delhi two months ago make it clear that the tariffs are primarily the consequence of the American president’s “personal pique” that he was not allowed to play a role in seeking to end the long running acrimony between India and Pakistan following the four-day military conflict between the two countries in May.

India has never accepted third party intervention in its relations with Pakistan and this remains a “red line” despite the economic costs of depriving the 47th American president of one of his opportunities to win the Nobel Peace Prize.

The other point is that no Indian government, including the current government, is going to open up agriculture to imports given the devastating impact it would have on many poor people.

Nearly 250m farmers and related labour derive their incomes from agriculture with the sector accounting for nearly 40% of India’s workforce.

That said, the word is that the two countries were very close to securing a trade deal before the conflict with Pakistan broke out triggered by the killing of 26 Indian tourists in Kashmir in April.

So the draconian tariffs India now faces is the result of an unfortunate series of events, compounded by the fact that Donald Trump has not ended the Ukraine conflict as he stated he would do.

As a result, India’s continuing purchases of Russian oil again become an issue.

But the reality is that everyone in the Indian capital understands that the real issue is the refusal to allow Donald Trump’s personal intervention in the Pakistan issue.

This is a classic example of where the “conceptual vacuum” in Washington is not in the national interest since it is surely not in America’s interests to push India closer to China, a trend which was already happening with direct flights between the two countries having resumed in late October after more than five years.

