The recent crash of Boeing’s (NYSE: BA) stock price has been absolutely spectacular.

The company was already dealing with issues with the Boeing 737 MAX before the current coronavirus outbreak caused a general stock market crash and hit the aviation industry especially hard.

Although Boeing is only the manufacturer of jetliners, airlines have already started cutting or deferring orders of Boeing’s jets due to falling demand and the 737 MAX issues.

Last December, Boeing fired its then-CEO Dennis Muilenburg for allegedly mismanaging the 737 MAX crisis.

During Muilenburg’s time as CEO, two of Boeing’s 737 MAX jets crashed, with faulty autopilot software designed by Boeing to blame.

Dave Calhoun, previously the chairman of Boeing, was appointed CEO after Muilenburg was pushed out.

It is safe to say that Calhoun’s tenure as CEO thus far has been anything but smooth.

In the last month, Boeing’s stock price has crashed more than 50%.

With the stock at a 4 to 5 year low, it got us wondering, is now the time to buy Boeing stock?

How An American Giant Lost Its Way

The cultural issues at Boeing were highlighted in the aftermath of the two 737 MAX crashes.

In a leaked email between two Boeing engineers discussing the 737 MAX, one states “This airplane is designed by clowns, who are in turn supervised by monkeys”.

Although the collapse in stock price is recent, Boeing’s problems unfolded over many years.

Boeing was forced to accommodate a larger engine on the 737 MAX and sought a solution in implementing the Maneuvering Characteristics Augmentation System (MCAS) which was designed to make the plane behave in the same way as the previous generation of 737s.

It was revealed at a later date that the MCAS would sometimes cause the plane to suddenly pitch the nose of the plane downwards if it malfunctioned or was fed bad data.

It was also revealed that Boeing had neglected to tell aviation regulators about the existence of the MCAS system due to fear of regulators demanding pilots having to retrain.

This meant that pilots on the two ill-fated flights had little to no training when flying the 737 MAX and may not have known what to do when the MCAS system malfunctioned.

The Boeing 737 MAX has been grounded worldwide since March of last year.

Originally, Boeing expressed hopes that the plane would fly again in mid-2020. We will see whether the coronavirus outbreak and the general slowdown of business at Boeing will cause delays in the certification process as regulators and government workers are forced to work from home.

The Bailout

With all these recent troubles, it is reported Boeing is seeking a $60B bailout from the government.

A Boeing bailout is surely going to be unpopular with the American public. The memory of big corporations being bailed out during a financial crisis still leaves a sour taste in the mouths of many who lost their jobs in the Great Recession of 2008-9.

Although the circumstances this time are different, many people see Boeing’s current troubles as consequences of their own making due to poor management that made them ill-prepared for a financial crisis, even if the company did not cause the financial crisis itself.

Many people remain angry at Boeing for using their cash to buyback their own stock before the coronavirus outbreak tanked the market.

The CEO of Boeing, Dave Calhoun, has gone on the record saying that Boeing still has over $15 billion in total liquidity from drawing on a $13.8 billon loan and can survive without a bailout if worst comes to worst.

Although later in the same interview Calhoun admitted that if present circumstances continue for 8 months, Boeing would need to be bailed out for real.

Calhoun is committed to rejecting any government proposal that requires Boeing to give up an equity stake in return for the bailout money.

If the government insisted on equity in Boeing then he would look at “plenty of other options”.

Apart from the equity stake option, realistically, there are two other options for a Boeing bailout.

- A debt guarantee

- Cash injection

A cash injection seems to be the easiest option.

As the name suggests, the U.S. government would just give Boeing cash in exchange for some stipulations.

The cash would most likely only be allowed to go to employee payroll or other costs that are essential to Boeing’s operations.

The other option is a debt guarantee, where the government would guarantee Boeing’s debt so the company could borrow additional funds on a longer-term basis.

The government likely would prefer a debt guarantee as they would not have to commit any cash upfront.

Besides the equity stake route, the debt guarantee is the most likely outcome in our opinion.

Boeing actually has quite a bit of leverage in negotiating a favourable bailout deal with the U.S. government.

Boeing claims that it is responsible for 2.5 million jobs and holds the secrets to many defense technologies like attack helicopters and bombers.

