Lululemon Athletica (NASDAQ: LULU) has their earnings report for Q4 2019.

Revenue came in at $1.40 billion which beat analysts’ estimates of $1.38 billion.

EPS came in at $2.28 which beat analysts’ estimates of $2.25.

Lululemon has fared quite well throughout this whole crisis, all things considered. Being a retail company, it would be understandable for it to get hit very hard.

Although the stock has declined quite a bit since a month ago, it has rebounded quite a bit in the past few days.

LULU is still outperforming competitors and the S&P alike by quite a significant margin on a YTD basis.

Why Does Wall Street Love LULU?

Despite the recent turmoil in the markets, analysts have been upping their earnings estimates for LULU. In the past 3 months, LULU has seen 27 upward revisions and 1 downward revision on EPS estimates with analysts, according to Seeking Alpha.

As recently as this past Monday, Needham lifted LULU to a ‘Buy’ rating from ‘Hold’ and added it to its Conviction Buy List.

With all this, many investors are scratching their heads and wondering why does Wall Street love LULU so much?

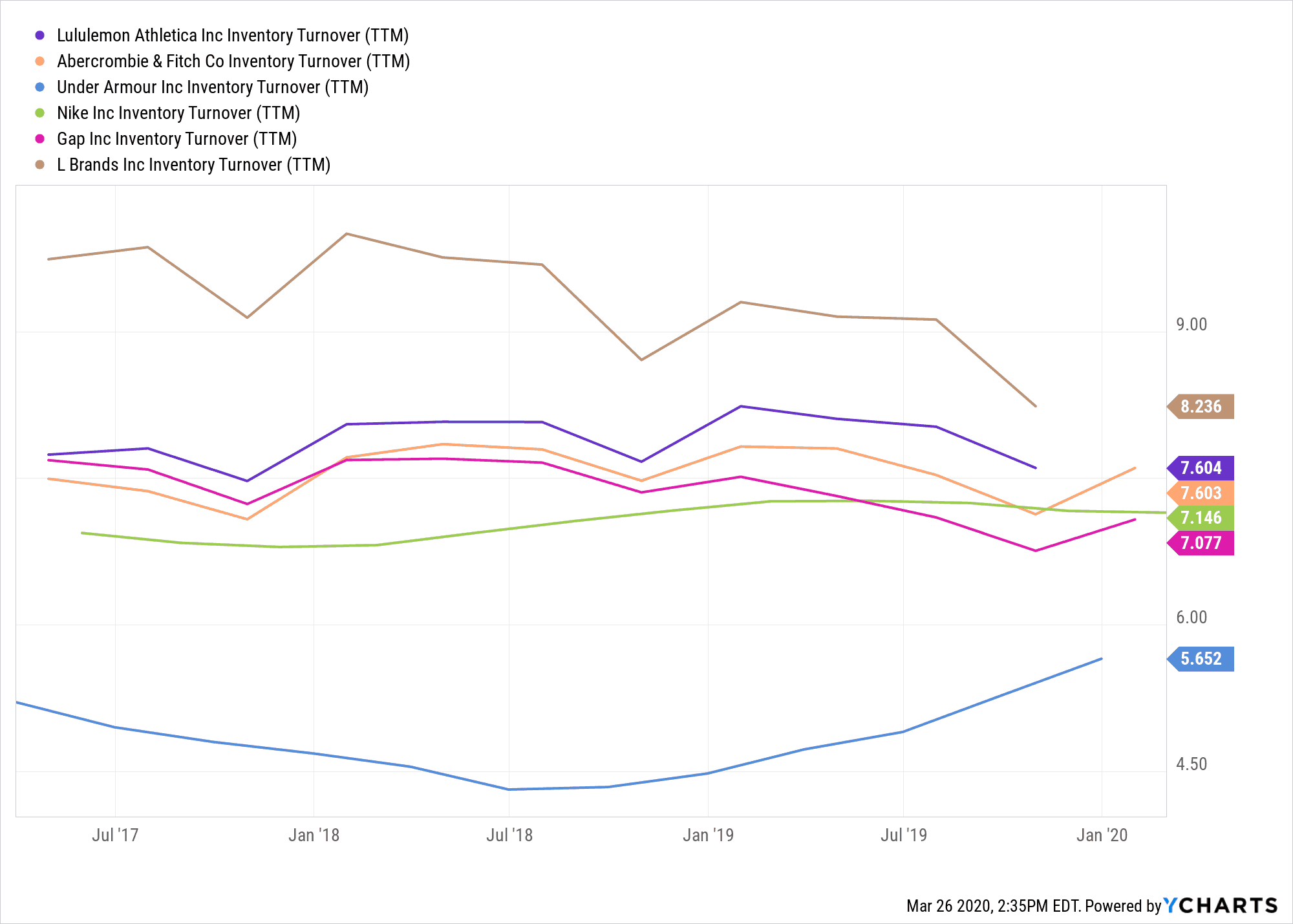

LULU Is Top Of The Pack for Many Metrics

When looking at retail stores, many analysts watch the inventory turnover rate, which measures how effectively a retailer can convert their inventory to sales.