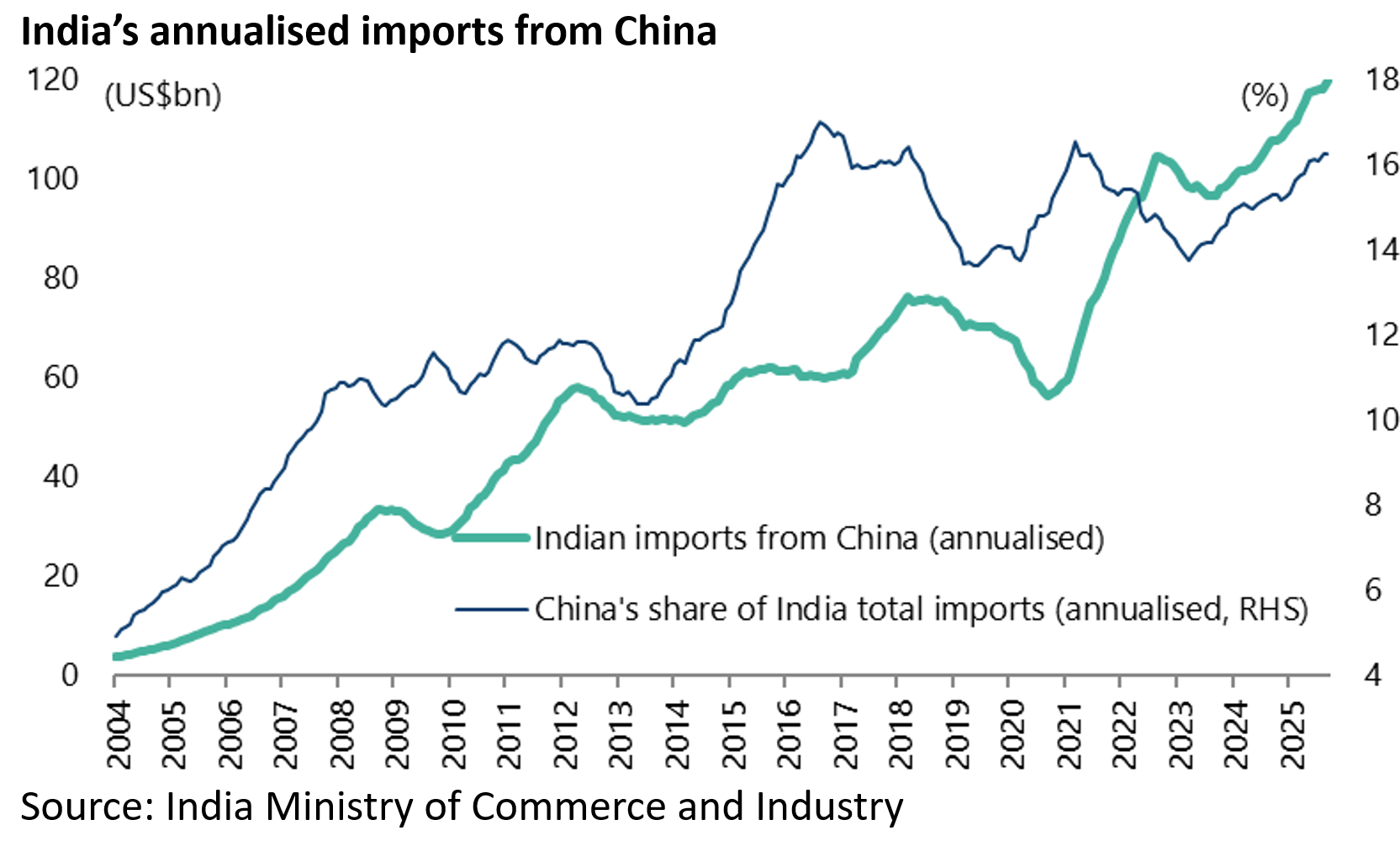

Meanwhile, India needs China’s cheap goods, for example, solar panels, with China imports into India now running at an annualised US$120bn or 16.3% of India’s total imports and growing by 11% YoY in the 12 months to September.

Meanwhile, there remain growing hopes of a deal being negotiated in the near term.

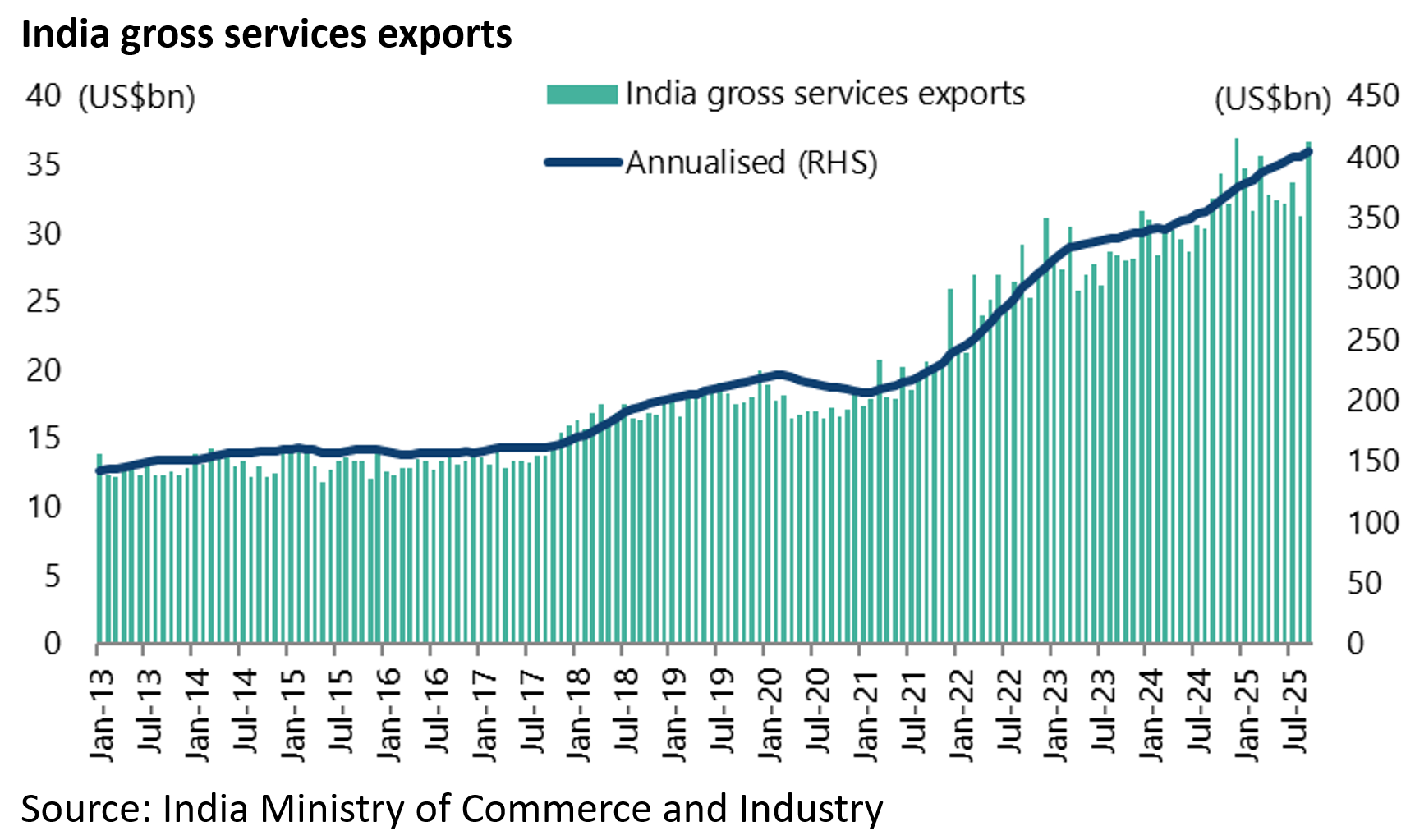

The other positive point is that the Trump administration has not yet at least focused on India’s booming exports of services.