The details of the bailout are still pending, but it is very likely that some sort of bailout deal with the U.S. government will be reached. Boeing is far too important to the U.S. for the government to allow them to fail.

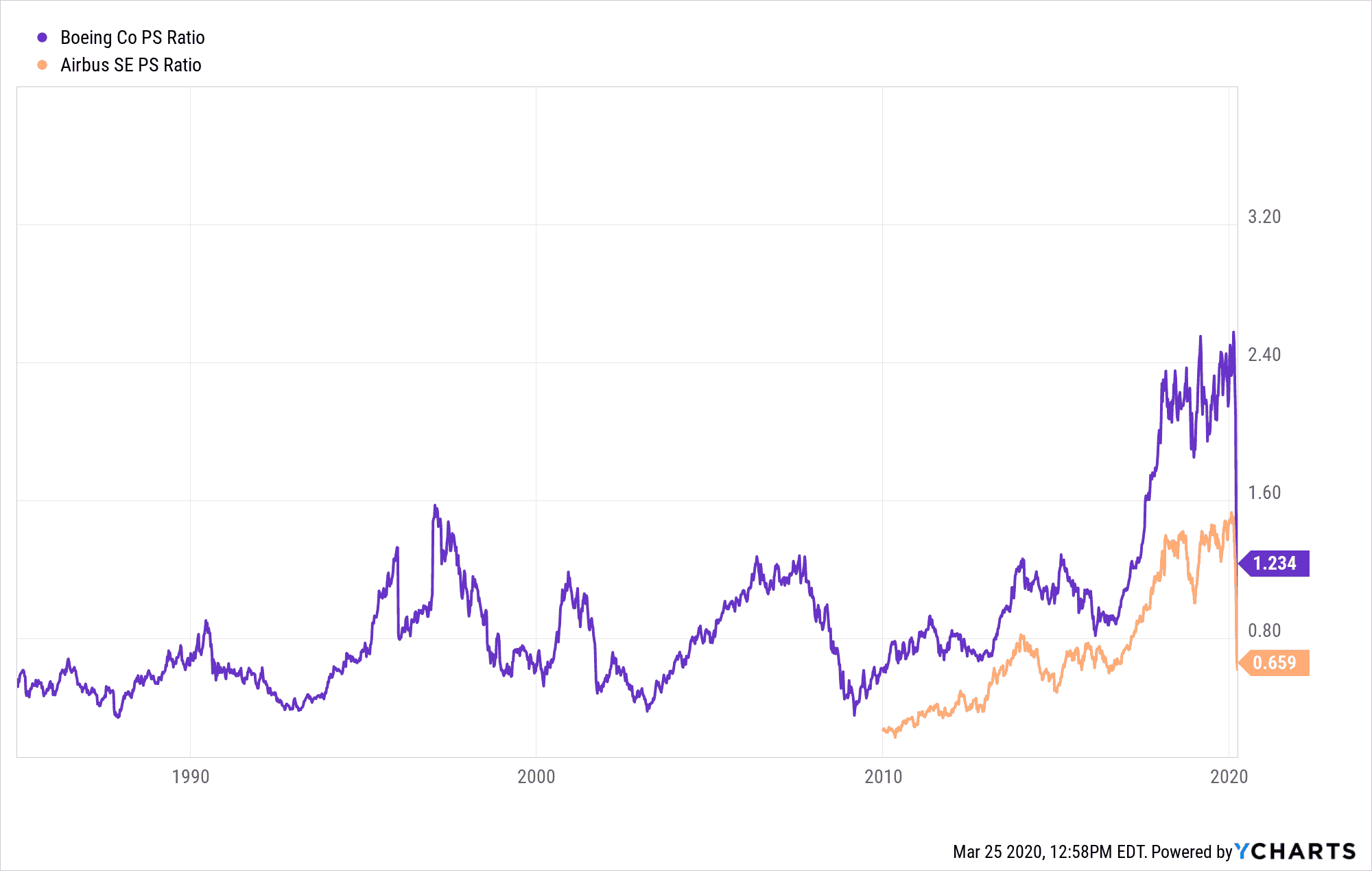

Boeing Still Seems Expensive Despite The Big Drop

Taking a look at the price to sales multiple for Boeing, we see that although it has dropped spectacularly, it is still much higher than the lowest levels reached back in March 2009, during the financial crisis.