A higher rate means better operational efficiency since it implies the company has less unsold inventory to deal with.

We see that LULU comes in near the top for Inventory Turnover among its peers.

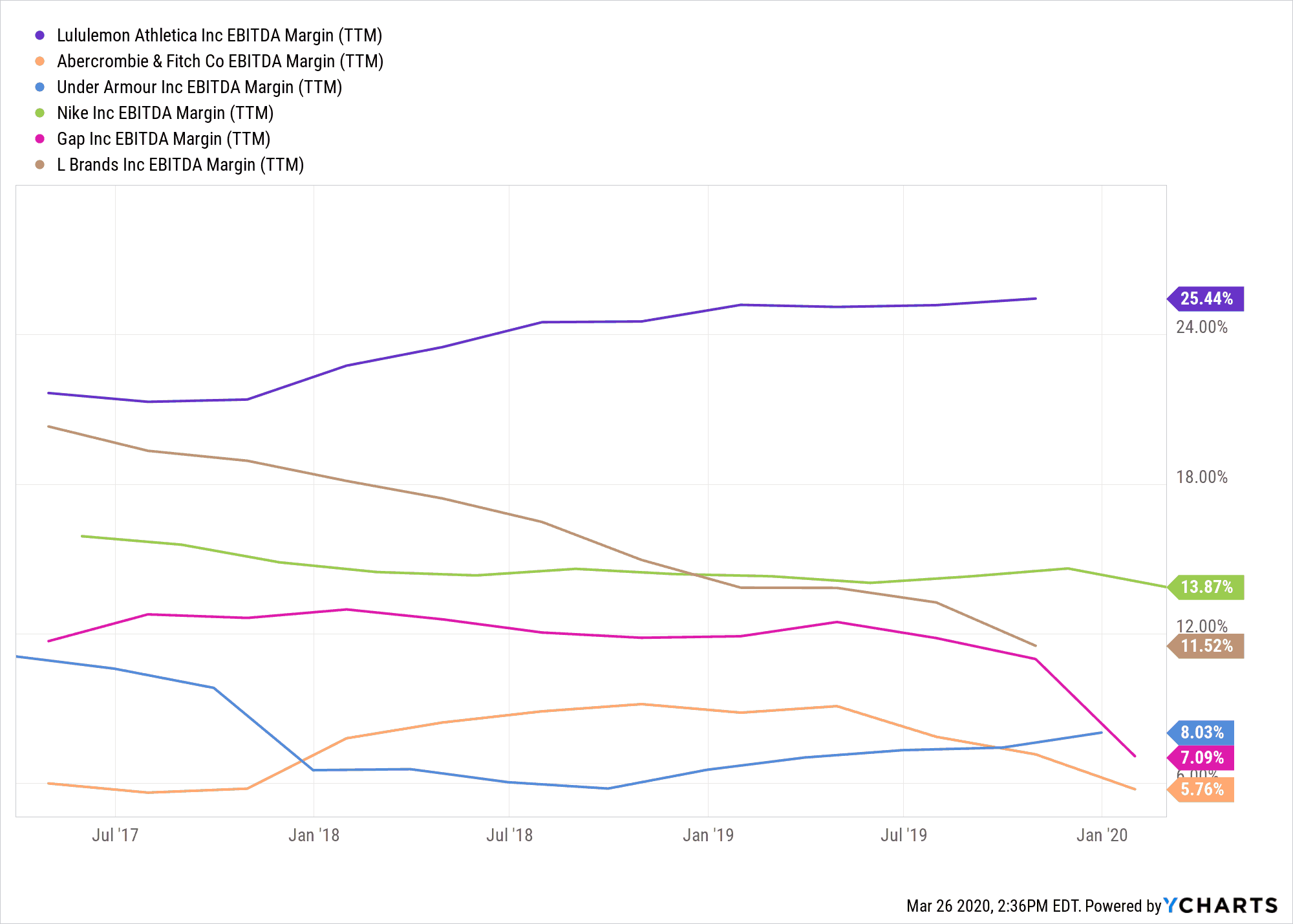

Taking a look at EBITDA Margin, we see that LULU continues to absolutely dominate the competition and has been doing so for the past 3 years.

When it comes to revenue growth, a similar story presents itself.

Although, with that being said, the valuation for LULU is also very rich. The company trades more like a tech stock than it does a retailer, coming in at a forward P/E of about 40 despite the recent troubles in the stock market.