This is not just IT services currently running at US$150bn annually, but also so-called global capability centres (GCCs) set up mainly by US multinationals which base their IT infrastructure out of India and where revenues total around US$60bn annually.

This reflects the reality so far that when Trump talks about trade, he seems to be almost solely focused on trade in goods.

Will India Stop Russia Oil Imports?

As regards the Russian oil issue, Delhi has also maintained a relatively hard line.

Foreign minister Subrahmanyam Jaishankar has stated publicly that the largest importer of Russian oil is Europe, albeit oil which has often been refined in India, thereby highlighting European hypocrisy on this issue.

He also noted, as previously discussed here (see The Real Sticking Point in China-US Negotiations, 27 October 2025), that China remains the bigger buyer of Russian oil.

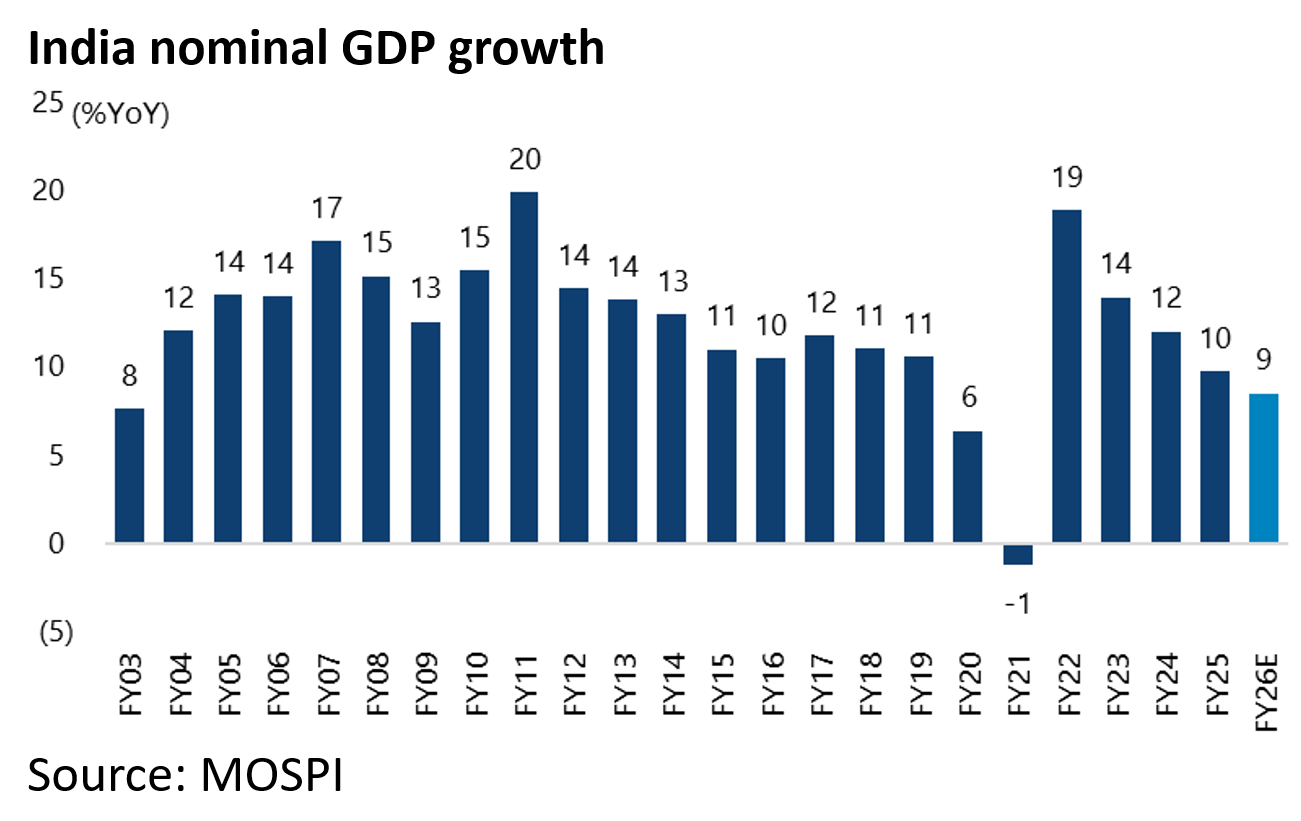

The tariff issue is all the more important in India because growth has slowed this year, particularly nominal GDP growth which is so important for equity markets.

