The Coronavirus continues to dominate the narrative with the lockdowns imposed by governments leading to a dramatic decline in activity.

Still long after the virus has disappeared from the headlines there will be long term consequences from some of the policies now being taken.

In the area of monetary policy the Federal Reserve has now crossed the Rubicon in terms of explicitly entering the fiscal area.

The key development, announced on 23 March, was that the Fed will deploy US$30bn in equity capital from the Treasury’s Exchange Stabilization Fund.

This monetary-financed fiscal facility can be leveraged 10 to 1 to buy corporate bonds and lend to businesses.

This, and the related announcement that the Fed has embarked on “unlimited” quanto easing, are what the media have liked to describe as the Fed “bazooka”.

There are now estimates that the Fed’s balance sheet could reach US$9-10tn by the end of this year, up from US$4.2tn at the start of this year.

But this is not the end of the Fed’s venturing into the fiscal area. The gigantic US$2tn fiscal package, finally approved on 27 March, has “earmarked” US$454bn for Fed collateral to fund assorted lending programs.

Again the idea is this can be leveraged 10 to 1.

So fiscal and monetary policy will become ever more intertwined as a result of the Fed’s long recognized promiscuous ability to create dollars out of thin air.

But it seems clear that Congress will want a say in terms of how this Fed funding is deployed in the real economy.

Are we Seeing the Beginning of the End for the 40 Year Bond Bubble

There is one “big picture” point that institutional and retail investors everywhere should now be thinking about.

That is whether all this dramatically ramped up government interventionism, and the resulting ever-greater merging of monetary and fiscal policy in the context of ballooning fiscal deficits, marks the beginning of the end of the bull market in US Treasury bonds in place since 1981.

This is an extremely tricky question to answer in the short term. This is because the economic shutdown, triggered by the Coronavirus, is likely to lead to a dramatic decline in velocity which is government bond bullish.

US Money Velocity (Nominal GDP/M2)

It is this anticipated plunge in velocity which makes it quite conceivable that the 10-year Treasury bond yield retests its recent low of 31.4 basis points, or goes even lower, as economic activity collapses.

Still this is only 33.9 basis points below current levels and should mark the end of the secular bull market in Treasury bonds (see chart below).

US 10-year Treasury Bond Yield (log scale)

Since the Fed will probably not contemplate negative rates, this means that the long-term risk-reward ratio of owning Treasury bonds is no longer interesting.

It also means that the risk parity trade, and all the machines and related geek programmers operating these machines, are at severe risk of becoming redundant.

The Fed Will Continue to Buy Government Bonds Forever

So the Coronavirus has served as a catalyst for Modern Monetary Theory (MMT)-style policies that were coming anyway the next time there was a downturn in the US and Europe, as a result of growing political pressures.

Even if the virus turns out to be the equivalent of a natural disaster, as is this writer’s base case, and has naturally run its course over the next, say, three to four months, the problem is that once these “temporary” policies are introduced they are likely to become more or less permanent – as has been the case with quanto easing.

Or at least investors should assume this, until proven otherwise.

If true, this means that the world could be looking at ongoing Fed direct purchases of newly issued US government debt.

This, by every law of logic and by the lessons of history, should prove sooner or later to be inflationary. Many monetarist economists have for years been wrongly predicting a pickup in inflation because they have been too focused on surging narrow money supply aggregates.

But inflation will only pick up if velocity breaks out of its long-term downtrend.

US monetary Base Growth

Federal Reserve Will Take a Page out of Japan’s Playbook

Still the policies are now being put in place in the Western world for such a secular change to happen even though the technological and demographic trends still favour the disinflationary story.

As for a potential bond investors’ revolt against surging fiscal deficits in the G7 economies, the Fed and other G7 central banks will sooner or later seek to pre-empt this by coming up with some more elaborate version of the Bank of Japan’s current yield curve control where government bond yields are “fixed” along the yield curve.

And if they do not do this pre-emptively, any kind of government bond sell-off will likely trigger such action.

Indeed this was signaled in a recent op-ed written in the pinko paper in March by Philipp Hildebrand, the former Swiss central bank governor (see Financial Times: “Central banks must evolve to help governments fight the crisis”, 25 March 2020).

The investment conclusion could not be clearer. Long-term bond investors who do not want to be locked into historically low nominal Treasury bond yields should start thinking about reallocating their money elsewhere.

In the fixed income world that means moving money out of the G7 bond universe, all of whose central banks are now likely, sooner or later, to come up with some form of yield curve control policy.

By contrast, emerging market sovereign bonds look much more attractive precisely because policy remains relatively much more orthodox.

What About Equities and Gold?

Clearly, in a world where central banks successfully suppress government bond yields by fiat, equities should outperform dramatically in relative terms.

They will also outperform in a world where G7 central banks lose credibility and so lose control of the bond market.

But in the latter case equities will do much better in nominal than in real terms.

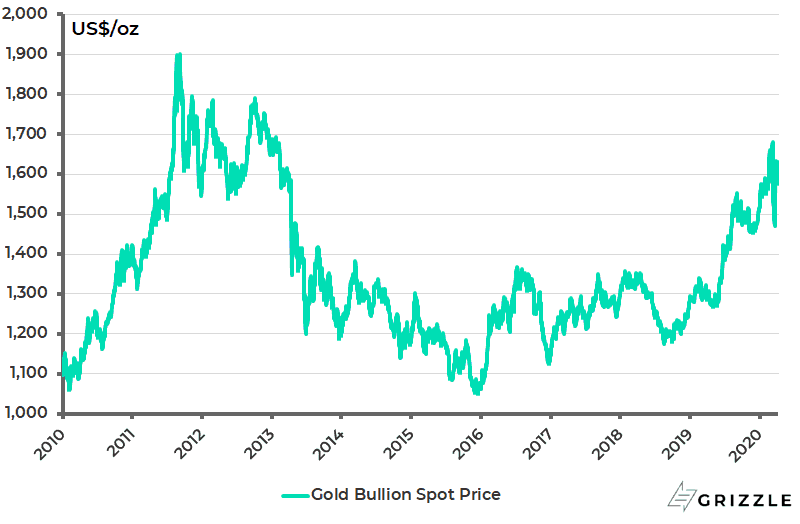

Meanwhile, the recent dramatic developments make gold more important than ever as a hedge.

Gold is vulnerable in the short term since the collapse in asset prices means investors may sell gold to raise cash to fund losses elsewhere.

Indeed this is why gold recently corrected to test the US$1460/oz support level.

It is now US$1631/oz.

Gold Bullion Price

Still there is one problem as regards owning gold that investors should be aware of.

[su_panel]That is a gold price that successfully breaks out above the previous 2011 high of US$1921/oz is a market signal that the G7 central banks are losing control of the game.[/su_panel]For that reason, these central banks will not want to see that price move happen. That is why this writer would never advise owning gold on leverage.

As for central banks outside the G7 world they will be much more relaxed about rising gold prices because they have been buying gold in correct anticipation of the sort of unorthodox policies that are now being announced by their G7 counterparts.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.