Boeing currently trades at a P/S of around 1.2x versus under 0.4x back in March 2009.

Also note that the P/S ratio is still higher than Airbus, Boeing’s main competitor who doesn’t have the same acute financial and regulatory problems.

Boeing Trailing Price/Sales Higher than 2009

It is worth noting that Boeing stock surged 15% today due to the U.S. Senate agreeing on a stimulus bill.

The details of the deal are still trickling in, but it appears that $17 billion has been set aside for businesses that work in “national security” which would almost certainly include Boeing since the company is a well-known defense contractor for the U.S. Military.

Bottom Line

A lot needs to go right for Boeing in the coming months.

On a macroeconomic scale, we need to see some sort of a sign that the COVID-19 pandemic is coming under control otherwise airline stocks along with their suppliers, will continue to get hammered.

Boeing also has to get the 737 MAX re-certified as soon as possible.

Boeing’s former high-flying stock price was bolstered artificially by stock buybacks, and with no more buybacks happening any time in the foreseeable future, we have a hard time imagining Boeing stock being anywhere close to its former highs anytime soon.

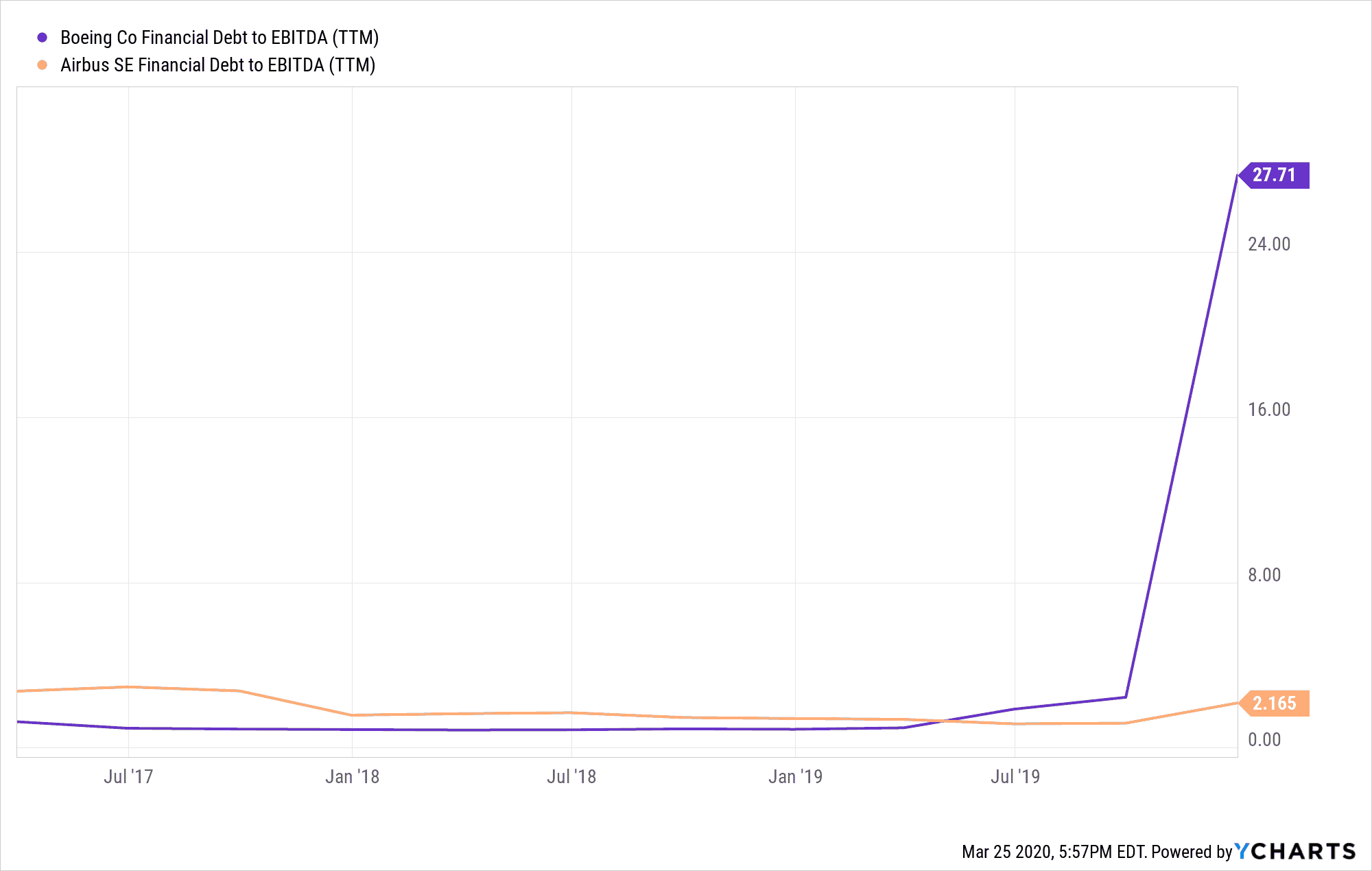

Not to mention Boeing’s mounting debt which has already eclipsed $28.5 billion according to Yahoo Finance, and is expected to only climb more in the near term.

We see that Boeing’s Debt/EBITDA has skyrocketed over the past 3 years, coming in at over 27 times due to financial difficulties.

In contrast, Airbus, Boeing’s main competitor, sits at a Debt/EBITDA of just over 2 times with total debt of just €10 billion ($15.45 billion USD).

Boeing’s Debt/EBITDA Has Skyrocketed

Even when we include the impact from the recently announced government bailout, from a long term perspective, we still don’t think buying Boeing stock is worth the risk.

The valuation still seems expensive when you factor in all the issues at the company.

A government-backed debt guarantee simply ensures that the stock won’t fall to zero, but that’s hardly reason enough to go out and buy the stock.