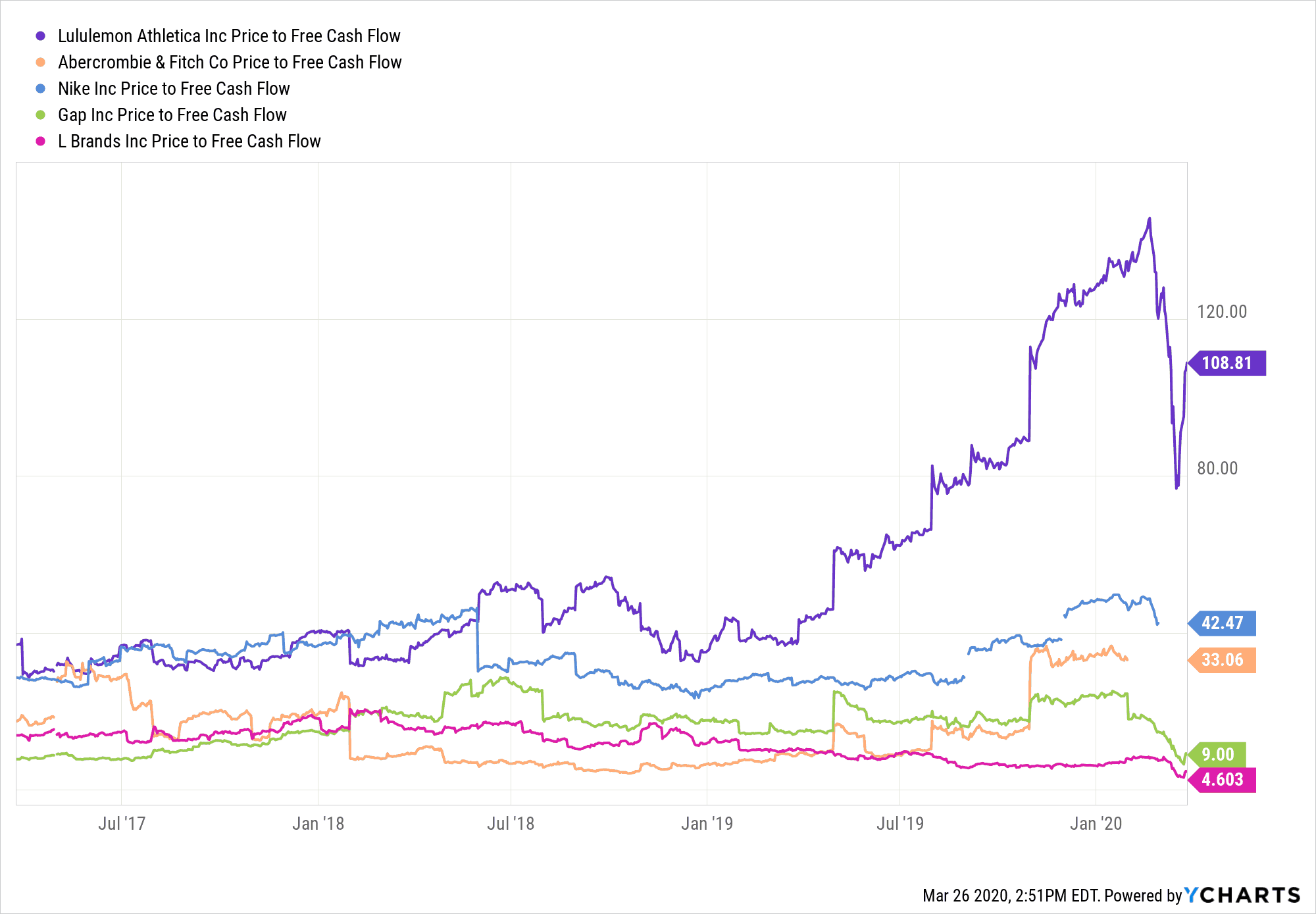

Another thing that investors absolutely love is free cash flow.

Looking at LULU’s Price-to-Free Cashflow multiple, once again LULU blows the competition out of the water and is proven to be a cash generating machine.

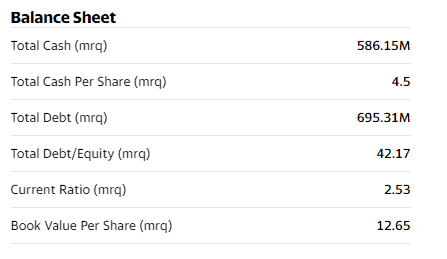

Looking at the balance sheet, we see that LULU has a pretty big cash position and should be able to weather any short-term turbulence like the huge drops in the stock market that has been brought on by the COVID-19 outbreak.

Bottom Line

Should you buy any LULU stock?

With these amazing performances in mind, it’s hard for anyone to say anything bad about LULU, however the valuation does seem a bit lofty considering many other quality stocks have dropped in price dramatically in the past month.

If you’re one who likes to bottom-fish stocks that are beaten down and are at dirt cheap valuations, LULU is not your game.

If you’re one who is looking for more of a quality stock, it’s hard to go wrong with LULU.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.