Bottom Line

This was the second quarter we got to see what Tilray is all about and we couldn’t find anything in the financial results to make us hopeful the company can grow into their eye-watering valuation.

Frankly, Tilray looks to be about one to two quarters behind Canadian peers in their quest to ramp up capacity to take advantage of the start of legal sales.

We question the edge they have that will allow them to catch up to peers who will have significant market share advantages in Canada by the time Tilray ramps up its own capacity.

Tilray may have a well-respected management team, top-notch research pipeline and solid brands, but the stock price is too high for the company to ever grow into over the next 3-5 years.

Why pay 340x sales when you can own companies with three times the funded capacity, thousands of medical clients, lower costs and faster growth for 1/10th the price.

Tilray may be able to placate investors for another quarter, but eventually, stockholders will realize this is a company that will never grow into its current stock price.

A correction is likely to follow.

For their own good cannabis investors need to splash some cold water on their face, come back to reality and put their money elsewhere.

Operational Review

Tilray sold 1,613 kg in the quarter, up only 7% from the prior quarter.

This is much slower volume growth than peers who have been ramping up grams sold by 15%-50% over the prior quarter.

Tilray is selling more product wholesale which led to falling revenue and gross margins and could continue to weigh on profitability next quarter as the company will be buying more product wholesale from another licensed producer to meet demand.

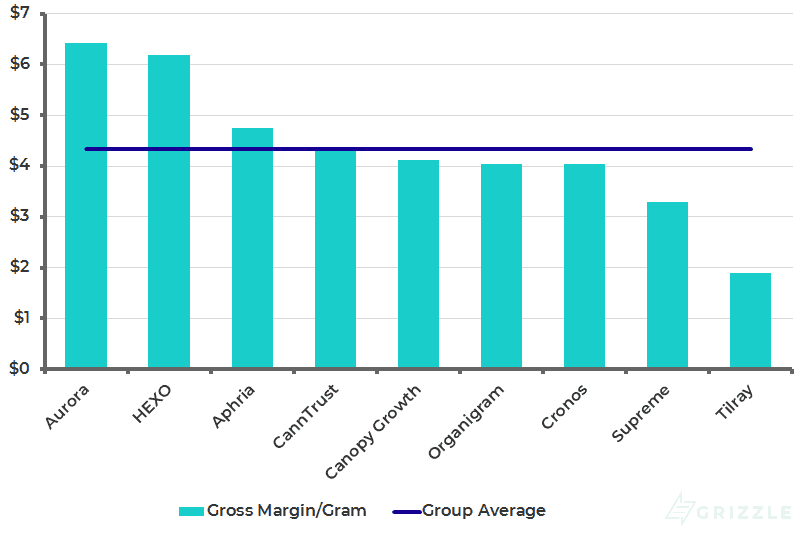

Taking Tilray’s gross margin and dividing it by grams sold, we can compare profitability among LPs.

Tilray has the lowest margin in the peer group and was 50% below the group average of $4.20/gram.

Gross Margin Per Gram

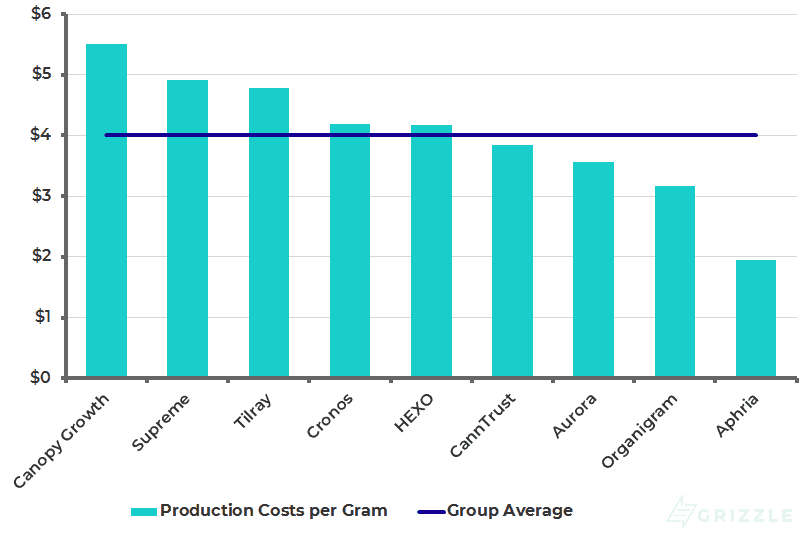

A big part of the reason Tilray’s margins are lower than peers is because of its higher cost structure.

Production costs are about $5/gram, 25% above the peer average. Costs per gram will definitely fall as volumes harvested increase, but Tilray still has a lot of work to do.

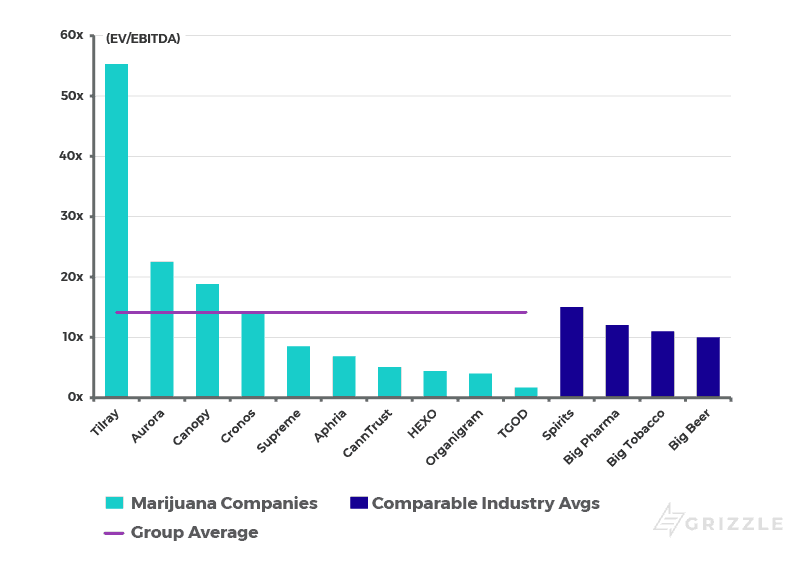

Valuation is in the Clouds

The best way to illustrate the world investors think Tilray will live in 3 years from now is with two examples.

If Tilray sells cannabis for this quarter’s selling price of $8.00/gram, the company will have to sell 375,000 kg a year at a 30% EBITDA margin to justify the current market cap.

375,000 is more than Tilray’s funded capacity and would represent a 40% market share of all cannabis sales in Canada.

Put another way, when Tilray reaches funded capacity of 140,000 kg they will have to sell each gram for $22 to justify their $13.5 billion market cap, a 175% increase from current selling prices.

Even in Tilray uses the $600 million raised in October to buy another Cannabis company the stock will continue to be the most expensive in the industry.

Any way you slice it Tilray is priced for an unlikely future.

We think investors will be much better off by investing in LP’s with cheap valuations and low production costs (Aphria), top-tier products (CannTrust), leading market share (Aurora) or the support of a major liquor company (Canopy Growth).

EV/EBITDA in 2020

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.