Buying the stock right now is not just a bet that the coronavirus threat will be over in 8 months, but also a bet that Boeing will be able to re-certify the 737 MAX in a timely manner.

And the question remains, will Boeing have trouble servicing all this debt if the timeline to bring the planes back online gets drawn out?

Further, will they also be able to execute their cash saving plans smoothly without suffering too many hits to their core operations?

This involves suspending its dividend entirely, and also promising to suspend all stock buybacks, both of which the company has already done in a bid to win some public favour for their bailout request.

Boeing has also made moves to preserve cash like implementing an immediate hiring freeze.

In particular, the company said to CNN Business that it will implement these steps to curb cash burn:

- Limiting travel and discretionary spending to business-critical activities only.

- Limiting overtime to critical 737 MAX return-to-service support and other key efforts in support of our customers.

- Pausing or placing on hold any new personnel requisitions at this time, pending a review of priorities and critical needs.

According to Fox Business, an insider that’s familiar with the industry stated about Boeing that layoffs or furloughs were also “a real possibility”.

Although Boeing has denied that it has any immediate plans for layoffs.

Some may argue that the 737 MAX issues are priced into the stock already because a bailout is so likely and investors are expecting it, the upside from a bailout may be priced is as well in our opinion.

Not to mention that there are still deep-rooted cultural issues like low employee morale and reports of engineers dissatisfied with the company‘s vision (or lack thereof).

These issues won’t be resolved overnight or even in 8 months.

The stock may have some upside after the coronavirus is brought under control, but the same could be said for many other stocks that have less baggage to deal with.

The long-term cultural issues make it a less compelling buy than it once was, which is why we prefer other stocks.