The estimated nominal GDP growth of 8.5-9.0% YoY in FY26 ending 31 March 2026 would mark the lowest growth rate in the past two decades except Covid-related FY20 and FY21.

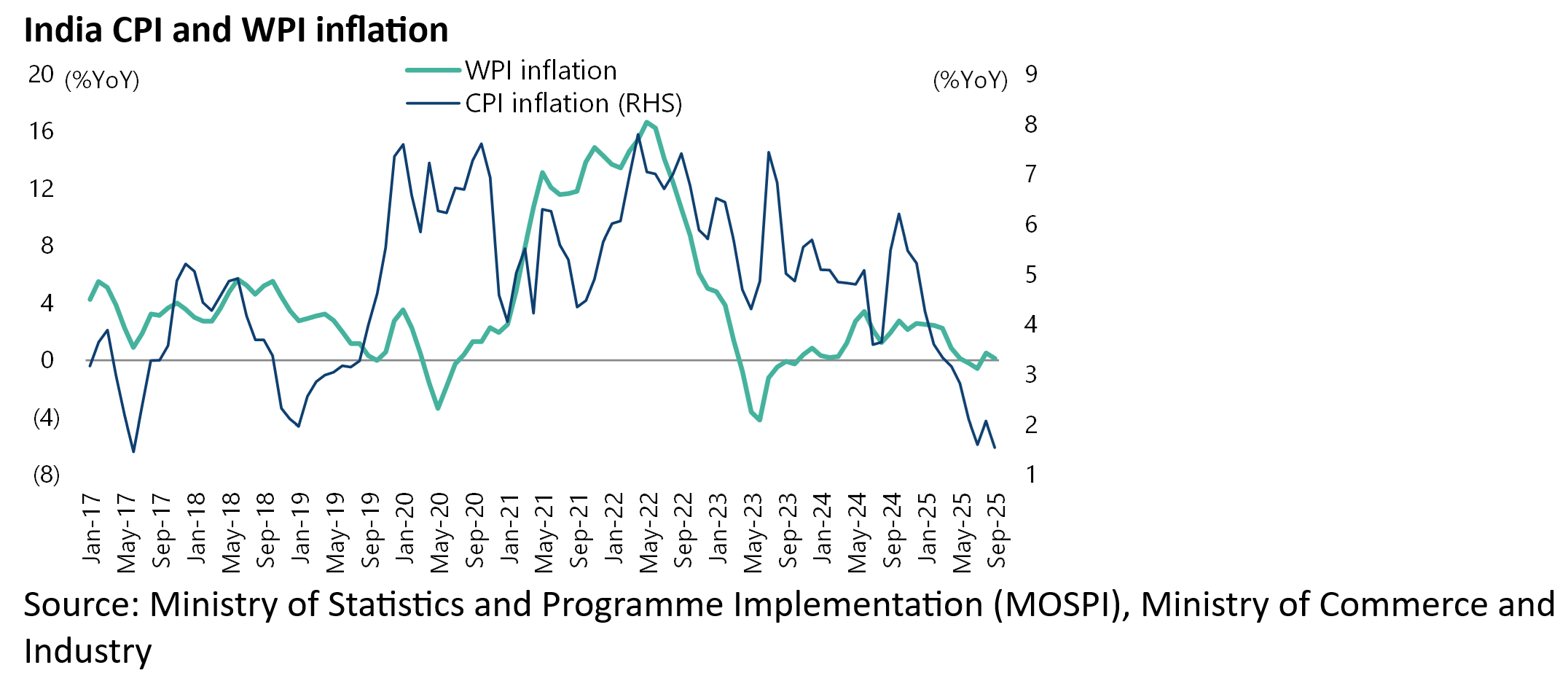

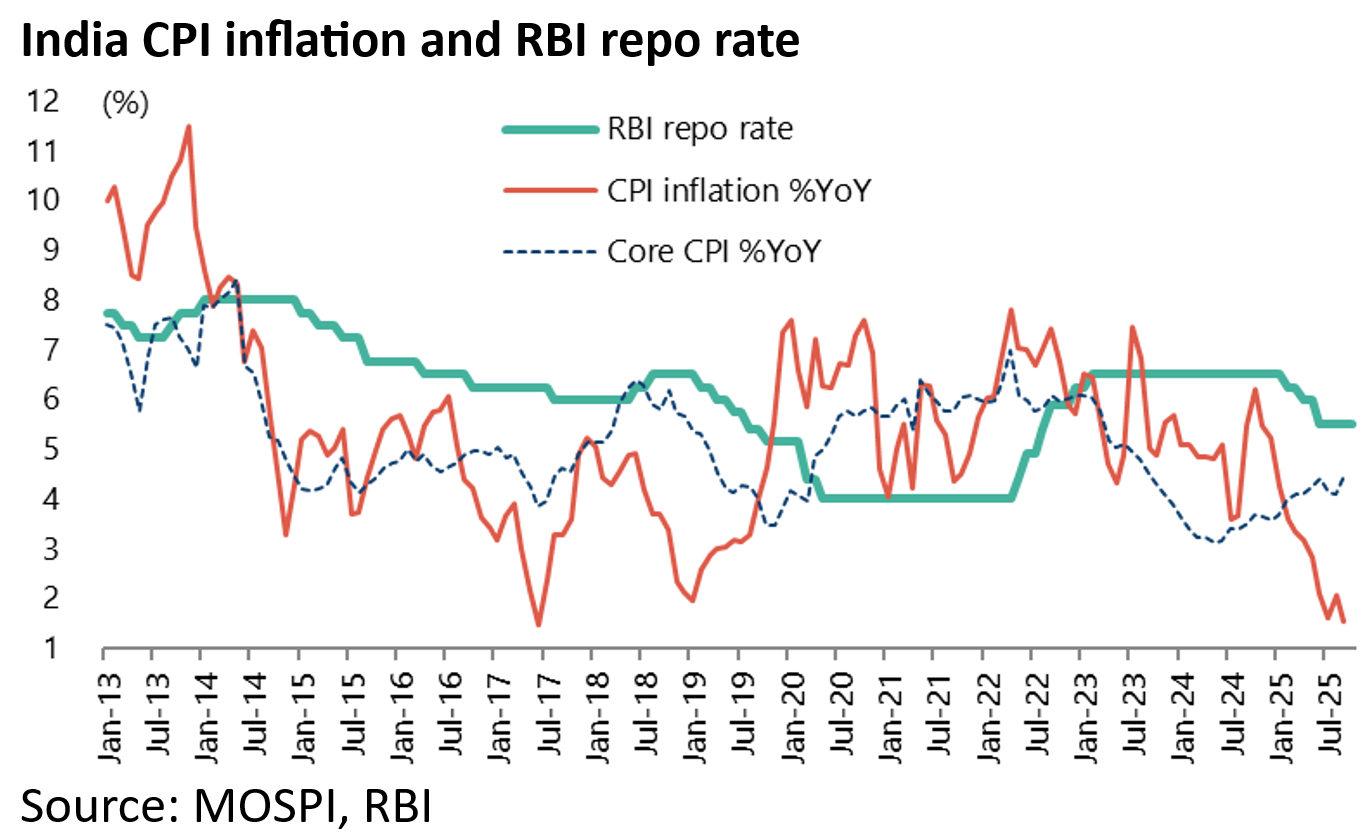

The main reason for this nominal slowdown is that headline CPI inflation was at an eight-year low of 1.5% YoY in September. While WPI inflation was only 0.1% YoY in September.

How is India Coping with US Tariffs?

Still, if this is the backdrop, the reason the stock market has not yet reacted more negatively to the 50% tariffs, particularly consumption-related stocks, is the escalating policy response of the government.

Income tax cuts were already implemented in the February budget.

But the more positive news of late has been a rationalisation and simplification of GST where the previous four bands (5%, 12%, 18% and 28%) have been reduced to two bands (5% and 18%).

This GST overhaul has been long in the planning, but execution was speeded up as a direct result of the Trump triggered tariff issue.

The new GST rates took effect 22 September.

The view is that the fiscal loss will only be small to the central government.

Indeed, the hopes are that the GST cuts will be self-financing by generating more sales.

Meanwhile, if the income tax cuts primarily favour the urban middleclass since only an estimated 30m Indians pay income tax, the benefits from GST cuts are much more widely spread as a tax on spending is felt by everybody.

If these are the two major pro-consumption initiatives taken by the government so far, though more fiscal easing is likely coming, the Reserve Bank of India (RBI) has also turned unambiguously doveish since new governor Sanjay Malhotra took over last December.

He has cut the policy repo rate by 100bp since February to 5.5%, though keeping it unchanged in the last two meetings in August and October, with the possibility of another 25bp cut to 5.25% by the end of this fiscal year ending 31 March 2026, given that inflation has been running well below the central bank’s formal target of 4%+/-2% (i.e. 2-6%). Headline CPI inflation was 1.54% YoY in September.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.