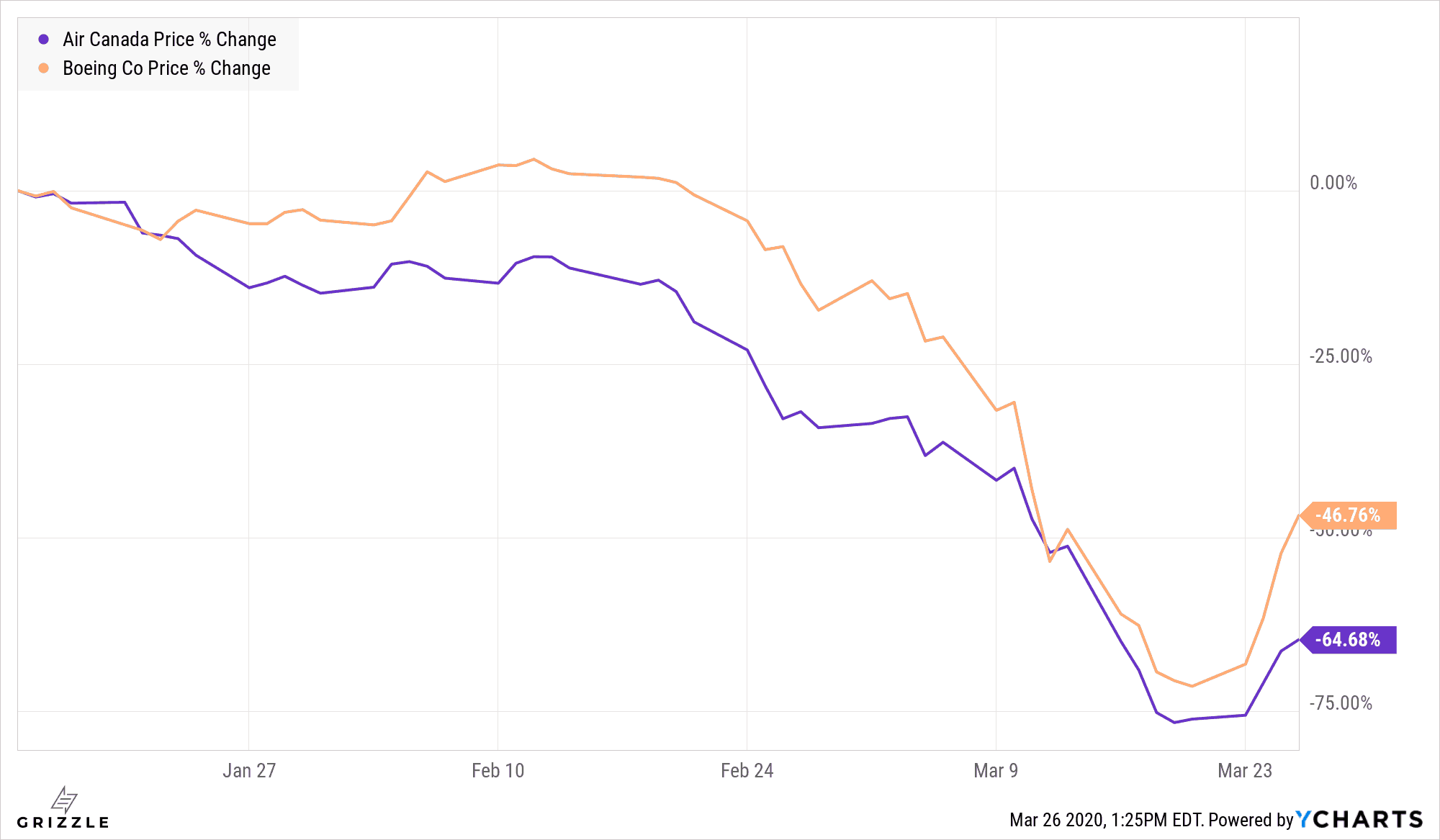

A better alternative is Air Canada (TSE: AC), which has C$5.89 billion in cash and trades at a forward P/E of just over 6, 50% cheaper than Boeing’s multiple.

Similar to Boeing, Air Canada is a national champion to the Canadian government and we believe a bailout is highly likely if the company runs into trouble from a prolonged coronavirus shutdown.

Therefore, Air Canada has the similar “government put” that Boeing has.

Since the crisis began, Air Canada has obviously been hit very hard due to a huge drop in demand in the travel industry, falling from the mid-40s dollars per share range down to just under $20/share, a decline of 65%.

Air Canada has not rebounded like Boeing and will rebound as the Coronavirus crisis recedes, plus offers better long term upside with a cheaper valuation, lower debt, and less operational baggage.

Stock Price Change Since Coronavirus Worries Began

In normal times, Boeing stock may be a buy, but in present market conditions, there seem to be way better deals elsewhere in the stock market considering the market as a whole has fallen over 30% since a little more than a month ago.

If Boeing crashes by another 50%, we think both the virus and problems with the MAX are all priced in and you should buy, but until that happens trade it, don’t own it.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.